It is not easy to provide a concise definition of accounting since the word has a broad application within businesses and applications.

The American Accounting Association define accounting as follows:

"the process of identifying, measuring and communicating economic information to permit informed judgements and decisions by users of the information!.

Included in this chapter - The accounting for costs incurred subsequent to asset acquisition, Appropriate methods to measure and record the disposal of PP&E, Accounting for asset exchanges, Rules for recording asset impairments, Natural resource accounting and depletion concepts and Intangible asset accounting and amortization concepts.

Accountants use generally accepted accounting principles (GAAP) to guide them in recording and reporting financial information. GAAP comprises a broad set of principles that have been developed by the accounting profession and the Securities and Exchange Commission (SEC). Two laws, the Securities Act of 1933 and the Securities Exchange Act of 1934, give the SEC authority to establish reporting and disclosure requirements.

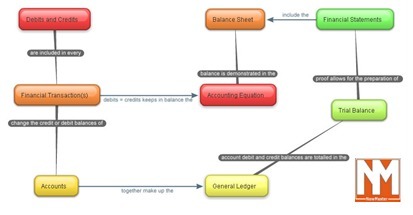

This article sets out to explain the history, purpose and application of 'Debits and Credits' in accounting. Starting with the confusion surrounding the terms and moving on through the relationships that 'Debits and Credits' have with the Accounting Equation and the source and destination of funds in the financial system, the article finishes with an infographic summary that brings all the concepts of 'Debits and Credits' visually together on one poster.

A video summary of chapter 7 in Perdisco's Financial Accounting 360Textbook. Including: Special journals & subsidiary ledgers, sales cycle: sales journal & cash receipts journal, Purchases cycle: purcases journal & cash payments journal, the general journal with special journals.

After studying this chapter you should be able to explain the revenue recognition principle, differenciate between the cash basis and accrual basis of accounting, explain why adjusting entries are needed, and identify the major types of adjusting entries, prepare adjusting entries for deferrals and accruals, define the nature and purpose of the adjusted trial balance, explain the purpose of the adjusted trial balance, explain the purpose of closing entries, describe the required steps in the accounting cycle, understand the causes of differences between net income and cash provided by operating activities.

This accounting infographic covers the key aspects of Debits and Credits in accounting including definition, the underlying principles, the rules of Debits and Credits, where it fits in the accounting process and how to determine the debit and credit for weach transaction. To download the full free infographic - click here - http://www.box.net/shared/v4j6okexia4y6lnj50t0

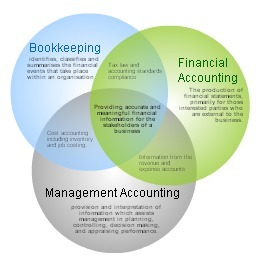

An infographic describing the relationship between the three functions of accounting: Bookkeeping, Financial accounting and Management accounting. Download the free poster by clicking on the title.

A video summary of chapter 6 in Perdisco's Financial Accounting 360Textbook and including the Inventory fundamentials, Inventory costing methods, Valuing inventory at other than cost.

Under GAAP rules, asset acquisitions are initially recorded at their original cost. Although an allowance for depreciation is reflected against most assets, no attempt is made to adjust these historical costs to current market values. This is called the historical cost principle.

The matching principle dictates that the cost of fixed assets such as machinery, furniture, and real estate ought to be spread over the number of periods that they will help generate revenue.

Financial accounting prepares a limited number of prescribed financial reports in accordance with statutory standards and the needs of external stakeholders. Financial accounting summarizes the consequences of past decisions on the performance of the business as a whole. Management accounting prepares an unlimited number of financial reports in accordance with business requirements and the needs of management. Management accounting analyses the performance of units within the business by comparing results with preset budgets and so assists management in their future planning and control functions.

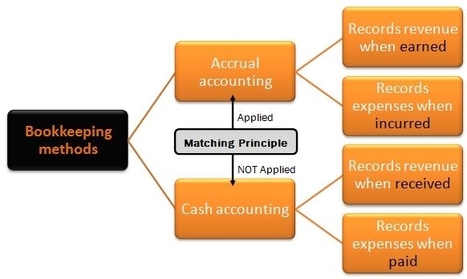

Both the cash and accrual accounting methods of bookkeeping are accepted by tax law and accounting standards as appropriate ways to record and report on the financial events of a business. The advantages and disadvantages of each method are only appropriate to small enterprises who are given this choice. Large corporations and for-profit companies are required to report on their financial position and performance using only the accrual accounting method.

Account balances sitting in general ledger “T” accounts do not provide a very useful format for accessing accounting information. Periodically, accountants need to compile the information in the general ledger into the basic financial statements: the balance sheet and income statement. How often should this happen? From a manager’s point of view, basic financial statements should be prepared in a timely fashion so any unexpected trends in revenues and expenses can be detected and addressed. Most businesses find monthly statements adequate, although firms operating under very stable economic conditions find quarterly or annual financial statements sufficient.

Bad debts occurs when customer debts due to the business for goods provided or services rendered, become uncollectable. Bad debts are usually a product of customer bankruptcy, company liquidation or where the extra cost of pursuing the debt is greater than the amount of money that the business could posibably collect. When it is determined that a debt is bad, the customer debt is written off in the books of the business. This transaction reduces the value of the accounts receivable in the balance sheet as it increases the expenses of the business in the Income Statement.

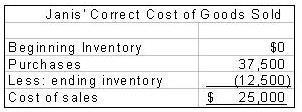

Goods sold to customers are assets called inventory. Inventory measurements can be surprisingly difficult. Different inventory measurement approaches can lead to wide variations in reported profits or losses.

Including: Measurement of costs assigned to property, plant, and equipment, Principles relating to service life and depreciation, Depreciation concepts and terminology, The straight-line, units-of-output, and double-declining balance depreciation methods, Unique features of depreciation under tax codes, Equipment leases and the accounting implications.

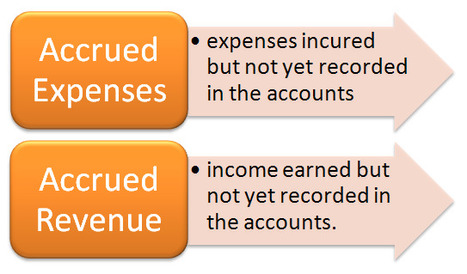

Accruals in accounting are special journal entries that are made by accountants and bookkeepers at the end of each accounting period and prior to the preparation and distribution of the financial statements. Accruals are the practical application of the matching period where income and expenses must be recorded in the accounting period where they are respectively earned and incurred. Accrual entries involve bringing to account revenue that has been earned but not yet invoiced and expenses that has been incurred but not yet billed.

IFRS, International Financial Reporting Standards, is similar to GAAP but is accepted around the globe between international companies. Originating from London, IFRS is required in over 100 countries and not in the U.S. Since there are an overwhelming amount of similarities between GAAP and IFRS, there has been discussion of bringing the two together and creating one mass set of standards for everyone to follow.

Answer (1 of 3): Like many things in accounting, the term amortization has different meanings in different contexts and the term is often used interchangeably with other similar concepts like depreciation.

This principles of accounting including how intent influences the accounting for investments, the accounting for "available-for-sale" securities, accounting for securities that are to be "held-to-maturity.", special accounting for certain investments that require use of the "equity method." and investments that result in consolidated financial statements.

A video summary of chapter 5 in Perdisco's Financial Accounting 360Textbook including merchandising operations, recording purchases of merchandise, recording sales of merchandise and completing the accounting cycle of a merchandiser.

To get content containing either thought or leadership enter:

To get content containing both thought and leadership enter:

To get content containing the expression thought leadership enter:

You can enter several keywords and you can refine them whenever you want. Our suggestion engine uses more signals but entering a few keywords here will rapidly give you great content to curate.

Your new post is loading...

Your new post is loading...