"Despite considering myself a cryptographer, I have not found myself particularly drawn to “crypto.” I don’t think I’ve ever actually said the words “get off my lawn,” but I’m much more likely to click on Pepperidge Farm Remembers flavored memes about how “crypto” used to mean “cryptography” than I am the latest NFT drop.

Also – cards on the table here – I don’t share the same generational excitement for moving all aspects of life into an instrumented economy.

Even strictly on the technological level, though, I haven’t yet managed to become a believer. So given all of the recent attention into what is now being called web3, I decided to explore some of what has been happening in that space more thoroughly to see what I may be missing.

How I think about 1 and 2

web3 is a somewhat ambiguous term, which makes it difficult to rigorously evaluate what the ambitions for web3 should be, but the general thesis seems to be that web1 was decentralized, web2 centralized everything into platforms, and that web3 will decentralize everything again. web3 should give us the richness of web2, but decentralized.

It’s probably good to have some clarity on why centralized platforms emerged to begin with, and in my mind the explanation is pretty simple:

People don’t want to run their own servers, and never will. The premise for web1 was that everyone on the internet would be both a publisher and consumer of content as well as a publisher and consumer of infrastructure.

We’d all have our own web server with our own web site, our own mail server for our own email, our own finger server for our own status messages, our own chargen server for our own character generation. However – and I don’t think this can be emphasized enough – that is not what people want. People do not want to run their own servers.

Even nerds do not want to run their own servers at this point. Even organizations building software full time do not want to run their own servers at this point. If there’s one thing I hope we’ve learned about the world, it’s that people do not want to run their own servers. The companies that emerged offering to do that for you instead were successful, and the companies that iterated on new functionality based on what is possible with those networks were even more successful.

A protocol moves much more slowly than a platform. After 30+ years, email is still unencrypted; meanwhile WhatsApp went from unencrypted to full e2ee in a year. People are still trying to standardize sharing a video reliably over IRC; meanwhile, Slack lets you create custom reaction emoji based on your face.

This isn’t a funding issue. If something is truly decentralized, it becomes very difficult to change, and often remains stuck in time. That is a problem for technology, because the rest of the ecosystem is moving very quickly, and if you don’t keep up you will fail. There are entire parallel industries focused on defining and improving methodologies like Agile to try to figure out how to organize enormous groups of people so that they can move as quickly as possible because it is so critical.

When the technology itself is more conducive to stasis than movement, that’s a problem. A sure recipe for success has been to take a 90’s protocol that was stuck in time, centralize it, and iterate quickly.

But web3 intends to be different, so let’s take a look. In order to get a quick feeling for the space and a better understanding for what the future may hold, I decided to build a couple of dApps and create an NFT.

Making some distributed apps

To get a feeling for the web3 world, I made a dApp called Autonomous Art that lets anyone mint a token for an NFT by making a visual contribution to it. The cost of making a visual contribution increases over time, and the funds a contributor pays to mint are distributed to all previous artists (visualizing this financial structure would resemble something similar to a pyramid shape). At the time of this writing, over $38k USD has gone into creating this collective art piece.

I also made a dApp called First Derivative that allows you to create, discover, and exchange NFT derivatives which track an underlying NFT, similar to financial derivatives which track an underlying asset 😉.

Both gave me a feeling for how the space works. To be clear, there is nothing particularly “distributed” about the apps themselves: they’re just normal react websites. The “distributedness” refers to where the state and the logic/permissions for updating the state lives: on the blockchain instead of in a “centralized” database.

One thing that has always felt strange to me about the cryptocurrency world is the lack of attention to the client/server interface. When people talk about blockchains, they talk about distributed trust, leaderless consensus, and all the mechanics of how that works, but often gloss over the reality that clients ultimately can’t participate in those mechanics. All the network diagrams are of servers, the trust model is between servers, everything is about servers. Blockchains are designed to be a network of peers, but not designed such that it’s really possible for your mobile device or your browser to be one of those peers.

With the shift to mobile, we now live firmly in a world of clients and servers – with the former completely unable to act as the latter – and those questions seem more important to me than ever.

Meanwhile, ethereum actually refers to servers as “clients,” so there’s not even a word for an actual untrusted client/server interface that will have to exist somewhere, and no acknowledgement that if successful there will ultimately be billions (!) more clients than servers.

For example, whether it’s running on mobile or the web, a dApp like Autonomous Art or First Derivative needs to interact with the blockchain somehow – in order to modify or render state (the collectively produced work of art, the edit history for it, the NFT derivatives, etc). That’s not really possible to do from the client, though, since the blockchain can’t live on your mobile device (or in your desktop browser realistically). So the only alternative is to interact with the blockchain via a node that’s running remotely on a server somewhere.

A server! But, as we know, people don’t want to run their own servers. As it happens, companies have emerged that sell API access to an ethereum node they run as a service, along with providing analytics, enhanced APIs they’ve built on top of the default ethereum APIs, and access to historical transactions. Which sounds… familiar. At this point, there are basically two companies. Almost all dApps use either Infura or Alchemy in order to interact with the blockchain. In fact, even when you connect a wallet like MetaMask to a dApp, and the dApp interacts with the blockchain via your wallet, MetaMask is just making calls to Infura!

These client APIs are not using anything to verify blockchain state or the authenticity of responses. The results aren’t even signed. An app like Autonomous Art says “hey what’s the output of this view function on this smart contract,” Alchemy or Infura responds with a JSON blob that says “this is the output,” and the app renders it.

This was surprising to me. So much work, energy, and time has gone into creating a trustless distributed consensus mechanism, but virtually all clients that wish to access it do so by simply trusting the outputs from these two companies without any further verification. It also doesn’t seem like the best privacy situation. Imagine if every time you interacted with a website in Chrome, your request first went to Google before being routed to the destination and back. That’s the situation with ethereum today. All write traffic is obviously already public on the blockchain, but these companies also have visibility into almost all read requests from almost all users in almost all dApps.

Partisans of the blockchain might say that it’s okay if these types of centralized platforms emerge, because the state itself is available on the blockchain, so if these platforms misbehave clients can simply move elsewhere. However, I would suggest that this is a very simplistic view of the dynamics that make platforms what they are.

Let me give you an example.

Making an NFT

I also wanted to create a more traditional NFT. Most people think of images and digital art when they think of NFTs, but NFTs generally do not store that data on-chain. For most NFTs of most images, that would be much too expensive.

Instead of storing the data on-chain, NFTs instead contain a URL that points to the data. What surprised me about the standards was that there’s no hash commitment for the data located at the URL. Looking at many of the NFTs on popular marketplaces being sold for tens, hundreds, or millions of dollars, that URL often just points to some VPS running Apache somewhere. Anyone with access to that machine, anyone who buys that domain name in the future, or anyone who compromises that machine can change the image, title, description, etc for the NFT to whatever they’d like at any time (regardless of whether or not they “own” the token). There’s nothing in the NFT spec that tells you what the image “should” be, or even allows you to confirm whether something is the “correct” image.

So as an experiment, I made an NFT that changes based on who is looking at it, since the web server that serves the image can choose to serve different images based on the IP or User Agent of the requester. For example, it looked one way on OpenSea, another way on Rarible, but when you buy it and view it from your crypto wallet, it will always display as a large 💩 emoji. What you bid on isn’t what you get. There’s nothing unusual about this NFT, it’s how the NFT specifications are built. Many of the highest priced NFTs could turn into 💩 emoji at any time; I just made it explicit.

After a few days, without warning or explanation, the NFT I made was removed from OpenSea (an NFT marketplace):

The takedown suggests that I violated some Term Of Service, but after reading the terms, I don’t see any that prohibit an NFT which changes based on where it is being looked at from, and I was openly describing it that way.

What I found most interesting, though, is that after OpenSea removed my NFT, it also no longer appeared in any crypto wallet on my device. This is web3, though, how is that possible?

A crypto wallet like MetaMask, Rainbow, etc is “non-custodial” (the keys are kept client side), but it has the same problem as my dApps above: a wallet has to run on a mobile device or in your browser. Meanwhile, ethereum and other blockchains have been designed with the idea that it’s a network of peers, but not designed such that it’s really possible for your mobile device or your browser to be one of those peers.

A wallet like MetaMask needs to do basic things like display your balance, your recent transactions, and your NFTs, as well as more complex things like constructing transactions, interacting with smart contracts, etc. In short, MetaMask needs to interact with the blockchain, but the blockchain has been built such that clients like MetaMask can’t interact with it. So like my dApp, MetaMask accomplishes this by making API calls to three companies that have consolidated in this space.

For instance, MetaMask displays your recent transactions by making an API call to etherscan:

GET https://api.etherscan.io/api?module=account&address=0x0208376c899fdaEbA530570c008C4323803AA9E8&offset=40&order=desc&action=txlist&tag=latest&page=1 HTTP/2.0

…displays your account balance by making an API call to Infura:

…displays your NFTs by making an API call to OpenSea:

GET https://api.opensea.io/api/v1/assets?owner=0x0208376c899fdaEbA530570c008C4323803AA9E8&offset=0&limit=50 HTTP/2.0

Again, like with my dApp, these responses are not authenticated in some way. They’re not even signed so that you could later prove they were lying. It reuses the same connections, TLS session tickets, etc for all the accounts in your wallet, so if you’re managing multiple accounts in your wallet to maintain some identity separation, these companies know they’re linked.

MetaMask doesn’t actually do much, it’s just a view onto data provided by these centralized APIs. This isn’t a problem specific to MetaMask – what other option do they have? Rainbow, etc are set up in exactly the same way. (Interestingly, Rainbow has their own data for the social features they’re building into their wallet – social graph, showcases, etc – and have chosen to build all of that on top of Firebase instead of the blockchain.)

All this means that if your NFT is removed from OpenSea, it also disappears from your wallet. It doesn’t functionally matter that my NFT is indelibly on the blockchain somewhere, because the wallet (and increasingly everything else in the ecosystem) is just using the OpenSea API to display NFTs, which began returning 304 No Content for the query of NFTs owned by my address!

Recreating this world

Given the history of why web1 became web2, what seems strange to me about web3 is that technologies like ethereum have been built with many of the same implicit trappings as web1. To make these technologies usable, the space is consolidating around… platforms. Again. People who will run servers for you, and iterate on the new functionality that emerges. Infura, OpenSea, Coinbase, Etherscan.

Likewise, the web3 protocols are slow to evolve. When building First Derivative, it would have been great to price minting derivatives as a percentage of the underlying’s value. That data isn’t on chain, but it’s in an API that OpenSea will give you. People are excited about NFT royalties for the way that they can benefit creators, but royalties aren’t specified in ERC-721, and it’s too late to change it, so OpenSea has its own way of configuring royalties that exists in web2 space. Iterating quickly on centralized platforms is already outpacing the distributed protocols and consolidating control into platforms.

Given those dynamics, I don’t think it should be a surprise that we’re already at a place where your crypto wallet’s view of your NFTs is OpenSea’s view of your NFTs. I don’t think we should be surprised that OpenSea isn’t a pure “view” that can be replaced, since it has been busy iterating the platform beyond what is possible strictly with the impossible/difficult to change standards.

I think this is very similar to the situation with email. I can run my own mail server, but it doesn’t functionally matter for privacy, censorship resistance, or control – because GMail is going to be on the other end of every email that I send or receive anyway. Once a distributed ecosystem centralizes around a platform for convenience, it becomes the worst of both worlds: centralized control, but still distributed enough to become mired in time. I can build my own NFT marketplace, but it doesn’t offer any additional control if OpenSea mediates the view of all NFTs in the wallets people use (and every other app in the ecosystem).

This isn’t a complaint about OpenSea or an indictment of what they’ve built. Just the opposite, they’re trying to build something that works. I think we should expect this kind of platform consolidation to happen, and given the inevitability, design systems that give us what we want when that’s how things are organized. My sense and concern, though, is that the web3 community expects some other outcome than what we’re already seeing.

It’s early days

“It’s early days still” is the most common refrain I see from people in the web3 space when discussing matters like these. In some ways, cryptocurrency’s failure to scale beyond relatively nascent engineering is what makes it possible to consider the days “early,” since objectively it has already been a decade or more.

However, even if this is just the beginning (and it very well might be!), I’m not sure we should consider that any consolation. I think the opposite might be true; it seems like we should take notice that from the very beginning, these technologies immediately tended towards centralization through platforms in order for them to be realized, that this has ~zero negatively felt effect on the velocity of the ecosystem, and that most participants don’t even know or care it’s happening. This might suggest that decentralization itself is not actually of immediate practical or pressing importance to the majority of people downstream, that the only amount of decentralization people want is the minimum amount required for something to exist, and that if not very consciously accounted for, these forces will push us further from rather than closer to the ideal outcome as the days become less early.

But you can’t stop a gold rush

When you think about it, OpenSea would actually be much “better” in the immediate sense if all the web3 parts were gone. It would be faster, cheaper for everyone, and easier to use. For example, to accept a bid on my NFT, I would have had to pay over $80-$150+ just in ethereum transaction fees. That puts an artificial floor on all bids, since otherwise you’d lose money by accepting a bid for less than the gas fees. Payment fees by credit card, which typically feel extortionary, look cheap compared to that. OpenSea could even publish a simple transparency log if people wanted a public record of transactions, offers, bids, etc to verify their accounting.

However, if they had built a platform to buy and sell images that wasn’t nominally based on crypto, I don’t think it would have taken off. Not because it isn’t distributed, because as we’ve seen so much of what’s required to make it work is already not distributed. I don’t think it would have taken off because this is a gold rush. People have made money through cryptocurrency speculation, those people are interested in spending that cryptocurrency in ways that support their investment while offering additional returns, and so that defines the setting for the market of transfer of wealth.

The people at the end of the line who are flipping NFTs do not fundamentally care about distributed trust models or payment mechanics, but they care about where the money is. So the money draws people into OpenSea, they improve the experience by building a platform that iterates on the underlying web3 protocols in web2 space, they eventually offer the ability to “mint” NFTs through OpenSea itself instead of through your own smart contract, and eventually this all opens the door for Coinbase to offer access to the validated NFT market with their own platform via your debit card. That opens the door to Coinbase managing the tokens themselves through dark pools that Coinbase holds, which helpfully eliminates the transaction fees and makes it possible to avoid having to interact with smart contracts at all. Eventually, all the web3 parts are gone, and you have a website for buying and selling JPEGS with your debit card. The project can’t start as a web2 platform because of the market dynamics, but the same market dynamics and the fundamental forces of centralization will likely drive it to end up there.

At the end of the stack, NFT artists are excited about this kind of progression because it means more speculation/investment in their art, but it also seems like if the point of web3 is to avoid the trappings of web2, we should be concerned that this is already the natural tendency for these new protocols that are supposed to offer a different future.

I think these market forces will likely continue, and in my mind the question of how long it continues is a question of whether the vast amounts of accumulated cryptocurrency are ultimately inside an engine or a leaky bucket. If the money flowing through NFTs ends up channeled back into crypto space, it could continue to accelerate forever (regardless of whether or not it’s just web2x2). If it churns out, then this will be a blip. Personally, I think enough money has been made at this point that there are enough faucets to keep it going, and this won’t just be a blip. If that’s the case, it seems worth thinking about how to avoid web3 being web2x2 (web2 but with even less privacy) with some urgency.

Creativity might not be enough

I have only dipped my toe in the waters of web3. Looking at it through the lens of these small projects, though, I can easily see why so many people find the web3 ecosystem so neat. I don’t think it’s on a trajectory to deliver us from centralized platforms, I don’t think it will fundamentally change our relationship to technology, and I think the privacy story is already below par for the internet (which is a pretty low bar!), but I also understand why nerds like me are excited to build for it. It is, at the very least, something new on the nerd level – and that creates a space for creativity/exploration that is somewhat reminiscent of early internet days. Ironically, part of that creativity probably springs from the constraints that make web3 so clunky. I’m hopeful that the creativity and exploration we’re seeing will have positive outcomes, but I’m not sure if it’s enough to prevent all the same dynamics of the internet from unfolding again.

If we do want to change our relationship to technology, I think we’d have to do it intentionally.

My basic thoughts are roughly:

We should accept the premise that people will not run their own servers by designing systems that can distribute trust without having to distribute infrastructure. This means architecture that anticipates and accepts the inevitable outcome of relatively centralized client/server relationships, but uses cryptography (rather than infrastructure) to distribute trust. One of the surprising things to me about web3, despite being built on “crypto,” is how little cryptography seems to be involved!

We should try to reduce the burden of building software. At this point, software projects require an enormous amount of human effort. Even relatively simple apps require a group of people to sit in front of a computer for eight hours a day, every day, forever. This wasn’t always the case, and there was a time when 50 people working on a software project wasn’t considered a “small team.” As long as software requires such concerted energy and so much highly specialized human focus, I think it will have the tendency to serve the interests of the people sitting in that room every day rather than what we may consider our broader goals. I think changing our relationship to technology will probably require making software easier to create, but in my lifetime I’ve seen the opposite come to pass. Unfortunately, I think distributed systems have a tendency to exacerbate this trend by making things more complicated and more difficult, not less complicated and less difficult."...

Social Impact Bonds (SIBs) are a private financing mechanism used to fund social programs. Also termed 'Pay For Success,' and 'Outcomes Based' or 'Performance Based' financing, these partnerships involve private entities funding projects aimed at improving social outcomes. If by the end of the project period, 'success' metrics are met (according to third-party evaluators), investors then profit by being paid interest on top of the reimbursed government funds for the cost of the project. This page includes a collection of updates and critical perspectives on these profit structures and on Blockchain Identity systems, de-centralized online ledger programs, poised to be the data backbone that would provide 'proof' of 'program impact' for investors. For files related to Blockchain, see: http://bit.ly/Blockchain_Files. [Note: Views presented on this page are re-shared from external websites and may not necessarily represent the views nor official position of the curator nor employer of the curator.]

Abstract "This article considers proponents’ arguments for Pay for Success also known as Social Impact Bonds. Pay for Success allows banks to finance public services with potential profits tied to metrics. Pay for Success has received federal support through the Every Student Succeeds Act of 2016 and is predicted by 2020 to expand in the US to a trillion dollars. As school districts, cities, and states face debt and budget crises, Pay for Success has been advocated by philanthropists, corporate consulting firms, politicians, and investment banks on the grounds of improving accountability, cost savings, risk transfer, and market discipline. With its trailblazing history in neoliberal education, Chicago did an early experiment in Pay for Success. This article provides a conceptual analysis of the key underlying assumptions and ideologies of Pay for Success. It examines the claims of proponents and critics and sheds light on the financial and ideological motivations animating Pay for Success. The article contends that Pay for Success primarily financially benefits banks without providing the benefits that proponents promise. It concludes by considering Pay for Success in relation to broader structural economic considerations and the recent uses of public schooling to produce short-term profit for capitalists."

Keywords Pay for Success; Social Impact Bonds; Chicago School Reform; Neoliberal Education; Corporate School Reform; Venture Philanthropy

By Kenneth Saltman "Investment banks such as Goldman Sachs, Bank of America, and J. P. Morgan; philanthropies such as the Rockefeller Foundation; politicians such as Chicago Mayor Rahm Emanuel and Massachusetts former governor and now Bain Capital managing director Deval Patrick; and elite universities such as Harvard have been aggressively promoting Pay for Success (also known as social impact bonds) as a solution to intractable financial and political problems facing public education and other public services. In these schemes, investment banks pay for public services to be contracted out to private providers and stand to earn much more money than the cost of the service. For example, Goldman Sachs put up $16.6 million to fund an early childhood education program in Chicago, yet it is getting more than $30 million[1] from the city. While Pay for Success is only at its early stages in the United States, the Rockefeller Foundation and Merrill Lynch estimate that by 2020, the market size for impact investing will reach between $400 billion and $1 trillion.[2] The Every Student Succeeds Act of 2016, the latest iteration of the Elementary and Secondary Education Act of 1965, directs federal dollars to incentivize these for-profit educational endeavors significantly, legitimizing and institutionalizing them.

Success is promoted by proponents as an innovative financing technique that brings together social service providers with private funders and nonprofit organizations committed to expanding social service provision. In theory, Pay for Success expands accountability because programs are independently evaluated for their success and the government only pays the funder (the bank) if the program meets the metrics. If the program exceeds the metrics, then the investor can receive bonus money, making the program much more expensive for the public and highly lucrative for the banks.

Banks love Pay for Success because they can profit massively from it and invest money with high returns at a time of a glut of capital and historically low interest rates. Politicians (especially rightist democrats) love Pay for Success because they can claim to be expanding public services without raising taxes or issuing bonds and will only have the public pay for “what works.” Elite universities and corporate philanthropies love Pay for Success because they support “innovation” and share an ethos that only the prime beneficiaries of the current economy, the rich, can save the poor.

Pay for Success began as social impact bonds and were imported into the United States from the United Kingdom around 2010. They were promoted by the leading consultancy advocate of neoliberal education, McKinsey Consulting; the neoliberal think tank Center for American Progress, which was founded by former Clinton chief of staff and Democratic Party leader John Podesta (who also led Obama’s transition); and the Rockefeller Foundation. Pay for Success expansion is now the central agenda of the Rockefeller Foundation. Shortly before championing Pay for Success for Chicago, Rahm Emanuel served as Obama’s chief of staff, having had a long career as a hard-driving Democratic congressman and political money raiser and also an investment banker. Certain other key figures lobbied to expand the use of Pay for Success. Most notably, Jeffrey Liebman went from Obama’s Office of Management and Budget to a large center at Harvard, the Government Performance Lab in the Kennedy School of Government, dedicated to expanding Pay for Success. Liebman is a leader of the Center for American Progress and was a key economic advisor to Obama in his 2008 campaign. Other key influencers of Pay for Success include the Rockefeller Foundation and Third Sector Capital.

Advocates explain that the value of a Pay for Success program is allegedly that it creates a “market incentive” for a bank or investor to fund a social program when there is not the political will to support the expansion of public services, and second, by injecting “market discipline” into the bureaucratically encumbered public sector, Pay for Success will make the public sector “accountable” through investment in “what works,” and it will avoid funding public programs for which the public has “little to show,” as Liebman and Third Sector Capital Partners are fond of suggesting (Wallace, 2014).[3] The value of any public spending in this view must be measurable through quantitative metrics to be of social value. Third, it consequently saves money by not funding programs that cannot be shown to be effective, and fourth, it shifts risk away from the public and onto the private sector while retaining only the potential social benefit for the public. Last, it mobilizes beneficent corporations, banks, powerful nonprofit companies, and philanthropic foundations to save the poor, the powerless, and the public from themselves. Here Goldman Sachs frames its profit-seeking activities as corporate social responsibility, charity, and good works that define its image in the public mind. In fact, all five of these positions that advocates claim explicitly or implicitly to support the expansion of Pay for Success are baseless.

The Myths of Pay for Success

Myth 1: Market Discipline

Repeating a long-standing neoliberal mantra of private-sector efficiency and public-sector bloat, advocates of Pay for Success claim that the programs are necessary because they inject a healthy dose of market discipline into the bureaucratically encumbered and unaccountable public sphere. According to the leading proponent of Pay for Success, Jeffrey Liebman, private-sector finance produces this market discipline because governments do not monitor and measure the services contractors provide. Says Liebman, “[Government] programs that don’t produce results continue to be financed year after year, something that would not happen in the business world.”[4] This is an odd claim from one of Obama’s leading economic advisors at the time that Obama was sworn in as president and who proceeded to have the public sector bail out the private sector. The 2008 financial bailout of the banks by the U.S. federal government represents a repudiation of the neoliberal logic of the natural discipline of markets and of deregulation. The private sector, including banks, insurance companies, and the automotive industry, needed the public sector to step in and save unprofitable businesses and businesses that had invested in the deregulated mortgage-backed securities market. More broadly, some of the largest sectors of the economy, such as defense, agriculture, and entertainment, rely on massive public-sector subsidies to function. Specifically, the financial crisis and consequent recession were a result first of neoliberal bank deregulation and a faith in markets to regulate themselves, but also they demonstrated the illegal activity, fraud, and lies of the same banks that now seek profit through Pay for Success, including Goldman Sachs, Bank of America, Merrill Lynch, and J. P. Morgan.

Pay for Success proponents claim that the financing scheme is necessary because there would otherwise not be the political will to do projects like early childhood education in Chicago for a couple of thousand children or recidivism reduction programs in Massachusetts. Third Sector Capital Partners, a nonprofit that relies on Pay for Success expansion as a cornerstone of its business, claims that Americans do not support state spending and hence Pay for Success is necessary.[5] However, Gallup shows that 75 percent of Americans favor expanded public spending on infrastructure, and 58 percent support replacing the Affordable Care Act with a universal federal health care system.[6] Indeed, as long-standing studies and, more recently, the Bernie Sanders presidential campaign of 2016 indicate, a large percentage of Americans support a range of increased spending on progressive social programs.

A mantra found in the literature that advocates Pay for Success is that it “allow[s] the government to avoid paying for programs that don’t make a difference.”[7] For working-class and poor citizens, many of whom are working two or three low-paying jobs, the cost of private early childcare and education is a major financial burden. The fact that early childcare and education have become corporatized by national companies who pay superexploitative wages to workers only worsens the situation. The fact that early childcare and education are vital economic needs raises a question about whose political will is in question when Pay for Success proponents claim that the only way to provide early child educational services is with the involvement of banks, and that without banks, it should not be provided. The parents and community members are not the ones who lack the political will. Political and financial elites do not want to pay for other people’s children—without a cut."...

"There are countless examples of the dangers posed by national ID schemes, including from Kenya, Uganda, Pakistan, India and elsewhere."

By Elizabeth M. Renieris

"Ethiopia has been making international headlines due to the steep escalation of a nearly year-long civil war in its northern Tigray region and ensuing humanitarian crisis, with millions teetering on the brink of famine and genocide. At the same time, we are beginning to recognize the role that technology companies and platforms can play in exacerbating such crises.

For example, Meta (formerly known as Facebook) and Twitter have been implicated in worsening matters by inciting violence and amplifying hate speech against certain ethnic groups in the region. Meanwhile, an offshore “Web 3” project with ambitions to build a national ID system in Ethiopia based on a suite of much-hyped blockchain technologies is going virtually unscrutinized by journalists, scholars and activists, even as such a system comes with significant risks for people in Ethiopia and in countries eyeing similar plans.

The project, known as Cardano, is actually run by a cluster of offshore entities — the Swiss-based Cardano Foundation, Hong Kong-based development arm IOHK and Japan-based venture arm EMURGO. Founded and led by the 34-year-old Charles Hoskinson, who previously co-founded Ethereum, Cardano raised more than US$62 million in an offshore initial coin offering from 2015 through 2017 designed to evade the reach of the US Securities and Exchange Commission.

Hoskinson, whose ultimate ambition is to build a national ID system for Ethiopia, recently struck a deal with Ethiopia’s Ministry of Education for a blockchain-based ID pilot involving five million secondary school students. As he describes it, “Every one of these students will have a digital identity — a DID. That DID carries with it information — metadata — that will travel with them throughout their academic life, and follow them into the economic world.”

At present, Ethiopia lacks a national ID system. Instead, it has a highly decentralized system whereby foundational IDs provided at the municipality level known as “kebele cards” can be used to obtain tax IDs, passports and other functional identity documents. It is perhaps ironic that blockchain promoters such as Hoskinson, who aggressively evangelize “decentralization,” would aspire to build a centralized ID scheme on top of a distributed ledger technology. But distributed computing and decentralized power are not the same thing — far from it. In the case of Cardano, a proof-of-stake consensus protocol allows coin holders to vote and influence how the protocol evolves. Ethiopians, of course, have no say. Moreover, rather than decentralize power, the Cardano network itself becomes a single point of failure — if the network goes down, so do all ID systems.

We have countless examples of the dangers of national ID schemes in general, including from Kenya, Uganda, Pakistan, India and elsewhere. But while national ID schemes can be highly problematic, building them on blockchain could be catastrophic. Putting aside the very obvious logistical hurdles, including very low internet penetration rates in Ethiopia (that are significantly lower in more rural regions) and the displacement of children from schools due to ongoing conflict and humanitarian challenges, there are much deeper problems with Hoskinson’s plans. Blockchain is fundamentally an accounting technology designed to track and trace digital assets through an immutable ledger of transactions. Blockchain-based ID schemes similarly treat identity as a transactional, mathematical problem. The more transactions, the more profitable for the network.

There are also serious privacy and data protection concerns with the logging of all this metadata. While proponents of blockchain-based ID claim that concerns are unfounded if the system is designed correctly and identity documents are kept off ledger, the dangers of metadata in this context are well-documented. Hoskinson himself concedes the dangers of blockchain-based ID schemes, saying, “Regimes like China or Saudi Arabia have an onerous record of very significant institutional violations…There, it makes no sense to build identity solutions or blockchain solutions because there’s a high probability that those solutions are going to be abused and weaponized against the population.”

But how naive to ignore the same risks in Ethiopia or elsewhere. How naive to think that regimes will not topple or that political winds will not change. A system easily abused or weaponized anywhere is a threat everywhere. In fact, there is already evidence of identity information being used to target populations in the Tigray conflict. Now imagine the implications of a national ID scheme built on an immutable ledger, driven by commercial incentives and operated by offshore entities. Imagine how much worse Kenya’s “double registration” problem would be or the additional dangers that the Taliban’s seizure of Afghanistan’s biometric database would pose had either system been built on an immutable ledger.

Hoskinson says his mission is to give people in Africa control over their own lives. But in reality, his plans for Ethiopia appear crypto-colonial. As researcher Pete Howson explains, “Innovators are not drawn to fragile states because they want to fix these things. Poverty and corruption are the ideal conditions for entrepreneurs exploring opportunities to extract resources from vulnerable communities.”

Or, as the sociologist Ruha Benjamin has powerfully articulated, “Most people are forced to live inside someone else’s imagination. And one of the things we have to come to grips with is how the nightmares that many people are forced to endure are the underside of an elite fantasy about efficiency, profit, and social control.”

Of course, Hoskinson is not alone. Just as when former child actor and Mighty Ducks-star-turned-cryptocurrency-evangelist Brock Pierce settled in Puerto Rico in the wake of Hurricane Maria’s devastation or when a 27-year-old American bitcoin investor named Jack Mallers persuaded El Salvador’s authoritarian president to make bitcoin legal tender in the country, local populations were not consulted. In fact, there are active and ongoing protests and resistance in El Salvador and in Puerto Rico.

As the conflict rages on in Ethiopia, Cardano enthusiasts are worried about whether it will interrupt the network’s development plans or reduce the value of their cryptocurrency tokens. As for civil society, we should worry about the implications of blockchain-based ID systems and the incentives driving them around the world. Most importantly, we should resist the urge to narrowly scrutinize the technical contours of a given technology or system; we should instead contest the underlying imaginations that shape it, making sure to ask whose imagination it represents."

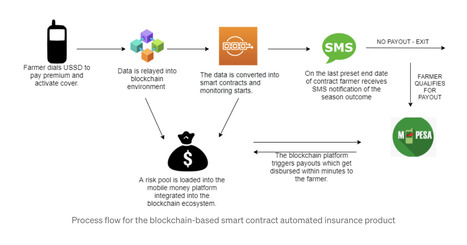

FinX is piloting blockchain smart contracts with existing weather index product to measure the impact on operational costs, payouts, and claim inquiries

"Everyday administrative practices are relatively understudied in research on illiberalism and authoritarianism. This article addresses this gap to account for the neoliberalist and technopopulistic motivations that support illiberal and authoritarian practices in a weak rule of law context. Using narrative analysis, it interprets the role of beliefs and desires of politico-administrative actors in facilitating such actions in the context of India’s public sector digitalisation. This article elaborates how the instrumental rationalities embedded into the design of digitalised policies and their practices at various levels of analysis can erode voluntariness and privacy as well as undercut democratic accountability. This article makes a case for recentering the democratic ethos in designing and implementing digitalised policy regimes to ensure everyday administrative practices are aligned with the need to avoid the infringement of individual freedoms and democratic accountability."

"For Michelle Milkowski, who lives in Renton, Washington, one thing led to another.

Because her son's daycare closed in the early days of the pandemic, she had some extra cash. So, like millions of other people, Milkowski downloaded the Robinhoodtradingapp.

Back then, the stock market was at the beginning of what would become a record-setting run, and Milkowski's new pastime became profitable.

She kept trading shares, but in early 2021, something else caught her eye: Milkowski noticed the value of Bitcoin had reached $60,000.

"I just couldn't believe it," she says, noting she first heard of the popular cryptocurrency in 2016, when its price was less than a hundredth of that. "I felt like I'd just missed the boat, because I could have bought it before it skyrocketed."

Last spring, Milkowski took another look at Bitcoin, and she took a leap. "Better late than never," she remembers thinking.

First, Milkowski bought $500. Then, $10,000. By the end of last year, Milkowski estimates, she had spent close to $30,000 on crypto.

In hindsight, the timing was terrible.

Like many first-time investors, Milkowski bought digital currencies as they were approaching all-time highs, and as companies were spending tens of millions of dollars on marketing to broaden crypto's appeal.

Quarterback Tom Brady and his wife, supermodel Gisele Bündchen, starred in an ad for FTX, and a commercial for Crypto.com featured Academy Award-winning actor Matt Damon.

These were designed to appeal to a potential investor's fear of missing out.

"Fortune favors the brave," Damon says. The ads included little-to-no explanation of crypto, and how risky the unregulated asset is.

About two weeks after that Crypto.com ad debuted, Bitcoin set a new record: $68,990. Today, it's less than a third of that.

Although its backers long claimed it would be a hedge against high inflation, that hasn't proven to be the case...."

"Drawing inspiration from India’s Aadhaar system, the World Bank is promoting a dangerous digital ID model in the name of providing “a legal identity for all.” But rather than providing a model, Aadhaar is merely a mirage—an illusion of inclusiveness, accuracy, and universal identity."

By Jaap van der Straaten

"Last month saw the publication of a report on the World Bank’s ill-conceived approach to digital ID, described as “essential reading for all concerned about human rights and development” by former UN Special Rapporteur on Extreme Poverty and Human Rights Philip Alston. As the press release summarizes:

“Governments around the world have been investing heavily in digital identification systems, often with biometric components (digital ID). The rapid proliferation of such systems is driven by a new development consensus, packaged and promoted by key global actors like the World Bank, but also by governments, foundations, vendors, and consulting firms. This new ‘manufactured consensus’ holds that digital ID can contribute to inclusive and sustainable development—and is even a prerequisite for the realization of human rights.”

The report argues that India’s digital identification system has been central to the formation and promotion of this consensus. This has also been increasingly clear to me in my experience as an economist and identity management consultant who has provided advisory services to the World Bank. For the World Bank—and particularly its Identification for Development (ID4D) cross-sectoral practice—the Indian system, named Aadhaar, has become the singular answer to development and a key source of inspiration. This continues irrespective of the body of evidence which shows how poorly a “fit” the Aadhaar system is for identity management in India, and even more so elsewhere. Aadhaar represents a mirage: it is not evidencing the universality, inclusiveness, unprecedented enrollment speed, meaningful legal identity, nor accuracy that it is claimed to represent.

The World Bank’s own data on the completeness of ID systems displays the “20/80-rule”: the overwhelming odds are that digital ID systems not building on a functional civil registration system (in which births, deaths, marriages and so forth are recorded) will exclude 20% or more of (mostly vulnerable) people, or they will take at least 80 years to cover all. Many developing countries often abandon underperforming ID-systems obtained at great cost, only to launch new and even more sophisticated systems. Instead of using existing service infrastructure for civil registration, new digital ID systems are rolled out through a quick fix “mobile campaign,” held once or twice, with mobile enrollment kits and temporary enrollment staff. But this invariably leaves a coverage and service void behind.

But what about Aadhaar, then? Hasn’t Aadhaar enrolled almost all of the Indian population (1.29 billion by March 2021, out of 1.39 billion), in just a decade (from September 2010), at minimal cost (USD $1.60/enrollment)? If one believes the data from the Unique Identification Authority of India (UIDAI), then yes. But independent data are unavailable; UIDAI controls the message—even the Comptroller and Auditor General of India (CAG) had to use UIDAI data for its first ever audit of Aadhaar. Still, CAG found that UIDAI’s operational and financial management have been utterly deficient. Claims about Aadhaar’s impressive coverage and universality might, then, be questionable. Neither is the database accurate: the Aadhaar system has no way of weeding out dead enrollees (about 80 million in 10 years) or people leaving India (including Indian citizens). CAG also found UIDAI’s digital archiving and its collection and storage of the physical documents that back up enrollments to be inadequate.

Furthermore, claims about the uniqueness guaranteed by biometric technologies within Aadhaar are also illusory. There is no uniqueness for the approximately 25 million children under five years old enrolled in the database. Multiple Aadhaars were issued to the same persons, while different Aadhaar numbers associated with the same biometric data were issued to multiple people. Fingerprint authentication success for 2020-21 was only (an unverifiable) 74-76%. This may well be the canary in the coalmine, indicating exaggerated coverage claims for Aadhaar. Indeed, a Privacy International study explains the very statistical impossibility of a unique biometric profile in a population of 1.39 billion people. Rather, each Indian person has an average of 17,500 indistinguishable biometric “doubles.”

These claims about the benefits of biometrics have far-reaching implications as Aadhaar is linked to other areas of governance. A new law provides for the use of Aadhaar to verify the electoral roll. Weeding out “ghost entries” when the uniqueness and de-duplicated nature of the Aadhaar database is disproved is a doomed exercise, and represents another potential threat to India’s democracy.

Aadhaar’s “big numbers” are a mirage too. Proponents claim that over a billion were newly enrolled at record speed at low cost. But this is not as unprecedented as is suggested. For elections in India, 900 million voters are registered or verified every five years—which tops Aadhaar’s enrollment accomplishment. And India’s bureaucracy has long provided multiple forms of documentation; for proof of identity, date of birth, and address, enrollees can choose from a menu of no less than 106 valid documents. Less than 3 in 10,000 enrollees lacked valid ID prior to Aadhaar enrollment by 2016. The Aadhaar system is a duplication which simply adds on biometrics—which, as we saw, are not the holy grail they are claimed to be. To suggest that other countries, which do not have this multitude of breeder documents and existing enrollment capacities, can copy the Aadhaar approach and obtain widespread coverage, is an illusion.

In respect of claims that Aadhaar brings down costs and increases efficiencies: these costs are applicable only in India. I have found that digital ID systems in many African countries cost 5 to 10 times more per capita than India’s ID system. The high failure rates of ID-systems in many developing countries add to the unbearable costs for poorer countries and their more vulnerable people.

This cries out for a better identity management model—one that is centered around citizenship, with civil registration as the foundation, which seeks to guarantee rights. A model closer to northern European identity management systems comes to mind, or one that is already in use in South Africa. Such systems stand in contrast with Aadhaar, which seeks to side-step the “pesky political issue” of citizenship. This is perhaps the most serious and dangerous element of the mirage: Aadhaar only provides an “economic identity” (with rights limited to government hand-outs, and “voluntary” use for private services), which aims to facilitate economic transactions and private sector service delivery. The UIDAI, then, insists that Aadhaar has “nothing to do with the citizenship issue.”

But Aadhaar’s “citizenship-blindness” is make-believe. Enrollment into Aadhaar was selective in Assam state, for example, where the issuance of digital ID was linked to citizenship determinations. Suddenly, Aadhaar proved to be exclusionary “citizenship ID” after all. Aadhaar has dangerously played into worrying trends, such as the Citizenship Amendment Act and widespread lack of proof of citizenship—all while proponents claim that it is a model of how to achieve “legal identity for all.”

Aadhaar proves to be a mirage that we see while traveling on “the road to hell,” which is paved with imaginary intentions and is leading to a deadly development destination. Its presentation as a “model” digital ID system should be urgently reconsidered."

"A new Trail of Bits research report examines unintended centralities in distributed ledgers

Blockchains can help push the boundaries of current technology in useful ways. However, to make good risk decisions involving exciting and innovative technologies, people need demonstrable facts that are arrived at through reproducible methods and open data.

We believe the risks inherent in blockchains and cryptocurrencies have been poorly described and are often ignored—or even mocked—by those seeking to cash in on this decade’s gold rush.

In response to recent market turmoil and plummeting prices, proponents of cryptocurrency point to the technology’s fundamentals as sound. Are they?

Over the past year, Trail of Bits was engaged by the Defense Advanced Research Projects Agency (DARPA) to examine the fundamental properties of blockchains and the cybersecurity risks associated with them. DARPA wanted to understand those security assumptions and determine to what degree blockchains are actually decentralized.

To answer DARPA’s question, Trail of Bits researchers performed analyses and meta-analyses of prior academic work and of real-world findings that had never before been aggregated, updating prior research with new data in some cases. They also did novel work, building new tools and pursuing original research.

The resulting report is a 30-thousand-foot view of what’s currently known about blockchain technology. Whether these findings affect financial markets is out of the scope of the report: our work at Trail of Bits is entirely about understanding and mitigating security risk.

The report also contains links to the substantial supporting and analytical materials. Our findings are reproducible, and our research is open-source and freely distributable. So you can dig in for yourself.

Key findings

Blockchain immutability can be broken not by exploiting cryptographic vulnerabilities, but instead by subverting the properties of a blockchain’s implementations, networking, and consensus protocols. We show that a subset of participants can garner undue, centralized control over the entire system:

While the encryption used within cryptocurrencies is for all intents and purposes secure, it does not guarantee security, as touted by proponents.

Bitcoin traffic is unencrypted; any third party on the network route between nodes (e.g., internet service providers, Wi-Fi access point operators, or governments) can observe and choose to drop any messages they wish.

Tor is now the largest network provider in Bitcoin; just about 55% of Bitcoin nodes were addressable only via Tor (as of March 2022). A malicious Tor exit node can modify or drop traffic.

More than one in five Bitcoin nodes are running an old version of the Bitcoin core client that is known to be vulnerable.

The number of entities sufficient to disrupt a blockchain is relatively low: four for Bitcoin, two for Ethereum, and less than a dozen for most proof-of-stake networks.

When nodes have an out-of-date or incorrect view of the network, this lowers the percentage of the hashrate necessary to execute a standard 51% attack. During the first half of 2021, the actual cost of a 51% attack on Bitcoin was closer to 49% of the hashrate—and this can be lowered substantially through network delays.

For a blockchain to be optimally distributed, there must be a so-called Sybil cost. There is currently no known way to implement Sybil costs in a permissionless blockchain like Bitcoin or Ethereum without employing a centralized trusted third party (TTP). Until a mechanism for enforcing Sybil costs without a TTP is discovered, it will be almost impossible for permissionless blockchains to achieve satisfactory decentralization.

Novel research within the report

Analysis of the Bitcoin consensus network and network topology

Updated analysis of the effect of software delays on the hashrate required to exploit blockchains (we did not devise the theory, but we applied it to the latest data)

Calculation of the Nakamoto coefficient for proof-of-stake blockchains (once again, the theory was already known, but we applied it to the latest data)

Analysis of software centrality

Analysis of Ethereum smart contract similarity

Analysis of mining pool protocols, software, and authentication

Combining the survey of sources (both academic and anecdotal) that support our thesis that there is a lack of decentralization in blockchains

The research to which this blog post refers was conducted by Trail of Bits based upon work supported by DARPA under Contract No. HR001120C0084 (Distribution Statement A, Approved for Public Release: Distribution Unlimited). Any opinions, findings and conclusions or recommendations expressed in this material are those of the author(s) and do not necessarily reflect the views of the United States Government or DARPA."

"WASHINGTON, D.C – The Atlantic Council published a report titled Designing Decentralized Finance For Financial Inclusion. They specifically note how DeFi projects need to expand their reach to mobile users and improve internet access to achieve financial inclusion. According to their report 90 percent of people who access the internet do it through their smartphone. They note how public private partnerships are essential to this process. Celo’s approach with mobile-first technology, and embedding itself in governmental, corporate and social organizations follows the recommendations the Atlantic Council set out.

Blockchain UBI – How it Works

First, they bring people into the social impact digital economy in the name of humanitarian aid, then lead them to financial applications where all their digital data, linked to their blockchain identity, is used to build credit profiles. Credit profiles and digital twins are synonymous. We tend to think of digital twins as avatars, but at their core they depend on digital identifiers attached to data in a standardized format.

The most successful attempt at building digital twins at Celo occurs though Impact Markets, a private Universal Basic Income initiative targeting the poor. Their stated goal is to eradicate extreme poverty by 2030. Obviously, blockchain UBI did not suddenly give humanity the ability to take care of each other, however blockchain UBI makes it profitable to give people money and provides momentum to the inclusive open air prison.

Impact Markets operates as a ‘DAO’ controlled by the PACT token. DAO is a euphemism for Digital Organization; the decentralized part of the acronym means nothing. A small concentration of token holders, or influence networks, control most significant Digital Organizations.

To receive UBI through Impact Market, an approved community manager from a ‘reputable’ social organization, has to get their community approved by the Digital Organization. Then that manager can add or remove UBI beneficiaries from their community. Each community is approved with different parameters controlling how much and how often communities/beneficiaries can claim from the treasury.

Voters control the network and UBI, including any upgrades or changes to the smart contracts. Voters also control when communities receive donations from the reserves. The following formula determines how much cUSD (celo stablecoin) a community will receive.

"cUSD amount per community = number of beneficiaries * UBI allowance / (Total amount already sent by the DAO to that community / Total raised so far to that community)

In the case of Impact Markets, their governance system is especially centralized. To submit a proposal and reach the threshold to pass a proposal, a user needs 100 million PACT tokens. Only 10 addresses, including three which appear to be non voting smart contracts, hold over 100 million PACT. Every proposal I saw passed through the vote of a single token holder.

On the ground ‘Ambassadors’ based in a country, cultivate community managers and identify areas of potential. They plan to create a sub committee of ambassadors which will handle community on/off boarding in a more scalable way. Since they aim to reach a million people by 2022, and eradicate extreme poverty by 2030, continuous expansion is essential.

To actually create the communities, and access the UBI, people have to connect the Valora mobile app to the Impact Market app. As a reminder, the Valora app is connected to people’s phone numbers and is the primary interface to interact with Celo on a phone.

Donors also receive the PACT token. A recently launched initiative called impact farming allows PACT holders to stake the token in order to earn more PACT rewards when they donate. Marco Barbosa, founder and CEO of Impact Market, describes their tokenomics as aligning incentives in a way that the PACT token appreciates in price as Impact Makerks reaches more people.

In September of 2020 Impact Markets began operations in Brazil. Within their first year they onboarded over 12,000 people."...

... "House Financial Services Committee U.S. House of Representatives Washington, D.C. 20510

Dear U.S. Congressional Leadership, Committee Chairs and Ranking Members,

We are 1500 computer scientists, software engineers, and technologists who have spent decades working in these fields producing innovative and effective products for a variety of applications in the fields of database technology, open-source software, cryptography, and financial technology applications.

Today, we write to you urging you to take a critical, skeptical approach toward industry claims that crypto-assets (sometimes called cryptocurrencies, crypto tokens, or web3) are an innovative technology that is unreservedly good. We urge you to resist pressure from digital asset industry financiers, lobbyists, and boosters to create a regulatory safe haven for these risky, flawed, and unproven digital financial instruments and to instead take an approach that protects the public interest and ensures technology is deployed in genuine service to the needs of ordinary citizens.

We strongly disagree with the narrative—peddled by those with a financial stake in the crypto-asset industry—that these technologies represent a positive financial innovation and are in any way suited to solving the financial problems facing ordinary Americans.

Not all innovation is unqualifiedly good; not everything that we can build should be built. The history of technology is full of dead ends, false starts, and wrong turns. Append-only digital ledgers are not a new innovation. They have been known and used since 1980 for rather limited functions.

As software engineers and technologists with deep expertise in our fields, we dispute the claims made in recent years about the novelty and potential of blockchain technology. Blockchain technology cannot, and will not, have transaction reversal or data privacy mechanisms because they are antithetical to its base design. Financial technologies that serve the public must always have mechanisms for fraud mitigation and allow a human-in-the-loop to reverse transactions; blockchain permits neither.

By its very design, blockchain technology is poorly suited for just about every purpose currently touted as a present or potential source of public benefit. From its inception, this technology has been a solution in search of a problem and has now latched onto concepts such as financial inclusion and data transparency to justify its existence, despite far better solutions to these issues already in use. Despite more than thirteen years of development, it has severe limitations and design flaws that preclude almost all applications that deal with public customer data and regulated financial transactions and are not an improvement on existing non-blockchain solutions.

Finally, blockchain technologies facilitate few, if any, real-economy uses. On the other hand, the underlying crypto-assets have been the vehicle for unsound and highly volatile speculative investment schemes that are being actively promoted to retail investors who may be unable to understand their nature and risk. Other significant externalities include threats to national security through money laundering and ransomware attacks, financial stability risks from high price volatility, speculation and susceptibility to run risk, massive climate emissions from the proof-of-work technology utilized by some of the most widely traded crypto-assets, and investor risk from large scale scams and other criminal financial activity.

We implore you to take a truly responsible approach to technological innovation and ensure that individuals in the US and elsewhere are not left vulnerable to predatory finance, fraud, and systemic economic risks in the name of technological potential which does not exist.

The catastrophes and externalities related to blockchain technologies and crypto-asset investments are neither isolated nor are they growing pains of a nascent technology. They are the inevitable outcomes of a technology that is not built for purpose and will remain forever unsuitable as a foundation for large-scale economic activity.

Given these vast externalities, together with the—at best still-ambiguous and at worst non-existent—uses of blockchain, we recommend that the Committee look beyond the hype and bluster of the crypto industry and understand not only its inherent flaws and extraordinary defects but also the litany of technological fallacies it is built upon.

We need to act now to protect investors and the global financial marketplace from the severe risks posed by crypto-assets and must not be distracted by technical obfuscations which mask an abject lack of technological utility. We thank you for your leadership on financial technology and regulation and urge you to consider our objective and independent expert judgments to guide your legislative priorities, which we remain happy to discuss anytime.

The resources offered here were chosen by the authors of this letter as useful reference material only. The inclusion of a paper and/or author in this list does not constitute an endorsement of this letter of our views.

Allen, Hilary. 2022. Driverless Finance. Oxford University Press.

Chancellor, Edward. 1999. 'Devil Take the Hindmost: A History of Financial Speculation'.

Dhawan, Anirudh, and Tālis J Putniņš. 2020. 'A New Wolf in Town? Pump-and-Dump Manipulation in Cryptocurrency Markets'. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.3670714.

Dywer, Gerald P. 1996. 'Wildcat Banking, Banking Panics, and Free Banking in the United States', 20.

Foley, Sean, Jonathan R Karlsen, and Tālis J Putniņš. 2019. 'Sex, Drugs, and Bitcoin: How Much Illegal Activity Is Financed through Cryptocurrencies?' The Review of Financial Studies 32 (5): 1798-1853.

Hamrick, JT, Farhang Rouhi, Arghya Mukherjee, Amir Feder, Neil Gandal, Tyler Moore, and Marie Vasek. 2018. 'An Examination of the Cryptocurrency Pump and Dump Ecosystem'. http://ssrn.com/paper=3303365.

Hanley, Brian P. 2018. 'The False Premises and Promises of Bitcoin'. ArXiv:1312.2048 [Cs, q-Fin], July. http://arxiv.org/abs/1312.2048.

Hockett, Robert C. 2019. 'Money's Past Is Fintech's Future: Wildcat Crypto, the Digital Dollar, and Citizen Central Banking'.

Kindleberger, Charles P, Panics Manias, and A Crashes. 1996. 'History of Financial Crises'. Wiley, New York.

Steele, Graham. 2021. 'The Miner of Last Resort: Digital Currency, Shadow Money and the Role of the Central Bank'. Technology and Government, Emerald Studies in Media and Communications, Forthcoming.

"An 18-year-old graduate student exploited a weakness in Indexed Finance’s code and opened a legal conundrum that’s still rocking the blockchain community. Then he disappeared."

By Christopher Beam

"On Oct. 14, in a house near Leeds, England, Laurence Day was sitting down to a dinner of fish and chips on his couch when his phone buzzed. The text was from a colleague who worked with him on Indexed Finance, a cryptocurrency platform that creates tokens representing baskets of other tokens—like an index fund, but on the blockchain. The colleague had sent over a screenshot showing a recent trade, followed by a question mark. “If you didn’t know what you were looking at, you might say, ‘Nice-looking trade,’ ” Day says. But he knew enough to be alarmed: A user had bought up certain tokens at drastically deflated values, which shouldn’t have been possible. Something was very wrong.

Day jumped up, spilling his food on the floor, and ran into his bedroom to call Dillon Kellar, a co-founder of Indexed. Kellar was sitting in his mom’s living room six time zones away near Austin, disassembling a DVD player so he could salvage one of its lasers. He picked up the phone to hear a breathless Day explaining that the platform had been attacked. “All I said was, ‘What?’ ” Kellar recalls.

They pulled out their laptops and dug into the platform’s code, with the help of a handful of acquaintances and Day’s cat, Finney (named after Bitcoin pioneer Hal Finney), who perched on his shoulder in support. Indexed was built on the Ethereum blockchain, a public ledger where transaction details are stored, which meant there was a record of the attack. It would take weeks to figure out precisely what had happened, but it appeared that the platform had been fooled into severely undervaluing tokens that belonged to its users and selling them to the attacker at an extreme discount. Altogether, the person or people responsible had made off with $16 million worth of assets.

Kellar and Day stanched the bleeding and repaired the code enough to prevent further attacks, then turned to face the public-relations nightmare. On the platform’s Discord and Telegram channels, token-holders traded theories and recriminations, in some cases blaming the team and demanding compensation. Kellar apologized on Twitter to Indexed’s hundreds of users and took responsibility for the vulnerability he’d failed to detect. “I f---ed up,” he wrote.

The question now was who’d launched the attack and whether they’d return the funds. Most crypto exploits are assumed to be inside jobs until proven otherwise. “The default is going to be, ‘Who did this, and why is it the devs?’ ” Day says.

As he tried to sleep the morning after the attack, Day realized he hadn’t heard from one particular collaborator. Weeks earlier, a coder going by the username “UmbralUpsilon”—anonymity is standard in crypto communities—had reached out to Day and Kellar on Discord, offering to create a bot that would make their platform more efficient. They agreed and sent over an initial fee. “We were hoping he might be a regular contributor,” Kellar says.

Given the extent of their chats, Day would have expected UmbralUpsilon to offer help or sympathy in the wake of the attack. Instead, nothing. Day pulled up their chat log and found that only his half of the conversation remained; UmbralUpsilon had deleted his messages and changed his username. “That got me out of bed like a shot,” Day says.

He shared his suspicions with the team, who over the next few days combed the attacker’s digital trail. They discovered that the Ethereum wallet used to transfer tokens during the attack was connected to another wallet used to collect winnings in a recent hacking contest by a participant who sometimes identified himself as UmbralUpsilon. Pulling up the participant’s registration, they saw that it linked to a profile on the collaborative coding platform GitHub.

The GitHub profile had been created by someone whose email address began with “amedjedo” and was associated with a domain owned by a public school board in Ontario. Day and his colleagues also found a Wikipedia contributor with a username similar to the one on GitHub. The Wikipedia editor had once altered the page for a popular Canadian quiz competition for high school students, adding a name under “Alumni”: “Andean Medjedovic, notable mathematician.” Google filled in the rest. Medjedovic had until recently been a master’s student at the University of Waterloo in Ontario, specializing in mathematics. His résumé said he had an interest in cryptocurrency.

The team breathed a sigh of relief. Once cyberattackers have been identified, they often return funds in exchange for a face-saving bounty and credit for being a “white hat” hacker. Day had already contacted UmbralUpsilon to offer a 10% reward for the tokens’ safe return, striking a note of grudging praise—“well played,” he wrote—but hadn’t heard back. So Kellar tried a different tactic, messaging Medjedovic and addressing him as “Andean.” This time Medjedovic reacted, taunting Indexed users publicly on Twitter: “You were out-traded. There is nothing you can do about that. … Such is crypto.” When a team member emailed him independently, saying that if he returned the tokens they’d pay him $50,000, Medjedovic responded with a link to an Ethereum address. “Send the money over,” he wrote. They didn’t take the bait from their tormentor—who they’d learned, to their astonishment, was only 18 years old.

Finally Kellar texted Medjedovic to make one last plea before, he said, they would be forced to bring in lawyers and police. “I implore you to give up now and make this easy on yourself,” he wrote. The teenager responded with “Xdxdxd,” an emoticon that evokes dying of laughter, and added, “Best of luck.”

When Kellar and his co-founders created Indexed, they imagined it as a step forward for DeFi, or decentralized finance, a blockchain-based movement that purports to offer a more automated, less intermediated version of borrowing and lending, asset trading, and portfolio management. Some proponents take a utilitarian view of DeFi, considering it an improved version of traditional finance, with its fee-taking middlemen and sluggish human decision-making. Others are more libertarian, seeing DeFi as an escape from the existing system, a way of circumventing the rules and restrictions imposed by governments or corporations. Then there are the skeptics, who think it’s all a grift.

Kellar, who describes himself as “very progressive,” fits squarely into the utilitarian camp. At age 23, after dropping out of the University of Texas at Dallas when computer science classes weren’t teaching him anything new, he started Indexed to solve a problem: What if you wanted to trade crypto but didn’t want the daily hassle of managing a portfolio?

In traditional finance, investors who want a wide, balanced array of stocks can purchase shares of index funds, outsourcing the day-to-day job of buying and selling the stocks to a portfolio manager. Kellar went about creating a similar arrangement on the blockchain, but with an algorithm driving the trading. Whereas an index fund manager would maintain a portfolio containing the underlying assets of an index share, the Indexed algorithm maintained a “pool” of underlying tokens for each index token. Users could swap one or all of the underlying assets into the pool in exchange for an index token—a process called “minting.” They could likewise “burn” an index token by trading it back into the pool in exchange for one or all of the underlying assets. Or, as with an exchange-traded fund, users could simply buy or sell index tokens on decentralized exchanges such as Uniswap.

Index funds take various forms, each with a different investment strategy. Some, such as the S&P500, are market-capitalization-weighted: If the value of one of its stocks goes up, the proportional value of that stock within the portfolio rises accordingly. Others seek to maintain a fixed balance of stocks. For example, if you wanted Microsoft shares to consistently make up 20% of your portfolio, and the value of the stock went up, the portfolio manager would sell shares of Microsoft to maintain its 20% weight.

Kellar and his team modeled Indexed on that type of fund, using a mechanism called an “automated market-maker” to maintain the balance of underlying assets, as many DeFi platforms do. Unlike a traditional market-maker, the AMM wouldn’t buy and sell assets itself; instead it would help the pool reach its desired asset balance by adjusting the “pool price” of component tokens to give traders an incentive to buy them from the pool or sell them into it. When the pool needed more of a particular token, its price within it would rise; when the pool needed less, the price would decline. This model assumed users would interact rationally with the protocol, buying low and selling high.

By eliminating human managers, Indexed could forgo management fees like the 0.95% its bigger rival, Index Coop, charged for simply holding its most popular index token. (Indexed would charge a fee for burning tokens and swapping assets within a pool, but those only applied to a small fraction of users.) It also saved on costs by limiting the number of interactions between the platform and outside entities. For example, when Indexed needed to calculate the total value held within a pool, instead of checking token prices on an exchange such as Uniswap, it sometimes extrapolated from the value and weight of the largest token within the pool, called the “benchmark” token. This way, it reduced the fees it paid for transactions on the Ethereum blockchain. Kellar saw full passivity as a “natural extension of the way index funds already operate.”

But passivity also created risk. If there was a problem with the code, someone could exploit it directly, without needing to bypass any human safeguards. And limiting blockchain interactions to cut costs entailed a trade-off: When a smart contract—a script that executes automatically when certain criteria are met—has fewer steps, it can leave more room for security vulnerabilities. The list of exploited crypto platforms is long and grows by the week: Poly Network, Wormhole, Cream Finance, Rari Capital, and many more. “There’s a common saying in DeFi that there are two types of protocols,” Day says. “Those that have been hacked and those that are going to be hacked.”...

"A closer look at the LooksRare platform that has quickly become the leading NFT marketplace by trading volume shows that most of the activity is actually users selling tokens to themselves to help earn rewards in the form of more coins.

The platform was launched in January by two anonymous co-founders -- who go by Zodd and Guts -- as an alternative to market leader OpenSea during the height of the NFT boom."....

Valerie Strauss "There is an emerging financial phenomenon in the education and social service world that could change the way social services are delivered in the United States — and who gets them. The term that describes a number of different programs in this arena are social impact bonds, and if you have managed not hear about them in recent years as they have been developed, now’s a good time to learn. What are these bonds?