Thu 26 Jan 12 | 06:00 AM ET...

Get Started for FREE

Sign up with Facebook Sign up with X

I don't have a Facebook or a X account

Your new post is loading...

Your new post is loading... Your new post is loading...

Your new post is loading...

(This article was first published on RStudio Blog, and kindly contributed to R-bloggers) The final version of RStudio v0.95 is now available for download from our website (thanks to everyone who put the preview release through its paces...

Some reads to start off your day: • Tech Giants’ Revenue Slows (WSJ) see also Google Cools Off, and Stock Drops (WSJ) • Josh Brown: It’s an RIA World, Everyone Else Just Lives in it (WSJ) • 5 Reasons QE3 Is Off The Table (Pragmatic Capitalism) but...

THIS IS NOT INVESTMENT ADVICE. The information is provided for informational purposes only.

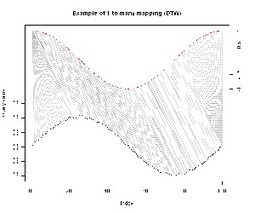

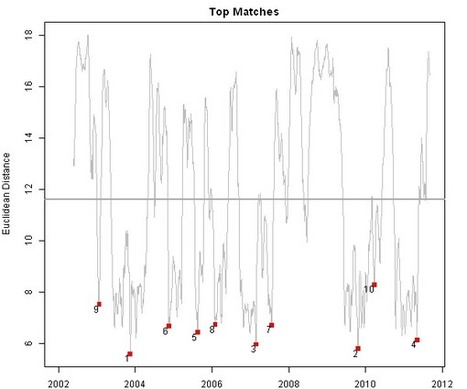

In the Time Series Matching post, I used one to one mapping to the compute distance between the query(current pattern) and reference(historical time series).

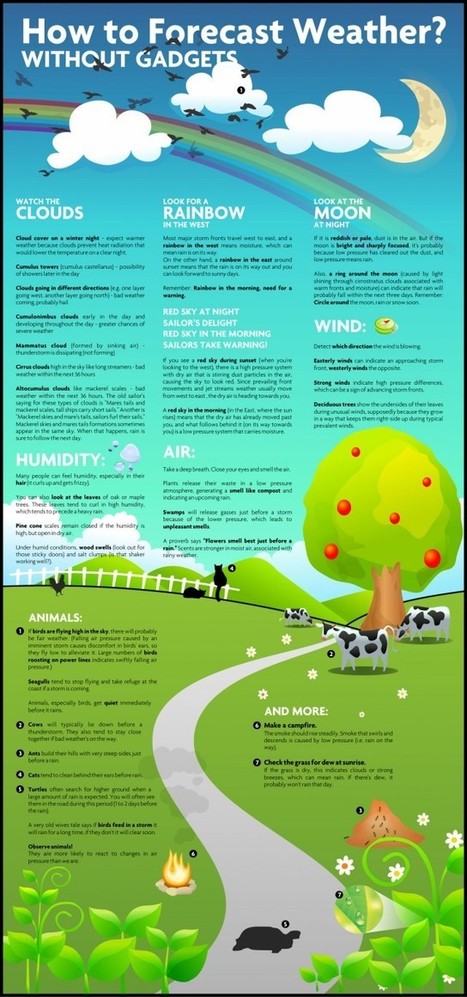

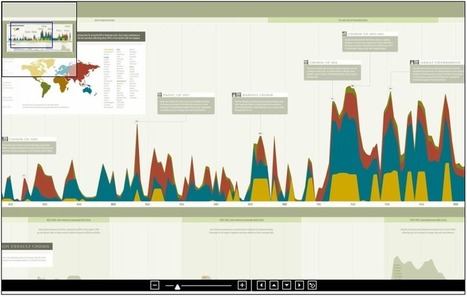

We first looked at this back in 2010, but with sailing weather a mere 3 months away, its time to bring this back: > > Full graphic after the jump > click for giant version via Daily Infographic...

(This article was first published on R, Ruby, and Finance, and kindly contributed to R-bloggers)

I was searching for open data recently, and stumbled on Socrata.

(This article was first published on R, Ruby, and Finance, and kindly contributed to R-bloggers) I recently posted an introduction to the Kaggle Algorithmic Trading Challenge, which I competed in.I said that I would post about my...

(This article was first published on Systematic Investor » R, and kindly contributed to R-bloggers)

THIS IS NOT INVESTMENT ADVICE. The information is provided for informational purposes only.

(This article was first published on Revolutions, and kindly contributed to R-bloggers) Last year, the Statistics and Mathematics Department of the Vienna University School of Economics and Business presented a research seminar series on...

(This article was first published on R-statistics blog » R, and kindly contributed to R-bloggers)

(This article was first published on Systematic Investor » R, and kindly contributed to R-bloggers)

I want to discuss the implementation of Rotational Trading Strategies using the backtesting library in the Systematic Investor Toolbox.The Rotational Trading strategy switches investment allocations throughout the time, betting on few top ranked...

I wrote about Rebalancing in the Asset Allocation Process Summary post. Deciding how and when to rebalance (update the portfolio to the target mix) is one of the critical steps in the Asset Allocation Process.

|

(This article was first published on Portfolio Probe » R language, and kindly contributed to R-bloggers) Why returns have a stable distribution As “A tale of two returns” points out, the log return of a long period of time is the sum of the...

(This article was first published on Econometric Sense, and kindly contributed to R-bloggers)

In a previous post, I worked through the theory behind intervention analysis.

History Shots has a cool new graphic poster for sale looking at the long history of Financial Crises.

(This article was first published on R, Ruby, and Finance, and kindly contributed to R-bloggers)

Linear regression can be a fast and powerful tool to model complex phenomena.

Quote of the day

“We shouldn’t be criticized for using Chinese workers,” a current Apple executive said. “The U.S. has stopped producing people with the skills we need.” (NYTimes) Chart of the day Should we trust the rally in the Shanghai Composite?

(This article was first published on mages' blog, and kindly contributed to R-bloggers)

The financial crisis has put a lot of pressure on countries' long-term foreign currency credit ratings, with France recently being downgraded by S&P.

(This article was first published on Rrasch, and kindly contributed to R-bloggers)

Ever since R was born (evoked?) geeks have been trying to get it to talk HTML. A list of web interfaces for R is updated on CRAN here.

(This article was first published on Programming R, and kindly contributed to R-bloggers)

R is used extensively in the financial industry; many of my recent clients have been working in or developing products for the financial sector.

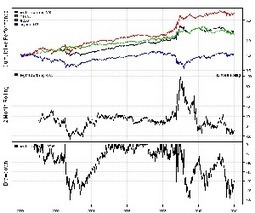

Equities as measured by the S&P 500 ended virtually unchanged for the calendar year 2011. Were it not for dividends the year would have been a complete washout. What 2011 did not lack was volatility. Given the year’s performance one could argue...

To follow up with last post, and also nicely tying into Engineering Returns’ recent sector rotational system I will show a factor decomposition of the S&P 500 from different sectors.

Quantum Financier wrote an interesting article Regime Switching System Using Volatility Forecast. The article presents an elegant algorithm to switch between mean-reversion and trend-following strategies based on the market volatility.

Frank Hassler at Engineering Returns blog wrote an excellent article Rotational Trading: how to reduce trades and improve returns. The article presents four methods to reduce trades:

|