Your new post is loading...

Your new post is loading...

|

Scooped by

Prentiss & Carlisle

October 16, 2018 9:22 AM

|

Warmer temperatures brought on by climate change will lead to drier soils and reduce tree photosynthesis and growth in forests later this century, according to a new University of Minnesota study published in the journal Nature. That important conclusion comes as scientists have speculated the opposite: that a warming climate might speed up a forests' photosynthesis and facilitate growth in cold-weather climates found in North America, Europe and Asia. "These results have important implications for the future," said Peter Reich, a professor of forest resources in the College of Food, Agricultural and Natural Resource Sciences and the study's lead author. "Typical dry spells already occur frequently enough to erase most of the potential benefits to tree growth of warmer summer temperatures. In a warmer future, the extra evaporation from warmer plants and soils will make those dry spells drier, further suppressing photosynthesis." Cool summers slow the growth of forests in cold places. That's why scientists had hypothesized that warmer climatological conditions might help increase a forest's growth rate in the future. In their study, University of Minnesota researchers looked at more than 2,000 young trees from 11 different species—including birch, maple, oak, pine and spruce—growing in 48 plots in two forests in northern Minnesota. During the three-year study, researchers increased temperatures at the test plots—without use of chambers of any kind—by 3.4 degrees Celsius (6 degrees Fahrenheit), an increase that might happen in Minnesota by the end of the 21st century. During the course of the study, researchers routinely measured photosynthesis at the plots to see how fast leaves were taking carbon dioxide out of the air to make sugars for the trees. Researchers found that:when soils were moist, photosynthesis was higher in plants growing at warmer than at ambient temperatures;in moderately to severely dry soils, which occurred during two-thirds of the growing season, warmer temperatures reduced photosynthesis;as a result, photosynthesis was reduced—on average—by the experimental climate warming. "These results show that low soil moisture will slow down or eliminate any potential benefits of climate warming on tree photosynthesis even in moist, cold climates like Minnesota, Canada and Siberia," said Reich.

|

|

Scooped by

Prentiss & Carlisle

October 16, 2018 9:10 AM

|

A number of important lumber-related developments have come out of North America over the last week: The US-Mexico-Canada Agreement (USMCA)

The USMCA was recently inked, which does not mention softwood lumber specifically but does renew the very important Chapter 19 dispute resolution mechanism. With the negotiations of the USMCA now complete, this leaves open the possibility that the US and Canada may now focus on resolving the contentious trade disputes regarding softwood lumber. ***

United Steelworkers Strike Notice The union representing roughly 2,000 sawmill workers in Northern BC, including Quesnel and Williams Lake, recently issued a 72-hour strike notice.

The most recent development as of this writing is that BC sawmill workers have now been banned from working overtime hours, which can make it difficult for producers to quickly adjust to market conditions or the arrival of fresh logs to the mill.

Erratic US Housing Market

US homebuilding was up in August but existing home sales slowed as prices have soared out of reach for many buyers. The US housing market—already struggling with tight inventory and rising building costs—faces a fresh headwind as 30-year mortgage rates rise close to the 5 percent threshold for the first time in years. The rise in mortgage rates so far this year means a potential homebuyer would pay about US$35,000 more interest on a US$220,000 loan over 30 years. Home prices are also soaring in conjunction with mortgage rates.

***

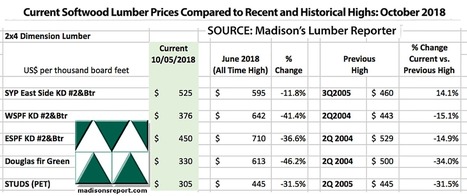

All of these factors appear to be combining to produce a level of uncertainty in the market. Prices for 2x4 dimensional lumber have dropped precipitously since hitting an all-time high in June; Douglas fir green 2x4s are down nearly 50%. The table below provides a comparison of the all-time high prices (June 2018) and current prices (mid-October 2018) for benchmark dimension softwood lumber 2x4s vs. their previous historical highs of 2004/05:

|

|

Scooped by

Prentiss & Carlisle

October 11, 2018 6:16 PM

|

ND Paper LLC has increased its presence in Maine, reaching an agreement to purchase the Old Town pulp mill that closed three years ago, saying that it will create more than 100 jobs in the Penobscot County community. The U.S. subsidiary of Hong Kong-based Nine Dragons Paper Holdings Ltd. recently purchased the Catalyst paper mill in Rumford and hopes its latest deal will be completed in 30 days. The sale is a cash deal for an undisclosed sum. “We are absolutely thrilled to restart the Old Town Mill and return well over 100 high paying jobs to Penobscot County,” Ken Liu, CEO of ND Paper, said in a statement Wednesday. “By leveraging our existing manufacturing platform in Maine, combined with the financial capacity to wisely invest in the mill’s production capabilities, we expect to create a very strong future for this facility.” ND Paper plans to make capital investments in Old Town and restart the mill in the first quarter of 2019 with the capability of annually producing 275,000 air dried metric tons of unbleached kraft pulp. ND Paper purchased what is now called the Rumford Mill in June and this week announced it will invest $300 million in that mill and another it owns in Biron, Wisconsin, over the next two years. ND Paper said the $111 million investment in the Rumford Mill will support 650 jobs and create another 50. ND Paper is headquartered in Oak Brook Terrace, Illinois. Nine Dragons Paper is Asia’s largest producer of containerboard, which is most commonly used in making cardboard boxes. *** The agreement calls for ND Paper to acquire the bleached kraft pulp mill, as well as 100 acres of property in Old Town. Prior to the mill being idled in the fourth quarter of 2015, the mill manufactured and distributed 155,000 air dried metric tons of bleached hardwood kraft pulp annually.

|

|

Scooped by

Prentiss & Carlisle

October 5, 2018 4:41 PM

|

Corn, coffee, cattle, and other crops can be raised on land that also supports cultivated timber. This symbiotic approach, known as agroforestry, has clear ecological benefits – and it could become a new asset class for timberland investors. The opportunities and obstacles to expanded agroforestry are explored by the Global Agroforestry Review, a new report from RISI, the leading information provider for the global forest products industry. "Public concern about environmental impact is mounting on agribusinesses, and on the pension funds and others who invest in them," said John North, RISI International Timber Economist and co-author of the report, along with RISI Director of International Timber Bob Flynn. "Timberland investment management organizations (TIMOs) and other investors should recognize the risks of current 'monoculture' approaches, and the potential for agroforestry to mitigate those risks." *** Agroforestry is an accepted practice throughout much of the world. Important cash crops, such as corn and rice, are planted in rows among eucalyptus trees in Brazil, India, and other major agricultural exporters. Coffee and cacao are harvested from timber-producing forests in Latin America and Asia, and cattle graze among cultivated pines in Argentina – a practice called "silvopasturing." Researchers and landowners in the US and Brazil, among others, are exploring how agroforestry methods can be scaled up worldwide. Promising agroforestry projects include a recent investment by PSP, one of the largest pension funds in the timberland space, in a Brazilian coffee producer that integrates timber and coffee operations. *** Benefits of agroforestry can include: - Diversification of revenue: Cash crops harvested annually can support farmers, landowners, and investors while trees mature.

- Environmental sustainability: Trees can prevent erosion and provide shade, while benefiting from the water/fertilizer applied to other crops.

- Social responsibility: Institutional investors face growing scrutiny of their practices, especially in the developing world. Agroforestry programs can demonstrate active support for the well-being of vulnerable farmers and ecosystems.

Agroforestry has yet to attract significant investment from TIMOs, but North and Flynn believe that the conditions are right for growth. "In our research for the Global Agroforestry Review, we found that the investment community believes that agroforestry is fine for farmers but very difficult to do on a large scale. It seems to complicate forestry operations, and there's uncertainty around valuation of land that's managed for multiple crops and end-users," said North. "Based on our review of agroforestry worldwide, we believe that this concern about scale somewhat misses the point," North said. "It doesn't have to be all or nothing. Agroforestry could comprise only a small portion of a timberland fund while adding considerable value, both through mitigating risks on-site and by improving relationships with farmers, communities, investors, and other stakeholders throughout the supply chain."

|

|

Scooped by

Prentiss & Carlisle

October 2, 2018 12:24 PM

|

Spain’s Ministry of Agriculture, Fisheries and Food (MAPAMA) has created an operating group focused on improving the traceability and efficiency of the wood supply using blockchain technology. Called ChainWood, the operating group is comprised of eight partners from different Spanish regions, including Galicia, the Community of Madrid, Andalusia, Castilla y León, and Asturias. The group was funded by MAPAMA, the Directorate General for Development Rural and Forest Policy, and the General State Administration. ChainWood aims to solve the limitations presented by the different wood supply chains in Spain, which makes it difficult to modernize and improve efficiency and access to information. ChainWood has already held working meetings in Santiago de Compostela and Madrid to develop a cloud-based software that will apply blockchain, big data, and machine learning to improve the transparency and flow of information throughout the supply chain. Once the software is developed, ChainWood will conduct pilot experiments in Castilla y León (poplar), Asturias (chestnut) and Galicia (oak). The ultimate goal is to apply the solution to all the products from the wood industry (solid wood, disintegration, cellulose pulp and biomass) and reduce costs for all actors. “The advantages of the solution are many for each of the actors,” the release said. “For example, producers will have more transparent access to the market to receive the best offers, guarantees on the volume of product and information in real time on the status of the product, the operating companies will be able to access the market more efficiently, obtain the best logistic services, obtain the best price for their products or services.”

|

|

Scooped by

Prentiss & Carlisle

October 2, 2018 11:54 AM

|

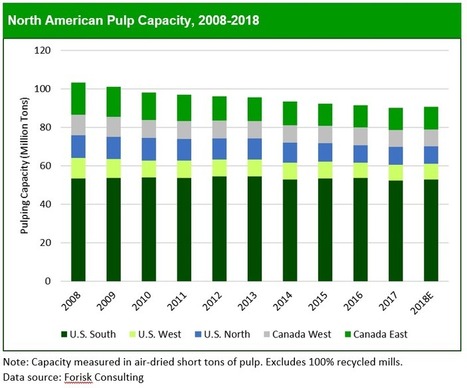

In reading about the pulp and paper industry, so much news focuses on the declines in printing and writing paper and newsprint. True, North American paper and paperboard production declined 25% since the start of the 2000’s, but the industry still has the capacity to use over 300 million tons of wood annually. Pulp and paper remains a massive and important industry. Different paper sectors have experienced divergent fortunes, with packaging and household paper far more resilient than newsprint and printing and writing papers. Much of the activity in the paper sector is in conversions to packaging, tissue or fluff pulp to service those thriving markets.

The end-use sector served by mills regionally provides important context to understand pulping capacity. The South has clear advantages over other regions, with the majority of both household/sanitary and packaging capacity. This has served as a bulwark against the paper industry’s overall decline over the past decade (Figure). Total pulping capacity in 2018 is 91 million tons, 12% less than the sector’s 103 million tons of capacity in 2008. Capacity declined in every region, but end-use exposure affected the scale of those shifts. The South has been and remains the largest pulping region, growing from 52% to 58% of North American capacity. Every other region shrank in proportional relevance, led by Eastern Canada, which represented 16% of total capacity in 2008, compared to 13% in 2018. Western Canada’s proportion dropped the least (0.5%) and remains around 10%.

The drop in pulping capacity is a function of mill closures. Between 2008 and 2018, the number of pulp mills decreased by 18%, while average pulp mill capacity increased 7%. Average capacity declined only in East Canada (0.6%), which also saw the greatest drop in operable pulp mills (30%). Average capacity increased in the other regions through investments and closure of smaller facilities. No new pulp mills have been built, though a small number of mills that were not operating in 2008 have reopened.

|

|

Scooped by

Prentiss & Carlisle

September 18, 2018 11:14 AM

|

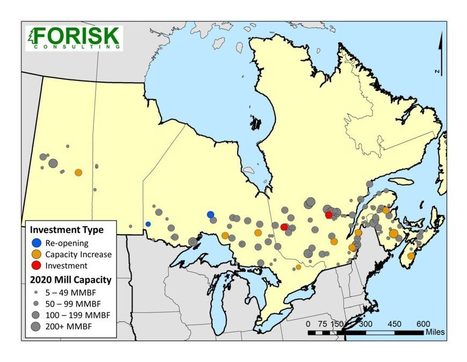

Over the past decade, Eastern Canada has consistently been the fourth-largest installed base of regional softwood lumber manufacturing capacity in North America, behind the U.S. South, the U.S. West, and Western Canada. However, the region has gained importance as a source of incremental production and capital investment, offsetting lost production in the wake of the mountain pine beetle infestation and devastating fires suffered in Western Canada. Eastern Canada currently accounts for 12.0 billion board feet (BBFT) of softwood lumber capacity (17% of North America’s total capacity), a modest reduction from a decade ago. However, production is on track to reach 11.8 BBFT this year – the seventh consecutive year of production gains (Figure 1). With a utilization rate of 98%, Eastern Canada lumber producers are making the most of their assets.

The narrowing rift between capacity and production is driving investment. Figure 2 maps announced, active and completed capital investment projects in Eastern Canada over a five-year period, beginning in 2016 and including projects with expected completion by 2020. Overall, these projects are modest in size, totaling less than 700 MMBF in softwood lumber capacity. Still, these investments, along with the highest utilization rates in North America since 2016, highlight the important role played by the region in North American production. The most remarkable take-home from the map is the broad and diversified effort to upgrade, improve or expand capacity at existing mills to, in part, offset lost production in Western Canada and serve the U.S. export market.

|

|

Scooped by

Prentiss & Carlisle

September 18, 2018 10:14 AM

|

Investment manager New Forests has announced its latest acquisition under the firm’s growing US timberland investment program, with the purchase of 10,400 acres of Humboldt County timberlands from Soper Company. The estate is known as the Pine Creek Timberlands and completes the placement of an investment fund focused on high carbon value forests in California.

“New Forests is pleased to acquire these high-quality Northern California timberlands,” said Jon Loevner, Manager of US Investments for New Forests. “The Pine Creek Timberlands are an excellent fit with New Forests’ investment strategy in the US, whereby we manage forests to optimize revenues from a combination of timber harvest and carbon offset sales. This strategy enables us to lengthen harvest rotations to create higher value, larger logs while at the same time delivering a measurable, verifiable climate benefit through California Carbon Offsets.”

New Forests is one of the world’s largest forestry investment managers and has solidified a leading position as a developer of forest offset projects for California’s cap-and-trade market. Earlier this year, New Forests was awarded the 2017 Project Developer of the Year award by the Climate Action Reserve. New Forests currently has 23 US carbon projects in development and operation.

“The world’s forests are a critical resource for climate change mitigation, with forests and land use offering up to 30% of mitigation potential through 2030,” said Brian Shillinglaw, Executive Director of New Forests Inc. “New Forests’ US timberland investment program responds to this challenge by applying New Forests’ deep forestry and carbon asset investment expertise to the US timberland market, delivering market-rate climate impact investment solutions to institutional investors.”

Shillinglaw continued, “New Forests’ in-house geospatial analytics and carbon valuation skills, combined with a track record of responsible forestry investment, drive investment value while at the same time securing carbon storage and capturing the climate benefit of ongoing carbon sequestration in sustainably managed forests. This differentiated approach to investing in the US timberland market presents a unique opportunity for institutional capital to make a meaningful contribution to climate mitigation while also meeting investors’ portfolio needs for higher risk-adjusted returns in real assets.”

The Pine Creek Timberlands include Douglas fir, mixed hardwoods, and redwood stands. The property has historically been managed for high value Douglas fir timber. The estate complements the recent acquisition of a predominantly redwood and Douglas fir forest with parcels located near Eureka on behalf of the same fund. New Forests also announced the acquisition of approximately 170,000 acres of mixed conifer forests in Northern California in early 2018, now operating as Shasta Cascade Timberlands LLC. The settlement on Pine Creek Timberlands brings New Forests’ US timberland assets under management to 186,000 acres.

The company also manages more than 500,000 acres of forest carbon offset projects throughout the continental United States and Alaska. Globally, New Forests manages around 2.3 million acres (915,000 hectares) of forests and conservation investments with assets under management of approximately USD 3.7 billion.

|

|

Scooped by

Prentiss & Carlisle

September 13, 2018 12:09 PM

|

*** In fiscal 2018, the Teacher Retirement System's stock market investments gained a return of 13.4 percent to reach $9.49 billion in value, while bond investments posted a return of 1.3 percent to end up at $2.57 billion, according to Aon Hewitt.

The system's private equity investments earned a return of 22.3 percent to reach $2.03 billion, while real estate investments gained 10.8 percent to end up at $1.41 billion, the consultant said.

Agricultural investments posted a 3.3 percent return to reach $195 million. Timber investments recorded a 1.2 percent return to end up at $267 million last fiscal year, according to Aon Hewitt.

The system's opportunistic alternative investments gained a return of 0.7 percent to end up at $984 million. Infrastructure investments totaled $182 million and cash totaled $179 million at the end of the fiscal year.

|

|

Scooped by

Prentiss & Carlisle

September 10, 2018 1:30 PM

|

Investors tired of poor returns, are getting out of timberland — at what some say is the wrong time. Leading the exit are CalPERS and Harvard. The California Public Employees' Retirement System, Sacramento, in the third quarter sold most of its $2 billion timberland portfolio, with few plans of investing again; instead, the $358.9 billion system will focus on core real estate. CalPERS' consultant said the fund sold the investments at a loss.

***

CalPERS' forestland portfolio underperformed its benchmark for the one, three, five and 10 years ended June 30. The portfolio earned 1.9% compared to the 3.8% benchmark return for the year; an annualized -2.4% (3.4% benchmark) for the three years; -1% (6.1%) for the five years; and -1.1% (4.1%) for the 10 years ended June 30. These returns do not include additional markdowns from the sale of the Crown Pine Timber portfolio, Mr. Junkin said. Meanwhile, Cambridge, Mass.-based Harvard Management Co., which manages Harvard University's $37.1 billion endowment, is also selling off portions of its timberland portfolio, sources said. Harvard Management Co. reported in September that natural resources, including timber, experienced a challenging year in its 2017 fiscal year and the endowment took write-downs and sold assets, some at or above their previous valuations. "Our natural resources platform will take multiple years to reposition," the report noted without providing details. Harvard is reportedly attempting to sell majority or minority stakes in a $700 million portfolio of timberland in South America. Fundraising by timber investment managers is way down. Two funds raised a combined $600 million so far in 2018, down from seven funds that raised $1.4 billion in all of 2017 and eight funds that raised $3.1 billion in 2008, according to data from London-based alternative investment research firm Preqin. More than 30 timberland funds manage about $57 billion of assets for investors "who cite the long-term investment horizon, low correlation with the general economy, biological growth regardless of economic conditions, and a relatively stable stream of cash flows as appealing characteristics of the asset class," according to a recent report by MetLife Inc.'s agricultural finance group, which oversees agricultural and timberland assets. Matthew Lynch, Hartford, Conn.-based managing director and head of real estate and private markets at UBS Asset Management, said poor returns are driving investors out of the asset class into other real asset sectors. Timberland assets earned 0.48% for the quarter ended June 30, down from 0.92% in the prior quarter and 0.7% in the second quarter ended June 30, 2017, the NCREIF Timberland index showed. The Total Timberland index had a 3.57% trailing return for the year ended June 30. Timberland market value per acre was $1,804 as of June 30, down from $1,824 a year earlier, according to NCREIF.

***

Between January 2017 to June 2018, average prices for commonly traded lumber in the U.S. increased by 40%, according to the Wood Resource Quarterly. During the same period, sawlog prices were practically unchanged in the South and rose about 28% in the Western U.S.

***

Some industry insiders say institutional investors are downsizing their timber exposure at the wrong time, when prices for timberland are way down. They also say the investors got into their current portfolios at the wrong time. *** Some timber managers and investors are buying timberland, seeing opportunities as some holdings are priced at a discount. In July, BTG Pactual Timberland Investment Group invested alongside British Columbia Investment Management Corp., Highland Capital Management, and Medley Management Inc. bought 1.1 million acres of prime East Texas timberland from CalPERS for $1.39 billion. The market value of CalPERS' investment in Crown Pine Timber — known as Lincoln Timber, a hedge fund of one managed by timber management organization Campbell Global — was $1.6 billion as of June 30. In October 2007, CalPERS had committed $2.2 billion to invest in 1.5 million acres in eastern Texas and western Louisiana, documents on CalPERS' website show.

|

|

Scooped by

Prentiss & Carlisle

September 10, 2018 1:12 PM

|

The battle for Phaunos Timber Fund (PTF) has intensified with CatchMark Timber Trust (CTT.N), a US real estate investment trust, announcing it is considering a $0.57 per share equity offer.

The potential bid beats a rival offer of $0.49 per share in cash from Phaunos’ former manager Stafford Capital Partners and would see shareholders receive around $284 million in CatchMark shares.

Phaunos, which holds its annual general meeting in Guernsey this afternoon, has responded by saying it will ‘engage with CatchMark to understand fully its proposal’ which represents a 16.3% premium to Stafford’s offer.

Jerry Barag, CatchMark president and chief financial offer said: ‘The Phaunos portfolio fits our existing strategy for acquiring institutional quality assets with superior productivity that can generate durable growth for our stock holders. It presents a compelling opportunity worth our study and analysis.’

***

Liberum analyst Conor Finn said CatchMark’s indicative offer looked attractive but questioned whether CatchMark shares would be a good fit for Phaunos investors.

‘We believe most of the Phaunos share register would not be long-term holders of CatchMark. This is likely to create downward pressure on CatchMark’s share price,’ he said.

***

Phaunos' board has rejected Stafford's bid as undervaluing the company, saying it will deliver more value for shareholders with an orderly wind-up and sale of its investments. Stafford has denied this saying the board's asset realisation programme will be slower and far more uncertain than its offer.

The bid tussle has embroiled Phaunos in a legal row with Rayonier, the majority investor in New Zealand's Matariki Forestry Group which represents three quarters of the company's assets. Rayonier says Phaunos breached a confidentiality agreement by publishing a valuation of Matariki in its formal response to Stafford's offer. It claims it now has the right to buy the rest of Matariki at a 20% discount, which if true would diminish the break-up value the board is seeking.

|

|

Scooped by

Prentiss & Carlisle

September 4, 2018 12:05 PM

|

A large-scale land purchase by an American forestry company west of Taupō will see 1148ha of farmland converted into a redwood forest. The $7 million purchase north of Taumarunui, near Matiere, by The New Zealand Redwood Company was approved by the Overseas Investment Office in July. The venture was likely to create six full-time jobs and increase New Zealand's export returns because the bulk of the timber will be exported to the United States in a processed form, the OIO consent said. Taupō-based NZRC was formed in 2001 by the Soper Wheeler Co of California, a 100-year-old forestry firm.

|

|

Scooped by

Prentiss & Carlisle

September 4, 2018 11:30 AM

|

As housing starts continued to slow in July, southern yellow pine (SYP) lumber prices followed suit before momentarily reversing course to stop a steady four-week slide. Forest2Market’s composite southern yellow pine lumber price for the week ending August 17 (Week 34) was $446/MBF, a 5 percent increase from the previous week’s price of $423/MBF. Year-over-year, week 34’s price represents an 18 percent increase from the same week in 2017.

The price reversal was likely driven by new SYP orders, which surged in week 34 to their highest level of 2018. While shipments didn’t reach into record territory, they were quite strong and at levels not seen since late May when SYP prices reached a peak of $576/MBF. Price volatility has been the norm thus far in 2018; the trend is likely to continue as the timing of the recent price increase and flood of new orders may foretell strong housing starts numbers for August, which will be released by the US Census Bureau on September 19.

A closer look at some of the prices we have seen since the beginning of the year:

1Q2018 Average Price: $449/MBF

2Q2018 Average Price: $523/MBF

YTD Average Price: $482/MBF

|

|

|

Scooped by

Prentiss & Carlisle

October 16, 2018 9:12 AM

|

U.S. Secretary of Agriculture Sonny Perdue today announced that Vicki Christiansen will serve as the 19th Chief of the U.S. Department of Agriculture’s (USDA) Forest Service. Christiansen has been serving as Interim Chief since March of this year. Following the announcement, Secretary Perdue issued the following statement:

“As a former wildland firefighter and fire manager, Chief Christiansen knows what’s needed to restore our forests and put them back to work for the taxpayers. With seven years at the Forest Service and 30 years with the states of Arizona and Washington, Vicki’s professional experience makes me confident that she will thrive in this role and hit the ground running.”

Tomorrow, Secretary Perdue will swear-in Christiansen as Chief in the Sidney Yates Building in Washington, D.C. Immediately following the ceremony, Secretary Perdue will hold a media availability.

|

|

Scooped by

Prentiss & Carlisle

October 16, 2018 8:53 AM

|

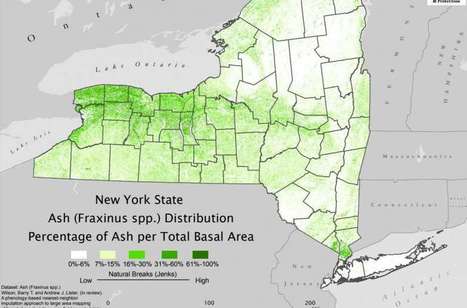

A tree that could ultimately vanish from New York under the relentless assault from a voracious invasive beetle is now worth more than ever as timber.

The value of ash trees has been on a steady climb in recent years as the state tried to quarantine areas infested by the emerald ash borer, an invasive beetle that came into the state from an infestation that started near Detroit in 2002.

***

This summer, with the borers infesting 43 of the state's 62 counties, DEC dropped that logging quarantine as no longer effective. Applauding the move, the logging industry said it might be time to cut remaining ash trees as timber before the borers get them.

This summer, the price for ash timber in parts of New York hit a peak of $600 per 1,000 board feet, about triple what it was shortly after the beetles first arrived in the state, according to bi-annual stumpage reports issued by the state Department of Environmental Conservation.

*** The average price for ash had climbed to about $300 per 1,000 board feet when the state began its quarantine in 2015, according to DEC stumpage reports at that time. *** The eventual loss of ash will forever change an industry that uses ash to produce bats for major league baseball. Ash wood has long been a staple of the Rawlings baseball bat factory in Dolgeville, Herkimer County, where bats have been made for more than six decades. As recently as 2012, ash accounted for about 90 percent of the bats made there.

|

|

Scooped by

Prentiss & Carlisle

October 10, 2018 11:55 AM

|

***

A glut of timber has piled up in the Southeast. There are far more ready-to-cut trees than the region’s mills can saw or pulp. The surfeit has crushed timber prices in Mississippi, Alabama and several other states. The volume of Southern yellow pine, used in housing and to make paper, has surged in recent decades as farmers replaced cropland with trees and as clear-cut forests were replanted. By 2020, the amount of wood growing per acre of timberland in many counties will have more than quadrupled since 1980, U.S. forestry officials estimate. It has been a big loser for some financial investors, among them the country’s largest pension fund. The California Public Employees’ Retirement System spent more than $2 billion on Southern timberland, and harvested trees at depressed prices to pay interest on money borrowed to buy. Calpers sold much of its land this summer at a loss. A spokeswoman for the pension fund declined to comment. It’s also been tough for the individuals and families who own much of the South’s forestland, and who had banked on its operating as a college fund or retirement account. The region has more than six million owners of at least 10 wooded acres, say academics and forestry consultants. Many of the owners were counting on forests as a long-term investment that could be replenished and passed on to heirs.

***

The housing crash 10 years ago worsened the developing timber glut by depressing lumber demand and prompting woodland owners to postpone harvests. Mills closed. Housing has come back in much of the country, pushing prices for finished forest products such as two-by-fours and plywood to historic highs during the spring and summer building season. Prices for logs, as well, have moved up in the U.S.’s other big timber-producing region, the Pacific Northwest, where supply is kept in check by wood-boring beetles and periodic wildfires. In the South, timber prices haven’t stopped sliding. Adjusted for inflation, the price of Southern pine is down about 45% since 2007, according to Daowei Zhang, an Auburn University professor of forest economics. So-called saw timber, for making lumber, is at a 50-year low, adjusted for inflation.

***

In the 1950s, the U.S. Department of Agriculture started dangling forestation incentives to stem erosion and prop up crop prices. At the depths of the 1980s farm crisis, when prices for agricultural commodities plunged, the Reagan administration launched the Conservation Reserve Program. Starting in 1986, it promised farmers annual payments of about $30 to $50 for each acre they planted with trees or grasses. Many seized the offer. By 1994, more than 2.2 million acres of farmland in the South had been converted to pine plantation, much of it in Mississippi, Alabama and Georgia. Other federal forestation programs added about 2.5 million acres more, according to Auburn’s Mr. Zhang. Meanwhile, timber was gaining popularity as an investment idea. People reasoned that trees would grow, and thus gain value, no matter what the stock market did. Investors large and small snapped up forestland that big paper companies put on the market to take advantage of the interest. Researchers reported in 1998 that residual fertilizer in the soil of former farms was helping trees grow faster. A crush of maturing trees arrived just as U.S. housing markets collapsed in 2007 and 2008, creating a supply imbalance that in some places has never ended. Even with increased demand from the housing recovery, there remain about 25 years’ worth of softwood supply in the Southeast, said Brooks Mendell, chief executive of Forisk Consulting, which advises timber investors. In parts of Mississippi and Alabama, the glut is even worse. “It’s unclear we’ll ever have timber prices like we did 10 or 20 years ago,” Mr. Mendell said. Southern mill owners—who buy logs from landowners and resell them as poles, lumber and pulp—anticipate wide margins for years because their raw material is so cheap. Billions of dollars of new saw mills and mill expansions have been announced by the likes of Georgia-Pacific and Canada’s Canfor Corp. Lumber is more practical than logs to haul long distances to stronger markets. The arbitrage inspired last year’s merger of Deltic Timber Corp. and Potlatch Corp. Deltic’s three Arkansas mills offered profits amid depressed prices for Potlatch’s Southern timber. The combined company quickly added a second shift to a mill in Ola, Ark., and a more efficient kiln for drying wood at another mill. More mills could help timber prices, but building one of today’s modern computerized mills, and finding the skilled labor to run it, is a complex task. “Can they install a mill in a rural town in Mississippi and be able to go hire a hundred workers who want to work in a saw mill?” asked PotlatchDeltic Chief Executive Michael Covey at an investor conference in New York this summer. “It’s going to take a few years for those Southern log prices to tip back up.”

|

|

Scooped by

Prentiss & Carlisle

October 2, 2018 12:32 PM

|

Forestry fund Phaunos Timber Fund Ltd said on Wednesday it has rejected Stafford Capital Partners' final cash offer of USD0.52 per share made on Tuesday.

The reasons given for the rejection was due to the offer not being shareholder friendly, and undervaluing the fund, mentioning that the asset realisation process had material upside, ofering in the range of USD0.54 to USD0.60.

Phaunos has advised shareholders to take no action regarding the offer.

Shares in Phaunos Timber Fund were untraded on Wednesday, last quoted at USD0.50.

|

|

Scooped by

Prentiss & Carlisle

October 2, 2018 12:19 PM

|

WITH Brett Kavanaugh’s fraught confirmation battle still raging across the street at the Capitol, the Supreme Court got back to work on October 1st on a quieter note. In the justices’ hands was a three-inch amphibian known as the dusky gopher frog. One of the most endangered species in the world, the dusky gopher numbered 135 in 2015—all of them living near a pond in Mississippi. Weyerhaeuser Co. v United States Fish and Wildlife Service asks whether the federal government erred in 2012 when it designated 1,544 acres in Louisiana as additional “critical habitat” essential to the species’ survival. The area in question belongs to Weyerhaeuser and a few other lumber companies, all unhappy that the Fish and Wildlife Service’s move has, in the words of Timothy Bishop, the company’s lawyer, diminished the value of their land by “tens of millions of dollars”. Mr Bishop told the justices that since no dusky gopher frogs currently reside on his client’s land, and wouldn’t survive there without a transformation of its terrain, the Endangered Species Act (ESA) does not authorise the government to set it aside as “critical habitat”. The land isn’t even the animal’s habitat, he reasoned, so it makes no sense to deem it critical to their conservation. “We would have to totally change the way that this land operates”, Mr Bishop said, “in order to accommodate the frog”. The loggers’ land caught the eye of the agency because it is home to a rare and peculiar geographical feature crucial to the frogs’ reproduction: “ephemeral ponds” that fill up annually and dry out by summer. The larvae and tadpoles develop in these small bodies of water and make it through because there are no fish to gobble them up. But with decreased rainfall and environmental change, ephemeral ponds are in short supply.

***

The colloquy between the justices and the lawyers focused on how significant a change to existing lands the law could reasonably expect. In an extended exchange with Justice Elena Kagan, Mr Bishop granted that if all that was needed was “a very minimal change” like “digging a few holes”, the ESA may permit the government to designate unoccupied tracts as critical habitat. But the dusky gopher frog’s idiosyncrasies also require nearby uplands with open-canopy forests and a particular type of ground cover serving as herbaceous highways between the trees and the ponds. The 1,544 acres would have to be “totally remade”, Mr Bishop argued, to be hospitable to the dusky gopher.

***

Chief Justice Roberts posed the dilemma to Mr Kneedler. If there were ephemeral ponds in Alaska, he mused, “you could build a giant greenhouse and plant the long-leaf pines” there, giving the frog a servicable home albeit at great cost and trouble. Could the government designate such odd spots as critical habitat? No, Mr Kneedler responded, since the law only requires “reasonable efforts” to change the landscape and make it habitable for an endangered species. Planting trees or draining a swamp are reasonable, he said; erecting palatial greenhouses is not. But the chief pressed on: “What’s the limit?” And Justice Alito chimed in: “What’s the definition of reasonable?”

***

It seems the four left-leaning justices are inclined to let the government go ahead with its efforts to protect the dusky gopher, while the four right-of-center justices are not. A split decision lets stand the ruling in the court below, and the Fifth Circuit Court of Appeals sided with the government by a vote of 2-1. So if Weyerhaeuser comes down to a 4-4 divide, the croakers, not the loggers, will reap the benefits.

|

|

Scooped by

Prentiss & Carlisle

September 24, 2018 12:49 PM

|

*** Only seven plans posted double-digit returns in the most recent year, following a year where every plan tracked by P&I but one exceeded 10%. *** Still, none of the plans in the most recent period experienced negative annual returns. The $778 million Austin (Texas) Police Retirement System had one of the lower returns at 7.3% for the year ended June 30, trailing its 9.6% benchmark return.

Pattie Featherston, executive director of the Austin police fund, attributed the plan's performance to several investments within its large allocation to alternative assets that underperformed. The pension fund's asset allocation as of June 30 included 8.8% real estate and 2.8% timber.

The pension fund "has taken a number of steps to redesign the … investment portfolio over the past five years in response to returns that were below expectations," Ms. Featherston said in an email.

This includes increasing its exposure to liquid markets, lowering fees by investing in more U.S. equity index funds, removing timber from its portfolio, repositioning its private equity portfolio and redesigning its allocation to real estate.

|

|

Scooped by

Prentiss & Carlisle

September 18, 2018 10:18 AM

|

Phaunos Timber Fund Ltd said on Monday it is currently considering the increased and final cash offer by Stafford Capital Partners Ltd of USD0.52 per share.

On Friday last week, Stafford vehicle Mahogany Bidco Ltd increased its offer by 6.1% to USD0.52 per share from USD0.49, an 18% premium to Phaunos's USD0.44 per share closing price on June 4. This new offer price values the timber investor at USD259.1 million.

Phaunos also is assessing the offer made by CatchMark Timber Trust Inc, which at USD0.57 per share is higher than even Stafford's improved offer.

Shares in Phaunos Timber Fund were untraded on Monday, last traded at USD0.48.

|

|

Scooped by

Prentiss & Carlisle

September 18, 2018 10:09 AM

|

The largest ever New Zealand forest industry delegation to China's showcase Global Wood Trade Conference has made the case for more investment in New Zealand forestry and timber processing.

Forest Owners Association President, Peter Weir has told delegates at Chongqing that more timber processing in New Zealand, before export, reduced the overall energy and carbon emissions required to produce and transport the finished product.

"There's also a particular opportunity for primary processing of pruned logs in New Zealand rather than the current approach of mixing quality logs with sap-degraded logs and a subsequent loss of value by both parties." Peter Weir said.

New Zealand Forestry Minister, Shane Jones told the conference New Zealand is heavily reliant on access to foreign capital and also has a need to substantially increase its forest reserves.

He said this is behind the government creating a more streamlined process for investment in forestry using foreign capital and this creates a special opportunity for those interested in working with New Zealand. He invited potential investors to consider connecting with the New Zealand industry representatives.

This invitation from Shane Jones comes at a time when there is increasing concern in China with the implications of the US tariffs.

Numerous Chinese speakers at the conference referred to the trade war with the US and that they anticipated this to be a long drawn out battle.

Commentators at the conference believe the impact of increased US tariffs could cost China 1.5% of its GDP.

On the positive side, potential Chinese investors acknowledged the US trade problems were an opportunity to strengthen other trading partnerships and thus welcomed the invitation from Shane Jones.

|

|

Scooped by

Prentiss & Carlisle

September 13, 2018 12:06 PM

|

Finnish development financier Finnfund has committed 10 million USD to a new impact fund for sustainable forestry, the Arbaro Fund (Arbaro).

Arbaro is projected to sequester over 20 million metric tons of CO2 in its lifetime and create more than 5,000 jobs in remote areas. Arbaro aims to invest in and actively manage a well-diversified portfolio of up to 12 sustainable forestry projects in Latin America and Sub-Saharan Africa – regions which are currently characterized by high deforestation rates and an increasing demand for wood resources.

Sustainable forestry is one of Finnfund’s focus sectors because of its high impact on the climate, environment and jobs. Finnfund has invested in ten forestry companies and funds primarily in Africa.

“Sustainable forestry has long been one of Finnfund’s key sectors because the world needs to step up its efforts to fight deforestation and climate change. We expect the Arbaro Fund to play an important role in this vital effort,” commented Finnfund CEO Jaakko Kangasniemi.

Arbaro was established by the global impact asset manager Finance in Motion together with timber sector advisory company Unique. Finnfund brings to the fund its expertise in sustainable forestry. One of the fund’s cornerstone investors is the European Investment Bank (EIB).

The fund marked its initial closing at USD 60.2 million in July 2018, with a target of USD 200 million. Arbaro also aims at solid financial returns, thanks to its target regions’ optimal biophysical growth conditions and high local timber demand.

|

|

Scooped by

Prentiss & Carlisle

September 10, 2018 1:17 PM

|

We unravel the complicated debate over N.H.'s biomass industry. This spring, the governor vetoed two energy-related bills designed to subsidize the biomass. [AUDIO]

|

|

Scooped by

Prentiss & Carlisle

September 4, 2018 3:19 PM

|

The previous post referenced the limitation of simply asking our two screening questions (“Big or small? Long or short?”) when evaluating potential disruptions. Some events affect businesses or investments locally, but not the entire industry or market and vice versa. Big changes can affect us locally, globally, or both. As we have long taught and written, timber markets are uniquely local. For strategy development, we want to specify the context of the disruption to best understand its absolute and relative risks, whether positive or negative.

Finance offers a useful analogy by distinguishing between systematic and unsystematic risks. Systematic risk, also called “undiversifiable” risk, refers to exposures and potential losses affecting the entire market or system, such as interest rates and recessions. Unsystematic risk includes “diversifiable” exposures specific to a given firm or industry. We have little, if any, control over systematic (global) risk, while unsystematic (local) risk can be mitigated and managed through diversification, insurance and other approaches.

***

This high-level framework prioritizes the relative importance of potential disruptions. It separates the local, tactical issues from the global and strategic. Now we apply this approach to a broader set of potential disruptions. *** Figure 6 [above] summarizes an analysis and ranking for ten selected disruptions based on a forest owner point of view (as opposed to a wood user or manufacturer). This ranks first for global (strategic) exposures and second for local impacts. Each assessment has a “story” that changes based on the profile, objectives and assets of the firm. Even at this level, the relative ranking highlights critical themes. - Tax and environmental policies matter.

- People matter.

- Technology matters.

- Demand matters.

Also, time as a strategic idea remains malleable. Discussions with clients and colleagues about potential disruptions reinforce the arbitrary nature of “short” and “long” term in timber. The space and time required for impacts to realize themselves in forestry is beyond the immediate quarter or year (with respect to what the asset can and should do). Value is created consistently over long periods of time, and to the extent we put arbitrary 1 or 5 or 10-year time horizons on the asset, we constrain its performance and change our understanding of the associated risks.

|

|

Scooped by

Prentiss & Carlisle

September 4, 2018 11:59 AM

|

The evidence is in: Urban trees improve air and water quality, reduce energy costs, and improve human health, even as they offer the benefit of storing carbon. And in cities across the country, they are disappearing. A recent paper by two U.S. Forest Service scientists reported that metropolitan areas in the U.S. are losing about 36 million trees each year. The paper, by David Nowak and Eric Greenfield, was an expansion of the same researchers’ 2012 study that found significant tree loss in 17 out of the 20 U.S. cities studied. This arboreal decline is happening even in some areas that promote “million-tree” campaigns, Arbor Day plantings, and street-tree giveaways. Cash-strapped municipalities just can’t find enough green to maintain the green. Additionally, many cities are adjusting to population booms, and to temperature increases and drought due to climate change—both conditions that can be hard on trees (while increasing their value as sources of cooling and cleaner air). There’s also a growing recognition of the inequity of tree-canopy distribution in many cities, with lush cover in wealthy neighborhoods and far fewer trees in disadvantaged areas. To find more funding for urban trees, some local governments, including Austin, Texas and King County, Washington (where Seattle is located), are running pilot projects with a Seattle-based nonprofit called City Forest Credits (CFC). The nonprofit is developing a new approach: generating funding for city tree canopies from private companies (and individuals) that wish to offset their carbon emissions by buying credits for tree planting or preservation.

***

The new credits aim to quantify not only the carbon benefits of urban trees, but also rainfall interception, energy savings from cooling and heating effects, and air-quality benefits. CFC has no role in marketing or selling credits for specific projects, but maintains the standards (protocols) and credentialing for other organizations that sell them. A third-party firm, Ecofor, verifies compliance for tree-preservation projects. Tree-planting projects are either third-party verified, or, for smaller projects that cannot afford that, verified by CFC with peer review, using Google Earth and geocoded photos. To be eligible for the credits, city tree projects must follow protocols created specifically for urban forests—rules governing such specifics as the location and duration of a project and how the carbon will be quantified. The new credits “are specifically catered to the urban environment and the unique challenges and possibilities there, so they differ from traditional carbon credits,” said Ian Leahy, director of urban forestry programs at the non-profit conservation group American Forests, and a member of the CFC protocol board.

***

The fact that credits can cover both stream-side plantings and trees on school property illustrates the complex task of developing a city credit—the protocols and quantification methods must work for the disparate tree species and stewardship strategies of an urban forest, in contrast to the more controlled setting of an industrial plantation.

***

Urban credits will be expensive—many times what a commodity credit for carbon might cost. Urban land is not cheap, and urban trees are costly to plant and maintain compared to those on forest land. However, urban trees offer more public benefits. “Compared to one additional tree left standing in a far-off industrial forest, each additional urban tree we protect has an outsized human impact,” argued Governali, because these trees bring cooling on hot days, better air quality, and even improved mental health. Finally, he noted, the sale of carbon credits from urban trees can help a municipality buy the underlying land and make it a public park, “a place for families to gather, relieve stress, get some exercise, relax, and for children to play and learn.” At the outset, the work adds to already full urban-forest workloads and stretches budgets, at least until credit revenue from buyers can support the programs. “We’re good at planting trees, but documenting the work to create an official carbon credit is new for us,” said Austin’s Baumer. However, generating credits is one more way to stall or reverse tree loss at a time when people are just starting to understand how critical trees—whether elms, oaks, Douglas firs, or cedars—are to a city’s health and economy.

|