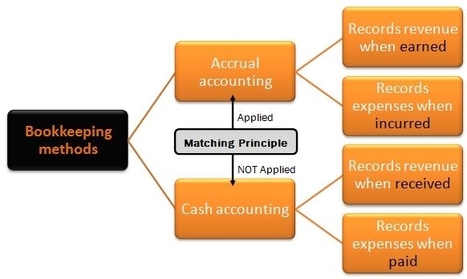

Both the cash and accrual accounting methods of bookkeeping are accepted by tax law and accounting standards as appropriate ways to record and report on the financial events of a business. The advantages and disadvantages of each method are only appropriate to small enterprises who are given this choice. Large corporations and for-profit companies are required to report on their financial position and performance using only the accrual accounting method.

Your new post is loading...

Your new post is loading...