This principles of accounting website provides a free comprehensive textbook and support resources. Both financial accounting and managerial accounting topics are covered including Inventory costing methods, The perpetual system for valuing inventory, Lower-of-cost-or-market inventory valuation adjustments ,Two inventory estimation techniques: the gross profit and retail methods ,Inventory management and monitoring, and the impact of errors.

A video summary of chapter 4 in Perdisco's Financial Accounting 360Textbook including classified balance sheet, closing entries and a summary of the accounting cycle.

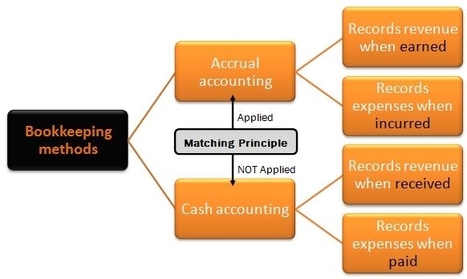

Accrual accounting is a method of bookkeeping that records revenues and expenses as they are earned or incurred, rather than when the cash is actually exchanged. By contrast, the cash accounting method delays the recording of revenues and expenses until the cash is actually exchanged (received or paid)

Cash accounting is a method of bookkeeping that delays recording the revenues and expenses of a business until the cash is actually exchanged (i.e. when cash is actually received or paid out). By contrast, the accrual accounting method records revenues at the point they are earned and records expenses when a legal obligation to pay is created.

This equation is also the basis for the most basic of accounting reports, the aptly named Balance Sheet. A balance sheet reports what a business owns (assets), what it owes (liabilities) and what remains for the owners (equity) as of a certain date. This equation must always be in balance. Always keep in mind the teeter totter illustration shown above.

A bad debt is the ultimate recognition of loss created when a specific debtor(s) is acknowledged as being unable to pay the debt they owe to the business. This loss, recorded in the Income Statement of a business assesses that at this point in time, the money owed to the business will never be received. Doubtful debts on the other hand are an interim recognition of possible losses caused by irrecoverable (bad) debt that may take place sometime in the future. While bad debts will be linked to specific debtors and written off in the period where the revenue was earned, doubtful debts are an estimate and provision for future losses that is usually based on previous history.

Your goals for this “merchandising” chapter are to learn about:Merchandising businesses and related sales recognition issues.Purchase recognition issues for the merchandising business.An alternative inventory system: The perpetual method.Enhancements of the income statement. The control structure.

The revenue recognition principle is a set of guidelines that helps accountants to identify when a revenue event has taken place and how to appropriately record cash exchanges before, during and after the revenue event. The revenue recognition principle also helps determine the accounting period in which the revenue is to be recorded.

A video summary of chapter 1 in Perdisco's Financial Accounting including - The role of accounting information, business structures, the accounting equation, transaction analysis and the introduction to financial statements.

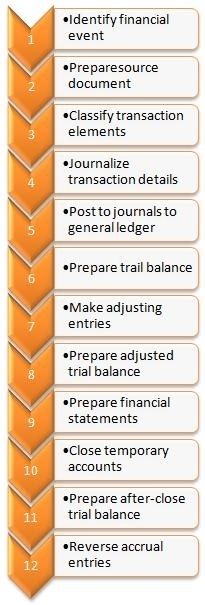

The previous chapter presented adjustments that might be needed at the end of each accounting period. These adjustments were necessary to bring a company's books and records current in anticipation of calculating and reporting income and financial position. This chapter begins by illustrating how such adjustments would be used to actually prepare financial statements.

This principles of accounting website provides a free comprehensive textbook and support resources. Both financial accounting and managerial accounting topics are covered.

This principles of accounting website provides a free comprehensive textbook and support resources. Both financial accounting and managerial accounting topics are covered.

This principles of accounting website provides a free comprehensive textbook and support resources including: The nature of financial and managerial accounting information, The accounting profession and accounting careers, The accounting equation: Assets = Liabilities + Owners’ Equity, How transactions impact the accounting equation and The four core financial statements..

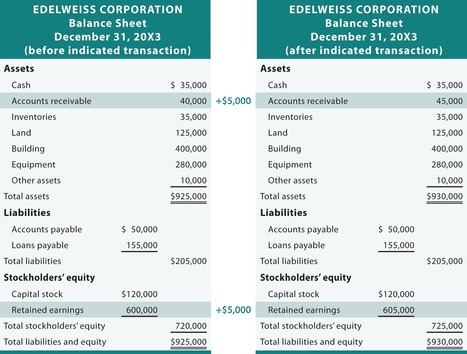

In accrual accounting, revenue is recorded when earned, and expenses recorded when incurred. A customer’s obligation to pay for goods and services provided is called accounts receivable. From the firm’s point of view, accounts receivable are assets. When a firm receives goods or services from another business before payment, the firm incurs a liability called accounts payable.

The text book chapter on the Principles of Accounting including; The costs and benefits of selling on credit; Accounting considerations for uncollectible receivables; Alternative approaches to account for uncollectibles; Notes receivable and interest, including dishonored obligations.

A video summary of chapter 3 in Perdisco's Financial Accounting 360Textbook dealing with timing and reporting of adjusting entries like prepaid expenses, unearned revenue, accrued expenses and accrued revenues.

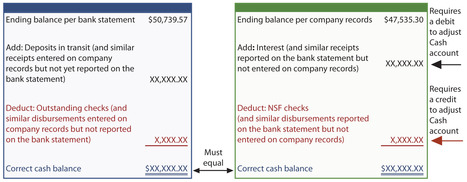

Your goals for this “cash” chapter are to learn about: The composition of cash and how cash is presented on the balance sheet, Cash management and controls for receipts and disbursements, Reconciliation of bank accounts, The correct operation of a petty cash system, Accounting for highly-liquid investments known as “trading securities.”

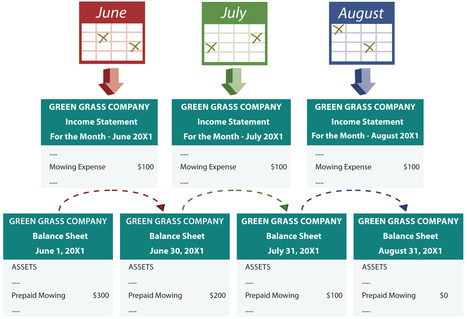

The matching principle is a fundamental accounting concept in the measurement of net income. The matching principle directs those preparing financial statements to ensure that revenues and all their associated expenses are recorded in the same accounting period. This is done to ensure that a net income is not distorted by time differences in billing and cash exchanges. The matching principle is the basis on which the accrual accounting method of bookkeeping is built.

A video summary of chapter 2 in Perdisco's Financial Accounting 360Textbook. It includes: Introduction to the accounting cycle, debits and credits, general journal and general ledger, illustration of transaction analysis, trial balance.

As balance sheets, income and loss statements, and also assets and liabilities are commonly used in the business world, it is nearly essential that you learn as much as possible about the ways of the double entry bookkeeping system.

A Trial Balance in accounting is prepared to verify that the double-entry bookkeeping rules have been adhered to in recording the financial transaction during a particular period. This is done by totaling all the [Dr.-Debit] balances in the general ledger and ensuring that they agree with the totals of all the [Cr.-Credit] balances in the general ledger.

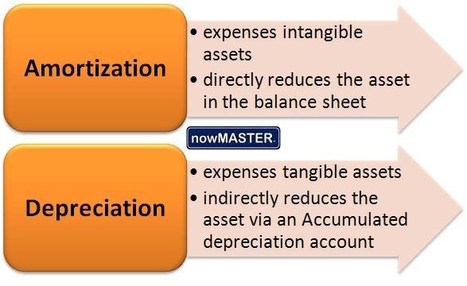

Amortization in accounting is the process of expensing (writing off) the value of the intangible (non-physical) assets of a business. Amortization for intangible assets is the same concept in accounting as depreciation is for fixed (physical) assets. Amortization of intangible assets takes place periodically over the period covering the estimate useful economic life of the intangible assets. Intangible assets typically include intellectual property costs and incorporation costs.

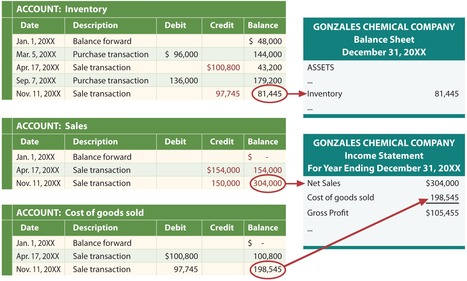

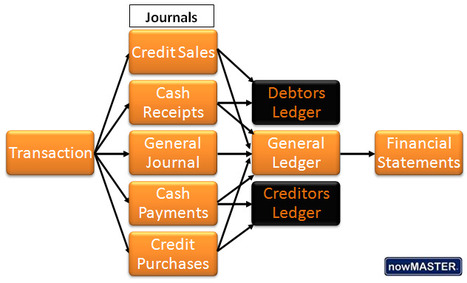

Subsidiary ledgers in accounting involve the grouping of individual accounts that share a common element. Individual accounts that share a common element include suppliers, customers, inventory items and fixed assets. These individual accounts collectively add up to the value of the corresponding control account reported as a total in the general ledger. For example the accounts payable is the control account for the subsidiary ledger of suppliers and known as the creditors ledger. The accounts receivable is the control account for the subsidiary ledger of customers and known as the debtors ledger.

The general ledger is the central core of the accounting information system where all of the financial transactions of a business are categorized and summarized into accounts. These accounts in the general ledger group similar transactions into individual records producing a continually updated credit/debit balance for each. The number and type of accounts that make up the general ledger is determined by the chart of accounts. The general ledger contains a permanent history of all the financial transactions that have taken place in the business since its first day of operation.

To get content containing either thought or leadership enter:

To get content containing both thought and leadership enter:

To get content containing the expression thought leadership enter:

You can enter several keywords and you can refine them whenever you want. Our suggestion engine uses more signals but entering a few keywords here will rapidly give you great content to curate.

Your new post is loading...

Your new post is loading...