Follow, research and publish the best content

Get Started for FREE

Sign up with Facebook Sign up with X

I don't have a Facebook or a X account

Already have an account: Login

Social Impact Bonds, "Pay For Success," Results-Based Contracting, and Blockchain Digital Identity Systems

2.3K views |

+0 today

Social Impact Bonds (SIBs) are a private financing mechanism used to fund social programs. Also termed 'Pay For Success,' and 'Outcomes Based' or 'Performance Based' financing, these partnerships involve private entities funding projects aimed at improving social outcomes. If by the end of the project period, 'success' metrics are met (according to third-party evaluators), investors then profit by being paid interest on top of the reimbursed government funds for the cost of the project. This page includes a collection of updates and critical perspectives on these profit structures and on Blockchain Identity systems, de-centralized online ledger programs, poised to be the data backbone that would provide 'proof' of 'program impact' for investors. For files related to Blockchain, see: http://bit.ly/Blockchain_Files. [Note: Views presented on this page are re-shared from external websites and may not necessarily represent the views nor official position of the curator nor employer of the curator.]

Curated by

Roxana Marachi, PhD

Your new post is loading...

Your new post is loading... Your new post is loading...

Your new post is loading...

"A social policy experiment is spreading across the country as a new way to finance, deliver, and improve public services and problems. But its merits are so far unproven.

The reason for the program’s demise has to do with another feature of the experiment: It was financed entirely with a $9.6 million loan from Goldman Sachs. New York City was to pay the investment firm back if the repeat offense rate went down by at least 10 percent over four years. In June, a preliminary report showed the program not only was missing its recidivism target, it had no impact on the rate altogether. Goldman Sachs moved swiftly and took a contract option to cancel the program one year early. The first social impact bond program in the United States has officially failed.

“Everyone went into this understanding what they were getting into,” says David Butler, a senior adviser at MDRC, a nonprofit social policy research organization that managed the treatment program at Rikers. “These things are risks. Just because something works in one environment doesn’t mean it will work somewhere else.”

Media outlets have often touted the innovative financing tool with few notes about the complicated nature of the projects. Last year on Capitol Hill, where bipartisan support is famously elusive these days, a $300 million proposal pushed by President Obama to allocate federal funds for social impact bond projects in the states managed to attract proponents on both sides of the aisle.

But as the enthusiasm for social impact bonds has grown, so has skepticism about the concept of partnering with the private sector to accomplish social goals. Last spring, a congressional hearing on the subject ended on a negative note as critics questioned the complicated structure of program contracts between governments, investors and the various private operators involved. “I don’t get this at all,” said Maine independent Sen. Angus King, squinting with disbelief. “I think this is an admission that government isn’t doing what it’s supposed to do. This strikes me as a fancy way of contracting out.”...

For full post see: http://www.governing.com/topics/finance/gov-social-impact-bonds.html

"Pay for Success" and social impact investing are poised to take over the public sector, imposing online service delivery and expansive data collection on all aspects of our lives. This 10-minute video offers a crash course on what you need to know right now."

To view within page, scroll down over the slides. To download slides as a pdf, click on title or arrow above, or here: https://wrenchinthegears.files.wordpress.com/2017/11/gambling-on-our-futures1.pdf

For blogpost and video narration of the slidedeck, see:

Click title or arrow above to download. https://datajustice.files.wordpress.com/2017/12/data-harm-record-djl2.pdf

See also https://datajusticelab.org/

"Sharing is good and necessary. But the super-wealthy hide a rigged system behind their “generosity”

By Sammy Kayes Our society is inhumane. Depending on who you are — depending on who your parents are, and what your identity is — you will have a different amount of basic rights and social power in comparison to the others around you. Sometimes, the differences will be stark and significant. You may have to work your heart out just to get by. Or you may never have to work a day in your life. It depends, mostly, on the luck of your birth: where and when you were born, and again, especially, who your parents are.

It’s why you should give a few dollars here, a few dollars there — when someone asks who is clearly in need. It’s why charitable organizations — legitimate ones that offer food, shelter, and comfort — are good. In our unfair world, and our unequal society, this is necessary. But do not confuse this with philanthropy. While there is an element of “giving” within philanthropy, it is something fundamentally different than simply helping, sharing, and caring. It is not even the same as simple “charity.”

On the whole, philanthropy is an exercise of political and economic power. It is something that maintains the status quo — the current political and economic system — and bolsters the already powerful and privileged. Philanthropy is used to mask our state of vast inequality, and is used consistently for other self-serving purposes, like tax evasion, control over foreign resources, and even co-opting of social programs and entire sectors of government for one’s own purposes. Philanthropy is a tool that is used to shift decisions that should be made democratically, by the public, into the hands of a few individuals. The decisions made by these few individuals often end up being incredibly wasteful, and just as often, considerably harmful, to those who are the target of that philanthropy.

Let me give you some examples. In the wake of Hurricane Maria, Puerto Rico residents are now fighting privatization efforts from entrepreneurs — assisted by the Trump administration. The door was opened by a call for generous, philanthropic makeover. It is similar to the Clinton Foundation’s philanthropy in Haiti, following a devastating earthquake. The foundation stepped in to help rebuild the place, but as determined by the locals themselves, the philanthropic organization left Haiti largely the same as before, or even worse. And they made a lot of money for themselves in the process. There is a similar precedent in Hurricane Katrina which flooded New Orleans in 2005, and lead to “generous” philanthropists moving in like vultures to privatize their public school system. Bill Gates is another example of simple wastefulness, and also harm, through philanthropy. Bill Gates dumped hundreds of millions of dollars into the UN Health Agency, and then, of course, insisted that the funds be used in the way he wanted them to be used.

It wasn’t just a gift from the heart. It was also a stubborn decision, a decision that should have been made, probably, by other people. Bill Gates and his philanthropic foundation have done many of these little experiments, in different areas, from health to education. Linsey McGoey calls it The Philanthropy Hustle. And she uses a more appropriate term for modern philanthropy, called “philanthro-capitalism.”

Through philanthro-capitalism, Bill Gates has supported corporate agriculture giant Monsanto — against the will of small farmers and local ecosystems, and at their expense."...

For full article, please see: https://extranewsfeed.com/charity-is-nice-philanthropy-is-a-facade-30c6c1c1d7df

Social Impact Bonds are so popular that politicians try to score points by including them in their campaign platforms. But is there a “there” there yet?"...

For full post, see:

"By David Bank Green bonds have grown into a more than $40 billion annual market, while social-impact bonds have had trouble getting out of the starting gate. It doesn't help when early and high-profile offerings not only fail to deliver returns to investors, but fail to deliver the social impact that the bonds were designed to finance in the first place. Last week's news that the plug had been pulled on the first U.S. social impact bond, or SIB, shook up the nascent marketplace. The failure of the New York City project, launched in 2012 to reduce the rate at which juvenile offenders go back to jail after release from Riker's Island, followed last year's report that the Peterborough, England, granddaddy of all social impact bond-financed projects, failed to meet the 10 percent recidivism-reduction targets needed to repay investors, though it did show an 8.3 percent drop. I haven't had the chance to dig in as deeply as is necessary to piece the full story together. Some of the details will have to come from New York City reporters and bloggers who know their way around City Hall and the ongoing scandals at Rikers Island and can reconstruct how the project came unglued. For impact investors, the important question is what can be learned for future SIBs, which account for less than 1 percent of impact assets under management, according to a recent report. The New York City project was always a chronicle of a death foretold. It was intended by then-Mayor Michael Bloomberg as a conversation-starter and demo of a concept that could be picked up elsewhere. From its initiation by the mayor's offices, through its underwriting at Goldman Sachs, to its loss-guarantee of more than 75 percent by Bloomberg Philanthropies, is was one-of-a-kind. One of the outcomes of the deal is that the billionaire's Bloomberg Philanthropies will now cut a $6 million check to Goldman Sachs to repay three-quarters of the bank's investment in the program. Goldman took a $1.2 million (or 17 percent) loss on a $7.2 million investment. If the program had continued for a fourth year, Goldman's exposure would have increased to $2.4 million, or 25 precent, as the loss-guarantee from Bloomberg Philanthropies dropped to 75 percent (or $7.2 million). (Note: The New York City project shouldn't be confused with a separate social-impact bond sponsored by New York State that also aims to reduce recidivism. The state project, financed with $13.5 million raised from investor by Bank of America Merrill Lynch and launched last year, was the subject of ImpactAlpha's piece last December, “Rebuilding Lives, Reducing Costs: Social Impact Bond Finances Jobs Not Jail.” More on the differences between the projects below.) Change of Plans The program's fate may have been sealed even before it began when the operator originally sought to run the program was replaced on the eve of the financing. One person in a position to know told me back in 2012 that Linda Gibbs, then deputy mayor of health and human services (and now a principal at Bloomberg Associates) had reached out to Barbara Gunn, president and CEO of Structured Employment Economic Development Corp., or Seedco, to run the program. Seedco was widely reported as a Bloomberg administration favorite. And Andrea Phillips, the Goldman vice president who led the social-impact bond financing, had previously been president of Seedco Financial, a community development financial institution (CDFI) that was spun off from Seedco to provide capital to small businesses and nonprofits in disadvantaged communities, and before that, executive vice president for programs at Seedco. Then Manhattan U.S. Attorney Preet Bhahara filed civil fraud charges against Seedco for filing false reports of job placements to meet goals of a separate federal contract contract goals. “How could you trust Seedco to run a program about measurement and results, when they're in paper for cheating on the test?” this person said at the time. “So Seedco was quietly let go.” (Seedco paid a $1.7 million fine and six agency managers settled with the government. The trial of a seventh ended in April with the jury finding one manager accountable for a small number of false placement reports.) When the deal was announced, MDRC, more of an advisory and intermediary than an operator, was named to run the program. The Vera Institute of Justice, a research and technical assistance organization, was selected as the evaluator. “Vera and MDRC are in non-typical roles,” said my source, whom I'm leaving unnamed since the conversation was so long ago. “They're not in the seats you'd expect to see them.” Scaling Challenges The principals are not saying much beyond their official statements. MDRC said it contracted with The Osborne Association, which ran the program in collaboration with Friends of Island Academy. Instead of a jobs program, the groups offered Cognitive Behavioral Therapy (CBT) and in particular, Moral Reconation Therapy (MRT). MDRC says those programs had proven effective elsewhere, but “had never been implemented at scale in as challenging an environment as Rikers,” and detailed some of the obstacles. On its website, MDRC describes itself as an “intermediary” that designs, evaluates and offers technical assistance “to build better programs and deliver effective interventions at scale.” Vera compared “recidivism bed days” for 16- to 18-year-olds eligible to participate in the program in 2013 with a similar group of Rikers' prisoners from 2006 to 2010, before the program was established. The program reached most of its target population, and 44 percent of participants hit at least one milestone but concluded bluntly, “The program did not lead to reductions in recidivism for participants.” That is, unlike the Peterborough pilot, the New York City program did not show any statistically significant reduction in recidivism. In the Huffington Post, Phillips, who leads Goldman's Urban Investment Group, and James Anderson, who leads Bloomberg Philanthropies' government innovation portfolio, put on a brave face to say, in effect, the patient died and the operation was a success. They acknowledged the “evidence-based cognitive behavioral therapy that's been effective in reducing recidivism in many other correctional settings, did not work at Rikers Island.” But Anderson and Phillips stress that as a public-private partnership to test an innovative model, the program actually succeeded. “And we can now say that this unique financing model made it all happen — and stands ready to help public sector leaders finance more efforts to better serve people who need support and better results.” Increased Scrutiny Talking points from other proponents of social-impact bonds, or pay-for-success contracts as they're more accurately called, also said the pilot demonstrated the essential aspect of social-impact bonds: that risks are borne by private investors, not taxpayers. On its PayForSuccess.org site, the Nonprofit Finance Fund stated, “Taxpayers did not pay for a program that appears not to have generated the desired outcomes set out at the pilot’s launch. That risk was borne by investors willing to put their capital at risk for the sake of demonstrating whether a social program achieved a societally beneficial result.” “Great to see stakeholders happy but have we learned WHY this SIB failed?” tweeted Cathy Clark, director of the CASE Initiative on Impact Investing at Duke University and author of The Impact Investor. “Where is story on intervention learning?” The end of the Rikers Island program puts other social-impact bond-financed projects under increased pressure to deliver. Investors in the New York State anti-recidivism SIB, including former Treasury Secretary Larry Summers, will be closely watching for the results of that program, which target older ex-offenders returning from state prison and offered job training and job placement. Goldman Sachs itself has invested in three other social impact bonds, including to tackle early childhood education in Utah and Chicago and homelessness in Massachusetts, that will report some results later this summer. Other financial institutions are also underwriting deals. Bills have been introduced in the Senate and House to target federal dollars to social impact bonds. It's too early to say the bloom is off the rose for social-impact bonds. The New York City experience may say more about the challenges in helping ex-offenders avoid the revolving door back to prison than it does about the efficacy of social-impact bond financing. Most early SIB investors are interested less in the financial returns than in the promise of early intervention to address chronic social challenges. If those promises fall flat, so too may the innovative financing model that has so far produced more fanfare than results."

http://impactalpha.com/the-prison-reform-fail-that-shocked-the-social-impact-bond-market/

By Emily Talmage "This week, the announcement of a massive collaborative between the world’s largest foundations and their philanthropic underlings underscored a disturbing and growing trend among America’s billionaire elite: the use of unprecedented levels of wealth to remake social policy.

If you’re one of those kindhearted Americans who still believes that the nation’s richest families are simply giving away their wealth to little people like us because they care, allow me to do this:

[image of balloon bursting]

Private foundations have long been used as tax-havens for the elite, but “philanthropy” has lately been retooled to serve a new function: the seeding of a new “social capital” marketthat has the potential to reap these self-proclaimed lovers-of-humanity billions of dollars in profit.

This new market, still in the works but advancing at lightning speed, relies on the complete undoing of the public sphere.

That whole Bill-Gates-Common-Core thing? Sure, he wanted everyone to have to buy his Microsoft products… but not as much as he wanted to build a data-tagging system that he and his cronies could use to “measure” and then profit off the “impact” of their investments.

Data is king in the new social capital markets, which is why it’s no coincidence that Congress is currently ramming through several bills expanding the role of the Feds to collect and aggregate data on pretty much everything, starting from when you’re a neonate. And maybe even more creepily, when it comes to “evidence-based policy”, it turns out that “evidence” doesn’t actually mean science or truth or even what’s remotely good for us.

Evidence means data, which can be p-hack’ed (massaged, if you will) anyway investors like.

And so we have folks like Tripp Jones of Massachusetts calling for an expansion of “evidence-based policy” while children die at alarming rates in his former for-profit foster care program; folks like Bill Gates relentlessly terrorizing the public school system in pursuit of an investment-friendly sector; and the folks who managed to balloon the national student debt to astronomical levels advancing new credentialing systems and grading systems…

…all under the guise of philanthropy."...

https://emilytalmage.com/2017/11/16/we-need-to-talk-about-our-philanthropy-problem/

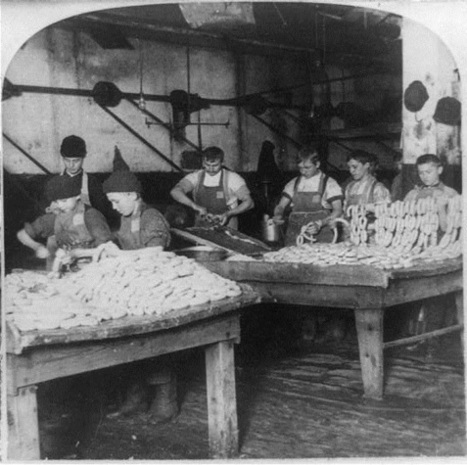

"When you think of child exploitation, what do you think of? A grimy basement filled with whirring sewing machines and silent children, toiling for an evil, shouting, and unshaven boss with a grease-stained shirt and a belt in his hand? Or little boys stuffing sausages in a frigid, unsanitary, meatpacking operation from over a century ago – like in the picture above? At least something like that, right?

How about high-stakes testing and high-pressure ‘evaluations’ of 5, 6, and 7 year-olds?

This is one story of how child labor has made its’ way into the 21st century: the wealthiest Americans are pinning their investment returns on children’s pre-kindergarten, 1st, and 2nd grade performance.

In Chicago, these new, sophisticated child exploiters are celebrated and honored, receiving praise and patronage from politicians, and minimal scrutiny from the press – but make no mistake, they are the same child exploiters, repackaged. Is this child labor 2.0™?

Indeed, what seems to be drowning out the cries of Chicago’s children is the clinking sound of champagne glasses in the halls of Chicago’s elite.

Why are teachers and education professionals removed entirely from these for profit early education schemes? Could it be because these investments are terrible for kids and teachers? Why do the richest people in the United States want to make money off of the work of Chicago 5 year-olds? On November 5th, the Chicago City Council approved a $17 million loan to the Chicago school board from a group of finance capitalists, which will allow the city to expand its’ pre-kindergarten slots by about 2,600 kids.

The lenders are guaranteed to make a killing from their investment – up to $30 million – but only as long as the little kids can be forced to produce results.

It is not a stretch to say that the most powerful finance capitalists in the world are dead-set on undermining education in the public interest. For years, these vampires have been making massive amounts of money at the expense of Chicago schools in scams such as auction-rate securities, which allow Goldman Sachs and their buddies at Bank of America to steal and/or gamble away up to $100 million of the public’s money. I guess when you can steal that kind of dough, why not get into the harder stuff – why not get into tying your profits directly to the performance of school kids?

Goldman Sachs (the most powerful finance firm in America,) Northern Trust (which financially represents 20% of America’s richest families,) and the Pritzker billionaires (Hyatt hotels, Royal Caribbean cruise lines, etc.,) have instituted what they call a Social Impact Bond, designed to generate wealth based on the hard work of preschoolers. Taking their orders from The Most Corrupt Man In Chicago – Mayor Rahm Emanuel – the rubber stamp city council voted the measure through with little debate, which is perhaps the strongest argument for their wholesale replacement (only five no votes against the scam).

So, if the politicians, newspapers, and TV stations are going to stop short of saying it, let me make this clear: There is an epic crime afoot in Chicago – Tying profits to the work of children is a violation of child labor laws.

“This hasn’t swept the nation yet, but this is part of the wave that’s coming,” – JB Pritzker, “industrial sector” billionaire, on his plans to make millions off of child labor. Glowing coverage of the child labor outfit at chicagobusiness.com.

Millions in cash transfers with names like, “Kindergarten Readiness Payments” and “Third Grade Literacy Payments,” will be funneled directly from public funds to the banks’ escrow account. I couldn’t make this up.

Emanuel’s cowed neoliberal defenders may argue that this technically isn’t a legal conspiracy to commit crimes against minors. However, in political, civil, – and most assuredly – in moral terms, what I’ve just described cannot be characterized as anything other than child labor violations.

Why has the press allowed this scam to be described in glowing terms by the establishment (from the Mayor to The Civic Federation,) with no questions about how this is the very definition of child exploitation?

It doesn’t take a genius to know that when Goldman Sachs starts going after little children in Chicago, you can’t for a minute consider yourself safe. No matter where you live."...

For full post, see: https://mediacolossus.wordpress.com/2014/11/08/19th-child-labor-repackaged-for-21st-century-chicago/

Picture caption: Before our unions smashed child labor, founder of Northern Trust, Armour and Co. ruthlessly exploited children for gain in their meatpacking business – now they would like to “educate” your toddlers for profit. Northern Trust is a partner in the new pre-k initiative.

"Digital Classrooms as Data Factories" [Part 2 of 7 in the Series: Education in the Cloud. Introduction at: https://wrenchinthegears.com/2017/07/13/smart-cities-social-impact-bonds-public-educations-hostile-takeover-part-ii/]

Slides also available on SlideShare at https://www.slideshare.net/MollySumner/digital-classrooms-as-data-factories and can be downloaded by clicking title or arrow above.

|

By Emily Talmage "Across the country, teachers are being asked to collect, record, and slog through mountains of data that "experts" insist is meant to improve their practice. There are pre-assessments and post-assessments, habits of work rubrics, writing prompts, social and emotional screeners, standards-based grading systems, RTI data, student learning objectives, professional growth goals, student surveys, self evaluations,…" For full post, please see:

By Steve Denning "It is clear to anyone who has studied the financial crisis of 2008 that the private sector’s drive for short-term profit was behind it. More than 84 percent of the sub-prime mortgages in 2006 were issued by private lending. These private firms made nearly 83 percent of the subprime loans to low- and moderate-income borrowers that year. Out of the top 25 subprime lenders in 2006, only one was subject to the usual mortgage laws and regulations. The nonbank underwriters made more than 12 million subprime mortgages with a value of nearly $2 trillion. The lenders who made these were exempt from federal regulations. How then could the Mayor of New York, Michael Bloomberg say the following at a business breakfast in mid-town Manhattan on November 1, 2011? It was not the banks that created the mortgage crisis. It was, plain and simple, Congress who forced everybody to go and give mortgages to people who were on the cusp. Now, I'm not saying I'm sure that was terrible policy, because a lot of those people who got homes still have them and they wouldn't have gotten them without that. But they were the ones who pushed Fannie and Freddie to make a bunch of loans that were imprudent, if you will. They were the ones that pushed the banks to loan to everybody. And now we want to go vilify the banks because it's one target, it's easy to blame them and Congress certainly isn't going to blame themselves.”

Barry Ritholtz in the Washington Post calls the notion that the US Congress was behind the financial crisis of 2008 “the Big Lie”. As we have seen in other contexts, if a lie is big enough, people begin to believe it.

Even this morning, November 22, 2011, a seemingly smart guy like Joe Kernan was saying on CNBC’s Squawkbox, “When the losses at Fannie and Freddie reach $200 billion... how can the ‘deniers’ say that Fannie and Freddie were enablers for a lot of the housing crisis. When it gets up to that levels, how can they say that they were only into sub-prime late, and they were only in it a little bit?” The reason that people can say that is because it is true. The $200 billion was a mere drop in the ocean of derivatives which in 2007 amounted to three times the size of the entire global economy.

When the country’s leaders start promulgating obvious nonsense as the truth, and the Big Lie starts to go viral, then we know that we are laying the groundwork for yet another, even-bigger financial crisis. The story of the 2008 financial crisisSo let’s recap the basic facts: why did we have a financial crisis in 2008? Barry Ritholtz fills us in on the history with an excellent series of articles in the Washington Post:

The driving force behind the crisis was the private sectorLooking at these events it is absurd to suggest, as Bloomberg did, that "Congress forced everybody to go and give mortgages to people who were on the cusp."

Many actors obviously played a role in this story. Some of the actors were in the public sector and some of them were in the private sector. But the public sector agencies were acting at behest of the private sector. It’s not as though Congress woke up one morning and thought to itself, “Let’s abolish the Glass-Steagall Act!” Or the SEC spontaneously happened to have the bright idea of relaxing capital requirements on the investment banks. Or the Office of the Comptroller of the Currency of its own accord abruptly had the idea of preempting state laws protecting borrowers. These agencies of government were being strenuously lobbied to do the very things that would benefit the financial sector and their managers and traders. And behind it all, was the drive for short-term profits. Why didn’t anyone say anything?As one surveys the events in this sorry tale, it is tempting to consider it like a Shakespearean tragedy, and wonder: what if things had happened differently? What would have occurred if someone in the central bank or the supervisory agencies had blown the whistle on the emerging disaster? The answer is clear: nothing. Nothing would have been different. This is not a speculation. We know it because an interesting new book describes what did happen to the people who did speak out and try to blow the whistle on what was going on. They were ignored or sidelined in the rush for the money.

The book is Masters of Nothing: How the Crash Will Happen Again Unless We Understand Human Nature by Matthew Hancock and Nadhim Zahawi (published in 2011 in the UK by Biteback Publishing and available on pre-order in the US).

In 2004, the book explains, the deputy governor of the Bank of England (the UK central bank), Sir Andrew Large, gave a powerful and eloquent warning about the coming crash at the London School of Economics. The speech was published on the bank’s website but it received no notice. There were no seminars called. No research was commissioned. No newspaper referred to the speech. Sir Andrew continued to make similar speeches and argue for another two years that the system was unsustainable. His speeches infuriated the then Chancellor, Gordon Brown, because they warned of the dangers of excessive borrowing. In January 2006, Sir Andrew gave up: he quietly retired before his term was up.

In 2005, the chief economist of the International Monetary Fund, Raghuram Rajan, made a speech at Jackson Hole Wyoming in front of the world’s most important bankers and financiers, including Alan Greenspan and Larry Summers. He argued that technical change, institutional moves and deregulation had made the financial system unstable. Incentives to make short-term profits were encouraging the taking of risks, which if they materialized would have catastrophic consequences. The speech did not go down well. Among the first to speak was Larry Summers who said the speech was “largely misguided”. In 2006, Nouriel Roubini issued a similar warning at an IMF gathering of financiers in New York. The audience reaction? Dismissive. Roubini was “non-rigorous” in his arguments. The central bankers “knew what they were doing.”

The drive for short-term profit crushed all opposition in its path, until the inevitable meltdown in 2008. Why didn’t anyone listen?On his blog, Barry Ritholtz puts the truth-deniers into three groups: 1) Those suffering from Cognitive Dissonance — the intellectual crisis that occurs when a failed belief system or philosophy is confronted with proof of its implausibility.

2) The Innumerates, the people who truly disrespect a legitimate process of looking at the data and making intelligent assessments. They are mathematical illiterates who embarrassingly revel in their own ignorance.

3) The Political Manipulators, who cynically know what they peddle is nonsense, but nonetheless push the stuff because it is effective. These folks are more committed to their ideology and bonuses than the good of the nation. He is too polite to mention:

4) The Paid Hacks, who are being paid to hold a certain view. As Upton Sinclair has noted, “It is difficult to get a man to understand something, when his salary depends upon his not understanding it.”

Barry Ritholtz concludes: “The denying of reality has been an issue, from Galileo to Columbus to modern times. Reality always triumphs eventually, but there are very real costs to it occurring later versus sooner .”

For full post, see here: https://www.forbes.com/sites/stevedenning/2011/11/22/5086/#1ff8a163f92f

By Nicholas MIdler “Stanford Analytica” trended on social media Tuesday afternoon as Facebook CEO Mark Zuckerberg testified before Congress on the Cambridge Analytica privacy breach and fielded questions about data mining startup Palantir. But what does Stanford or Palantir have to do with Facebook’s data disaster?

When Senator Maria Cantwell of Washington used the name “Stanford Analytica” for Palantir, she was making a dig at the notoriously secretive tech startup that, like Cambridge Analytica, has close ties to an elite university deeply embedded in the private sector technology and data analytics scene — all but one of the five Palantir founders completed degrees at Stanford. Co-founder Peter Thiel ’89 JD ’92 continues to maintain networks with The Stanford Review, and a healthy contingent of Stanford-educated interns and employees joins Palantir each year.

As part of Tuesday’s hearing, Cantwell asked Zuckerberg whether Palantir — whose co-founder Thiel sits on Facebook’s board of directors — had ever scraped data from Facebook. “Senator, I’m not aware of that,” Zuckerberg answered. He later said in reply to another question that he was “not that familiar with what Palantir does.” Earlier on, Cambridge Analytica whistleblower Christopher Wylie had implicated Palantir in the misuse of Facebook data. “There were Palantir staff who helped build the models that we [Cambridge Analytica] were working on,” Wylie told members of the UK parliament. “There were senior Palantir employees that were also working on the Facebook data.”

Palantir disputes Wylie’s claims. “Palantir has never had a relationship with Cambridge Analytica nor have we ever worked on any Cambridge Analytica data,” a Palantir spokesperson told TechCrunch.

The Times story exposing Cambridge Analytica’s links to Palantir characterized the latter as a “top Silicon Valley contractor to American spy agencies and the Pentagon”; other journalism about the company has emphasized Thiel’s support for President Donald Trump, whose campaign allegedly benefited from Cambridge Analytica’s data). But the nature of Palantir’s business is famously murky, whether to the media or to industry players interested in the company’s finances and valuation. A document leaked to TechCrunch in 2015 revealed that the company’s operations as of 2013 focused on making human data easily accessible for clients, who do not need to be able to code to query huge datasets.

Applications range from public sector uses such as “predictive policing” to analyzing consumer behavior to humanitarian efforts such as aid distribution to refugees. A 2016 Mercury News profile quoted “a person close to the company” stating that “at least 60 percent of the company’s work is with for-profit companies” despite its roots as a government and defense contractor — but because Palantir is not a publicly-traded firm, its clients, finances and activities remain largely unknown to the general public."

For full post, see: https://www.stanforddaily.com/2018/04/10/what-is-stanford-analytica-anyway/

For a related piece, see:

"Infographics on the distribution of wealth in America, highlighting both the inequality and the difference between our perception of inequality and the actual numbers. The reality is often not what we think it is."

By In The Public Interest

A Guide to Evaluating Pay for Success Programs and Social Impact Bonds aims to help advocates identify the critical issues surrounding PFS contracts and their impact on vulnerable individuals and the public. We describe these issues and include a list of key questions advocates can raise to help ensure that decision makers make choices that advance the public good. PFS brings venture capital to the provision of public services. Investors, such as Goldman Sachs or Bank of America, provide up-front funds for critical preventive services with the expectation of receiving a return on their investment. The theory is that the private investment dollars can fill a funding gap when government doesn’t have adequate financial resources to spend on prevention activities.

Under a PFS arrangement, the government repays the loan with interest if pre-determined social outcome targets are met. The theory presumes that even after paying the investors and service providers, the state ultimately reaps financial savings through foregone budget dollars spent to address future more costly, but now avoided, social problems. But PFS looks better on paper than in reality. A closer look at how they operate raises issues that warrant careful consideration for decision-makers looking to undertake a PFS. Some Important Questions to Ask

For full (original) post, see:

By Emily Talmage If you haven’t heard yet, data is the new gold, and next-gen ed reformers can’t wait to get their hands on as much of it as they can.

Digital and online learning providers want this gold to “personalize” their computerized instruction; Wall Street wants it to prove that their social impact bonds are “working;” testing companies want it because people are paying them big money for it; and corporations want it so they can track and influence what kinds of products the public schools churn out for them.

Unfortunately for the miners, there are a few pesky barriers preventing them from having full access to your children’s personal information, including the Family Education Rights and Privacy Act, which prevents third parties from accessing student information without written consent from parents.

To get around this law, United Way of Salt Lake City, which has recently partnered with an organization called “StriveTogether” – a subsidiary of KnowledgeWorks Foundation that has received millions from the Gates Foundation – is now encouraging parents to sign a form waiving their FERPA rights.

They’ve even put together a video to convince parents just how important it is that they give up their children’s personal information to just about any organization in the city that wants it – including the Salt Lake City Chamber of Commerce"...

For full post, please see: https://emilytalmage.com/2016/01/17/united-way-to-parents-give-us-your-gold/

The slides above are provided in Part 3 of 7 in the Series: Education in the Cloud. Introduction at: https://wrenchinthegears.com/2017/07/13/smart-cities-social-impact-bonds-public-educations-hostile-takeover-part-ii/

They can also be downloaded by clicking the title or arrow above or the following link: https://www.slideshare.net/MollySumner/what-is-a-smart-city-77832725

|