Your new post is loading...

Your new post is loading...

|

Scooped by

ETF Research & Solutions

June 7, 2012 5:17 AM

|

(This article was first published on Timely Portfolio, and kindly contributed to R-bloggers) As I thought more about Trend Following Factors from Hsieh and Fung, I thought that the trend following factors might indicate a state/regime for...

|

|

Scooped by

ETF Research & Solutions

May 9, 2012 8:29 AM

|

(This article was first published on Systematic Investor » R, and kindly contributed to R-bloggers)

Diversification is hard to find nowadays because financial markets are becoming increasingly correlated.

|

|

Scooped by

ETF Research & Solutions

May 1, 2012 1:36 AM

|

Today I want to show how to use Volatility Position Sizing to improve strategy’s Risk Adjusted Performance.

|

|

Scooped by

ETF Research & Solutions

April 23, 2012 4:23 PM

|

(This article was first published on Systematic Investor » R, and kindly contributed to R-bloggers)

I came across a free source of Intraday Forex data while reading Forex Trading with R : Part 1 post.

|

|

Scooped by

ETF Research & Solutions

April 17, 2012 9:51 AM

|

(This article was first published on DataPunks.com » R, and kindly contributed to R-bloggers)

Timely Portfolio has a nice post about linear models sytems for stock.

|

|

Scooped by

ETF Research & Solutions

April 16, 2012 5:56 PM

|

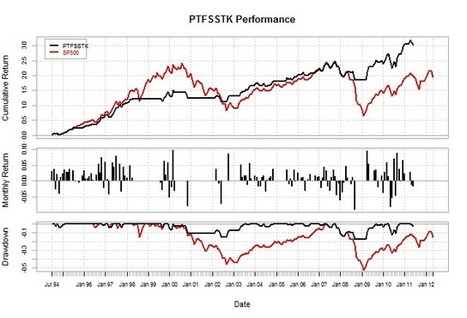

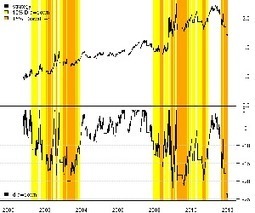

I want to highlight two great Visualization techniques I discovered by reading the fine blog from Timely Portfolio.

First method is based on the lm System on Nikkei with New Chart.

|

|

Scooped by

ETF Research & Solutions

April 10, 2012 8:10 AM

|

RExcel is a great tool to connect R and Microsoft Excel. With a press of a button, I can easily execute my R scripts and present output interactively in Excel. This easy integration allows non-R users to explore the power R language.

|

|

Scooped by

ETF Research & Solutions

April 5, 2012 1:33 AM

|

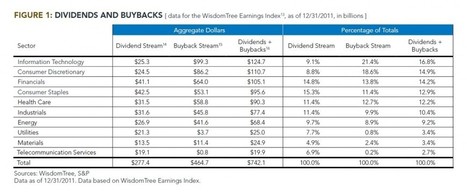

Jeremy Schwartz, the director or research over at WisdomTree, is one of my favorite writers to follow (you can find his archived commentary under Institutional Reads > WisdomTree in the blogroll or here.) A couple fund reads: The Importance Of...

|

|

Scooped by

ETF Research & Solutions

March 28, 2012 4:00 AM

|

>

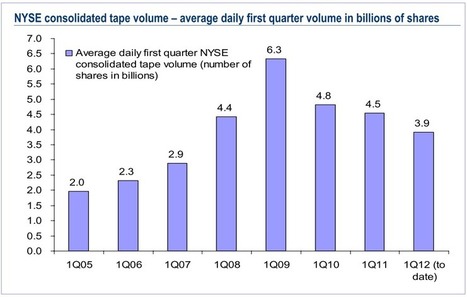

Interesting note from Merril Lynch’s Technical Analyst Mary Ann Bartels about NYSE volume. Ms.

|

|

Scooped by

ETF Research & Solutions

March 26, 2012 1:51 PM

|

(This article was first published on Portfolio Probe » R language, and kindly contributed to R-bloggers)

The missing link between beta and volatility is correlation.

|

|

Scooped by

ETF Research & Solutions

March 26, 2012 12:12 AM

|

|

|

Scooped by

ETF Research & Solutions

March 23, 2012 2:13 AM

|

Hedge

Managing risk more dynamically is becoming an increasingly vital function of the investment management process. Those that can demonstrate their effectiveness at reacting quickly to volatility are held in high regard.

|

|

Scooped by

ETF Research & Solutions

March 19, 2012 1:24 AM

|

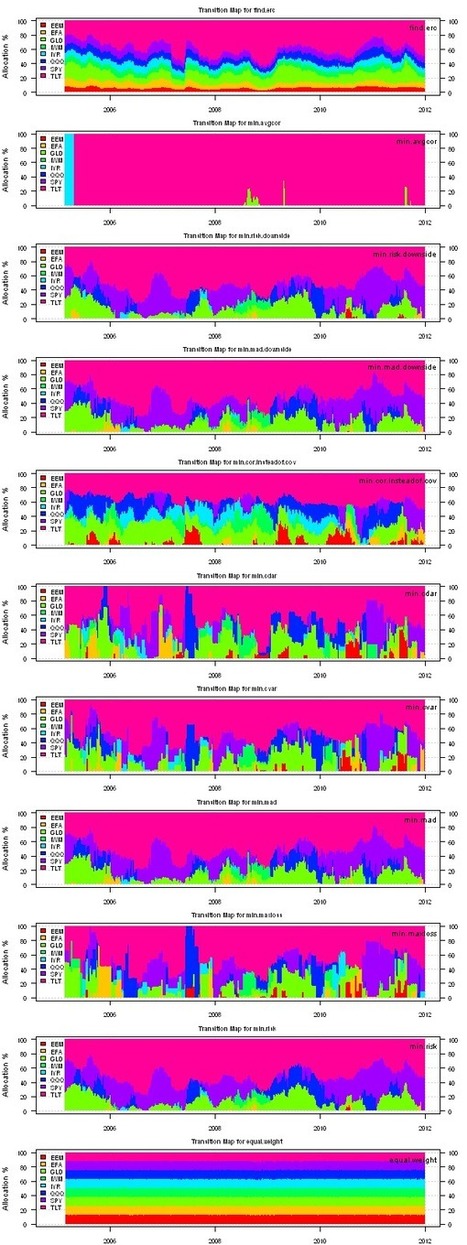

I have previously described a few examples of portfolio construction: Introduction to Asset Allocation Maximum Loss and Mean-Absolute Deviation risk measures 130/30 Portfolio Construction Minimum Investment and Number of Assets Portfolio...

|

|

|

Scooped by

ETF Research & Solutions

May 9, 2012 8:29 AM

|

(This article was first published on Freakonometrics - Tag - R-english, and kindly contributed to R-bloggers) Yesterday, while I was attending the IFM2 conference, at HEC Montreal, I heard a nice talk about credit risk, and a comparison...

|

|

Scooped by

ETF Research & Solutions

May 2, 2012 3:09 PM

|

(This article was first published on Systematic Investor » R, and kindly contributed to R-bloggers)

Today I want to show how to use Volatility Position Sizing to improve strategy’s Risk Adjusted Performance.

|

|

Scooped by

ETF Research & Solutions

April 24, 2012 1:09 AM

|

(This article was first published on rbresearch » R, and kindly contributed to R-bloggers) Analyzing transactions in quantstrat This post will be part 1 of a follow up to the original post, Simple Moving Average Strategy with a Volatility...

|

|

Scooped by

ETF Research & Solutions

April 19, 2012 7:24 AM

|

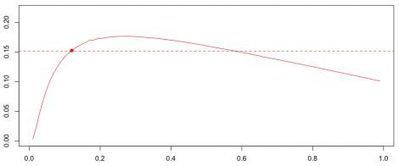

I did a very basic experiment in Efficient Frontier of Buy-Hold and Tactical System where I determined the efficient frontier of the S&P 500 with itself transformed by a Mebane Faber 10-month moving average tactical allocation.

|

|

Scooped by

ETF Research & Solutions

April 16, 2012 5:57 PM

|

(This article was first published on DiffusePrioR » R, and kindly contributed to R-bloggers)

Typically, regression models in empirical economic research suffer from at least one form of endogeneity bias.

|

|

Scooped by

ETF Research & Solutions

April 16, 2012 5:56 PM

|

The last decade we have seen a significant increase in the demand for high frequency data. This is explained for a large part by an increased attention of the academic world in algoritmic trading.

|

|

Scooped by

ETF Research & Solutions

April 5, 2012 1:33 AM

|

(This article was first published on Portfolio Probe » R language, and kindly contributed to R-bloggers)

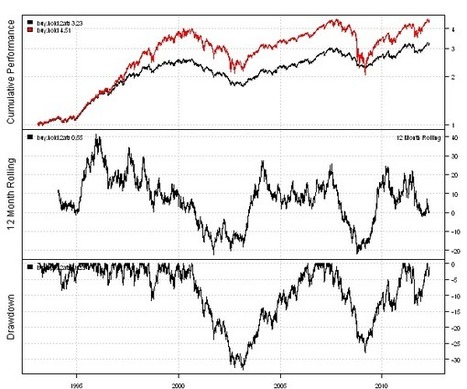

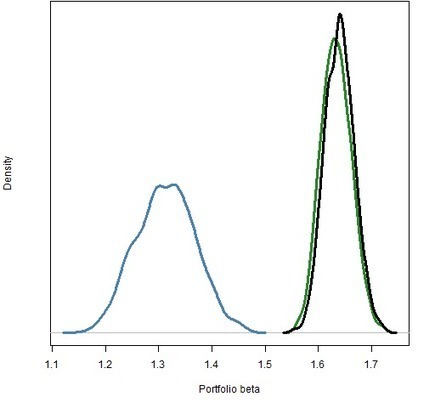

How did the constraints affect portfolio betas, and how did the betas change over time?

|

|

Scooped by

ETF Research & Solutions

April 3, 2012 4:54 PM

|

I want to introduce the Transaction Cost and Execution Price functionality in the Backtesting library in the Systematic Investor Toolbox.

The Transaction Cost is implemented by a commission parameter in the bt.run() function.

|

|

Scooped by

ETF Research & Solutions

March 27, 2012 3:42 AM

|

Contrary to what traditional asset pricing would imply, a strategy that bets against beta, i.e.

|

|

Scooped by

ETF Research & Solutions

March 26, 2012 12:12 AM

|

It has been over 5 years and 1,000 posts since I started writing, so I thought I would dig through the archives and touch on a few of my favorite posts, and maybe some of the dumber/better ideas over the years…but to start, below is the very first...

|

|

Scooped by

ETF Research & Solutions

March 26, 2012 12:10 AM

|

David Varadi have recently wrote two posts about Gini Coefficient: I Dream of Gini, and Mean-Gini Optimization.

|

|

Scooped by

ETF Research & Solutions

March 20, 2012 2:23 AM

|

(This article was first published on Systematic Investor » R, and kindly contributed to R-bloggers) In the last post, Portfolio Optimization: Specify constraints with GNU MathProg language, Paolo and MC raised a question: “How would you...

|