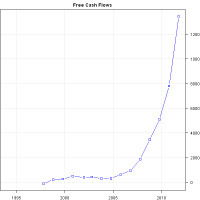

Today I want to show a simple example of how we can value a company using Discounted Cash Flow (DCF) analysis. The idea is to compute the company’s Intrinsic Value based on the discounted future cash-flows.

Your new post is loading...

Your new post is loading... Your new post is loading...

Your new post is loading...

Today I want to show a simple example of how we can value a company using Discounted Cash Flow (DCF) analysis. The idea is to compute the company’s Intrinsic Value based on the discounted future cash-flows.

No comment yet.

Sign up to comment

(This article was first published on a modeler's tribulations, gopi goteti's web log, and kindly contributed to R-bloggers) Problem When a correlation or covariance matrix is not positive definite (i.e., in instances when some or all...

(This article was first published on Revolutions, and kindly contributed to R-bloggers) Jeffrey Breen (the man behind the Twitter airline sentiment analysis example) recently posted a collection of slides with some great tips for accessing...

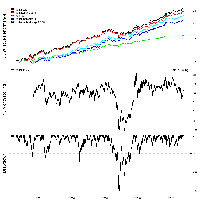

(This article was first published on Timely Portfolio, and kindly contributed to R-bloggers) Almost always, when I see a system backtested, the backtest assumes a static portfolio with no contributions or withdrawals. This assumption only...

(This article was first published on The Shape of Code » R, and kindly contributed to R-bloggers)

Today I want to follow up with the Minimum Correlation Algorithm Paper post and show how to incorporate the Minimum Correlation Algorithm into your portfolio construction work flow and also explain why I like the Minimum Correlation Algorithm.

(This article was first published on Stats raving mad » R, and kindly contributed to R-bloggers)

(This article was first published on rbresearch » R, and kindly contributed to R-bloggers)

The strategies used in Strategy Diversification in R were labeled as Strategy1 and Strategy2.

(This article was first published on Pairach Piboonrungroj » R, and kindly contributed to R-bloggers)

Arguably, knitr (CRAN link) is the most outstanding R package of this year and its creator, Yihui Xie is the star of the useR!

A very good list of ressources, worth to read

As a newbie to R, I thought it would be worthy to note a few quality R packages that seem to have more advanced some functionality that Matlab does not even give you. Here is my experience thus far:

(This article was first published on Revolutions, and kindly contributed to R-bloggers)

Earlier this week, Revolution Analytics' Joe Rickert gave a webinar Introduction to R for Data Mining.

(This article was first published on tradeblotter » R, and kindly contributed to R-bloggers)

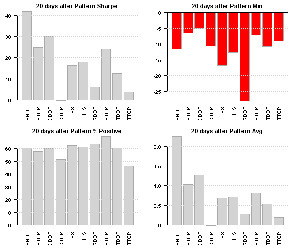

(This article was first published on Systematic Investor » R, and kindly contributed to R-bloggers) In the last post, Classical Technical Patterns, I discussed the algorithm and pattern definitions presented in the Foundations of Technical...

|

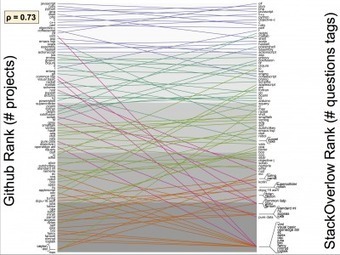

(This article was first published on Revolutions, and kindly contributed to R-bloggers) Data Scientist Drew Conway tackles the problem of deciding which programming languages are the most popular in an interesting way: by comparing the...

Mean-variance investing is all about diversification. Diversification considers assets holistically and exploits the interaction of assets with each other, rather than viewing assets in isolation. Holding a diversified portfolio allows investors to increase expected returns while reducing risks. In practice, mean-variance portfolios that constrain the mean, volatility, and correlation inputs to reduce sampling error have performed much better than unconstrained portfolios. These special cases include equal-weighted, minimum variance, and risk parity portfolios.

I have previously described and back-tested the Permanent Portfolio strategy based on the series of posts at the GestaltU blog.

(This article was first published on FOSS Trading, and kindly contributed to R-bloggers) If you haven't signed up for the Introduction to Computational Finance and Financial Econometrics course taught by Eric Zivot on Coursera, it's not too...

(This article was first published on Systematic Investor » R, and kindly contributed to R-bloggers)

(This article was first published on Revolutions, and kindly contributed to R-bloggers)

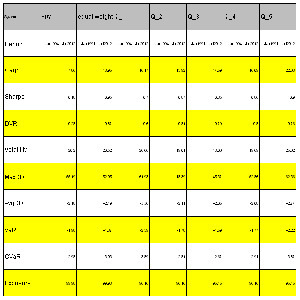

In the prior post, Factor Attribution 2, I have shown how Factor Attribution can be applied to decompose fund’s returns in to Market, Capitalization, and Value factors, the “three-factor model” of Fama and French.

(This article was first published on Systematic Investor » R, and kindly contributed to R-bloggers)

I want to continue with Factor Attribution theme that I presented in the Factor Attribution post.

(This article was first published on R User Groups, and kindly contributed to R-bloggers) This post shares the video from a talk presented on June 20 2012 by Dr Lyndon Walker (...

A very good set of links to integrate R with other sets.

I just returned from the useR! 2012 conference for developers and users of R.

- One of the common themes to many of the presentations was integration of R-based statistical systems with other systems, be they other programming languages, web systems, or enterprise data systems.

- Some highlights for me were an update to Rserve that includes 1-stop web services, and a presentation on ESB integration.

- Although I didn’t see it discussed, the new httr package for easier access to web services is also another outstanding development in integrating R into large-scale systems.

(This article was first published on Ben Mazzotta's Weblog » R, and kindly contributed to R-bloggers)

I’m hardly the first person you would want to talk to about learning statistics in R.

In the last post, Classical Technical Patterns, I discussed the algorithm and pattern definitions presented in the Foundations of Technical Analysis by A. Lo, H. Mamaysky, J. Wang (2000) paper.

|