Your new post is loading...

Your new post is loading...

|

Scooped by

Prentiss & Carlisle

November 2, 2018 2:58 PM

|

Executives Mark McHugh - SVP and CFO

Dave Nunes - President and CEO

Doug Long - SVP, U.S. Operations

Analysts

Collin Mings - Raymond James

Ketan Mamtora - BMO Capital Markets

Collin Mings ***

Mark, you've spent a lot of time discussing Timberland markets and just return to the asset class over time, just kind of against that backdrop, just maybe talk a little bit about what you're seeing in terms of deal flow. It looks like you guys made a total of about $7 million to $8 million in Timberland acquisitions during the quarter. Mark McHugh I guess, it had a very high level and I'll invite Doug or Dave to comment as well. I'd say we continue to see a pretty robust Timberland M&A market.

***

But overall I'd say we continue to see a pretty steady pace of activity and just to be clear, I'd say the Timberland market as a whole doesn't tend to overreact to the noise that we see in the market around kind of monthly housing stats and things of that nature.

***

Keep in mind, this is an asset class, it's underwritten on a 25-year to 50-year DCF assuming making assumptions regarding long-term sustainable harvest flows and trendline prices and so you know, we tend to not see the private market correct meaningfully relative to these statistics that we see coming on a regular basis. I'd say the China situation is certainly creating some noise in the market.

***

But I'd say overall, discount rates, maybe there's been a bias towards seeking higher IRRs in transactions given the rise in interest rates, but again, Timberland tends to be valued on a real DCF basis and so while the overall interest rate environment fluctuates, it is certainly up over time. I wouldn't say people's view of real long-term discount rates have changed significantly. Ketan Mamtora ***

And then just turning to sort of U.S. south on the domestic side, have you seen with this sharp drop in lumber prices, have you seen any signs of people pulling back on these sawmill projects that have really come up quite a bit over the last 12 months? Are you seeing any signs of people either postponing it or pulling back? Or even sort of any signs of kind of caution on bidding for stumpage? Doug Long Yes, it's Doug again. So we haven't heard of anybody pulling back on their projects. Again, I think a lot of people feel that this is a short term thing and not the long term. So, I think they are continuing moving forward. And delay that we have heard of so far on the sawmills have been more around resourcing and getting equipments and people to work on the projects. So we haven't heard of anyone who specifically said they are pulling back based on kind of what we believe is going to be a short-term correction. On the stumpage side, as probably we have talked about for the last couple of quarters, we didn't see our southern stumpage prices run up with the lumbar. And we also haven't seen them go down with the lumber. So they haven't been correlated to lumber prices at all. And so, I guess while it would have been nice to see them run up with the lumber, the other side of equation they have been very stable and we have just continued moving forward with what's been going on for the rest of the year.

|

|

Scooped by

Prentiss & Carlisle

August 30, 2018 5:43 PM

|

Problems at Phaunos Timber (PTF) continue to mount as the specialist investment company faces legal action from a majority shareholder in one of its New Zealand forestry assets.

The distressed portfolio, which recently rejected a takeover from its former manager, has been hit with a legal challenge from Rayonier, the majority shareholder in Matariki Forestry Group.

It has started proceedings at Auckland’s high court over what it alleges is a breach of confidentiality by Phaunos.

The complaint stems from a valuation report on Matariki which was included in a circular Phaunos sent to investors in response to the takeover offer from former manager Stafford Capital Partners, which Phaunos said ‘significantly undervalued’ the company.

Rayonier, which owns 77% of Matariki, said the inclusion of the valuation breached confidentiality and has served an acquisition notice stating that it now had the right to acquire Phaunos' stake in Matariki for NZ$225 million, equivalent to a 20.5% discount to the most recent valuation by the fund.

|

|

Scooped by

Prentiss & Carlisle

June 26, 2018 11:25 AM

|

Vanguard Group bought more than $2.2 billion worth of data-tower stocks and $1.2 billion of construction-timber stocks from January through last month, and plans to buy more shares of the handful of real estate investment trusts (REITs) in each sector, according to a report.

The Malvern-based investment firm, which manages about $5 trillion in assets, is adding those stocks to its real estate index funds for the first time, writes a team of analysts headed by Ric Prentiss in a report to clients of brokerage firm Raymond James & Associates this morning.

The move makes Vanguard a major owner of American Tower Corp. and Crown Castle International Corp., which own towers that connect the nation’s smartphones and data centers; and of Weyerhaeuser Co., Rayonier Inc., and PotlachDeltic Corp., among other companies that make American construction timber and other wood products.

***

This move to add timber and tower stocks follows Vanguard’s decision last year to broaden its REIT holdings by including sectors it had previously avoided, after Vanguard’s popular REIT index funds became a dominant owner of commercial real estate REITs.

Prentiss reported that “we would expect additional buying demand” by Vanguard for timber and tower REITs, until Vanguard’s Real Estate Index Fund Investor Shares (VGSIX), Real Estate Fund Admiral Shares (VGSLX), and Real Estate ETF (VNQ), which now total around $50 billion in assets, reach their targets, as allocated by the benchmark MSCI U.S. IMI Real Estate 25/50 Index.

*** The company’s buying spree could contribute in the months ahead to “fluctuations” in timber and tower share prices, Prentiss concluded.

|

|

Scooped by

Prentiss & Carlisle

February 13, 2018 8:27 AM

|

Rayonier Inc., through Rayonier Atlantic Timber Co. and Rayonier Forest Resources L.P., sold up to 7,000 acres in St. Johns County last week for $25.24 million. Rayonier, based in Yulee, sold the property to New York-based First Coast Land and Timber LLC, formed in November. The property is between Interstate 95 and U.S. 1 from St. Augustine to Hastings. Alejandro Barbero, Rayonier director of strategic development and communications, said the property was 6,500 to 7,000 acres of timberland in southern St. Johns County. *** Barbero said the offer was unsolicited. “Sometimes we receive unsolicited offers. When it makes sense, we execute on transactions,” he said. He declined to comment on the buyer’s identity or plans for the property. The deed shows that First Coast Timber’s New York City address is the same as Ruane, Cunniff & Goldfarb Inc., a privately owned hedge fund sponsor. It manages Sequoia Fund Inc., described by Bloomberg as an open-ended equity mutual fund begun and managed by the firm. *** Rayonier says in its corporate profile that its growth “is boosted by an excellent portfolio of properties suited for higher and better uses in the fast-growing US Southeast region, primarily in the coastal corridor between Northeast Florida and Southeast Georgia along Interstate Highway 95.” Its Real Estate operation develops strategies to transition timberland “for higher and better uses” while its Forest Resources operation sells timber to markets that include pulp, paper, building products and energy production. In September, Rayonier sold 1,311 acres at its Crawford Diamond Industrial Park in Nassau County to Florida Power & Light Co. for $13.1 million. The utility has not said what it intends to do with the property. Rayonier retains almost 500 acres there. Rayonier also is developing the 2,900-acre Wildlight mixed-use development at northeast I-95 and Florida A1A in Yulee.

|

|

Scooped by

Prentiss & Carlisle

August 14, 2017 6:08 PM

|

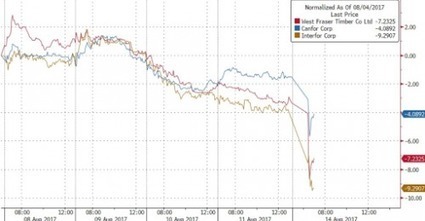

Canadian lumber stocks are diving this morning following a report from BMO analyst Mark Wilde who writes that "prospects for a near-term settlement of the U.S./Canadian lumber dispute have faded", prompting him to downgrade the main players in the space. The report has sent the stocks of West Frasier Timber (WFT), Canfor (CFP) and Interfor (IFP) as much as 6%, 4.6% and 6.2% lower, respectively. *** So with no near-term resolution to the ongoing lumber dispute between the two NAFTA neighbors, the alternative is a steadily progressing trade war. As a result, as Wilde writes, "we anticipate a period of countervailing and anti-dumping duties on Canadian lumber imports as well as continued litigation around those duties." As regards the 3 abovementioned stocks, the analyst notes that at current stock price levels, "we think the big risk is downside disappointments. Thus, we are downgrading West Fraser, Canfor, and Interfor to Market Perform. We are also downgrading Weyerhaeuser and Rayonier ratings to Market Perform. The key issue in timber is continued soft pricing on southern sawlogs. We are not making any changes to our price targets."

|

|

Scooped by

Prentiss & Carlisle

March 20, 2017 4:57 PM

|

Rayonier Inc. (NYSE:RYN) today announced that the company has entered into three transactions with separate sellers to acquire approximately 95,100 acres of high-quality industrial timberlands located in Florida, Georgia and South Carolina for an aggregate purchase price of approximately $217 million, or $2,280 per acre (the “Acquisitions”). The Acquisitions are comprised of highly productive timberlands located in some of the strongest timber markets in the U.S. South, primarily along the I-95 coastal corridor near Savannah, GA.

Key attributes of the Acquisitions include the following: - Strong timber markets – located in the top three U.S. South timber markets based on average composite stumpage price by region (1)

- Diverse customer base – very competitive wood market with multiple pulpwood, grade and export customers

- Highly productive timberlands – 78’ site index; 73% plantable; sustainable yield* of approximately 450,000 tons (or 4.7 tons per acre per year on the acquired lands)

- Well-stocked timber inventory – 4.3 million tons of merchantable timber inventory* (or 45 tons per acre); average plantation age of 14 years

- Complementary to existing Rayonier landholdings – increases Rayonier’s ownership in U.S. South Coastal Atlantic markets by approximately 15%

- Primarily fee simple ownership – 89% fee simple ownership and 11% leased lands

- Accretive to cash flow – targeting an annual increase in Adjusted EBITDA** and Cash Available for Distribution (CAD)** of approximately $13 million and $10 million, respectively, over the medium-term

Rayonier expects to finance the Acquisitions with cash on hand and the proceeds of a follow-on offering of Rayonier common shares, which the company also announced today. ***

(1) Based on Timber Mart-South weighted average composite stumpage price by region assuming product mix of 50% pulpwood, 30% chip-n-saw and 20% sawtimber.

|

|

Scooped by

Prentiss & Carlisle

February 14, 2017 10:38 AM

|

Executives Mark McHugh – Senior Vice President and Chief Financial Officer Dave Nunes – President, Chief Executive Officer and Director Doug Long – Senior Vice President-U.S. Operations Chris Corr – Senior Vice President, Real Estate and Public Affairs Analysts Collin Mings – Raymond James & Associates, Inc. Ketan Mamtora – BMO Capital Markets (United States) Mark Weintraub – The Buckingham Research Group, Inc. Mandeep – RBC Capital Markets Mark Weintraub Okay. And then lastly sort of shifting gears. A fair bit of timberland that might be coming to the market in the next year, year and a half via the TIMOs. How important – is what's going on in interest rates to how these lands are likely to – or how you would view, how you would value these properties? Dave Nunes Well, it’s dynamic. I mean, I think that in some level as you see a rising interest rate environment that rising interest rate environment is predicated on an inflationary environment, which is in turn predicated on higher production – product pricing. So as we see more inflation impacting the price of the products, we expect that that's going to play into the rise in interest rates. We certainly look at it more from – we factor that in as we think about hurdle rates, but we're also looking at it from the perspective our alternative uses of capital and we’re always - when we look at acquisitions understanding how our own timber is trading at the time on an imputed discount rate and we compare that to what we think the market clearing discount rate is on any particular transaction. I don’t know Mark if you want to add anything to that. *** Mark Weintraub Well, and maybe just add one more. Would look that like particularly in the U.S. South that buyers already incorporate substantial appreciation in expected sawtimber pricing et cetera. Now do these same models in your judgment certainly can use your own thought process, do they incorporate meaningful increases in interest rates as well? Or is it that you've actually, the models are getting benefit to price appreciation and not necessarily so much for the interest rates. Of course prices could go up more than what’s imputed, but any thoughts on that? Dave Nunes Yeah, I mean, it probably depends on who you're talking to, I mean everybody – it’s a little bit differently and recognize too that you know a big impact. This really kind of boils down to how you think about discount rates and hurdle rate and it's not only you know, reflective of your cost of capital and alternative uses of capital, but it's also reflective of the flows of capital. What we've seen is that there's been continued interest in the timber asset class from a capital flow standpoint and that has tended to have a dampening effect on cap rates in the sector as people have pushed money into this sector from a flight to quality and just a general conservative investment perspective. So you’ve got some offsetting things at play there.

|

|

Scooped by

Prentiss & Carlisle

May 4, 2016 5:30 PM

|

Rayonier Inc. (NYSE:RYN) today announced the company has completed two separate transactions to enhance its Pacific Northwest timberland portfolio. The transactions include the acquisition of approximately 61,000 acres of well-stocked, highly-productive timberlands in Oregon and Washington, and the disposition of approximately 55,000 acres comprised of predominantly pre-merchantable timber in Washington. On a combined basis, these transactions will smooth the age-class distribution and materially improve the sustainable yield, near-term harvest potential, species mix and market diversification of the company’s Pacific Northwest timberland portfolio. Menasha Acquisition: The first transaction involves the purchase of Menasha Forest Products Corporation (“Menasha”) jointly with Forest Investment Associates (“FIA”), a leading timberland investment management organization (“TIMO”) based in Atlanta, Georgia. Menasha is a privately held timberland REIT with approximately 132,000 acres of timberland located in Oregon and Washington, which since 2007 has been managed by Campbell Global, a leading TIMO based in Portland, Oregon. Rayonier teamed with FIA to acquire all of the outstanding common stock of Menasha. In a subsequent transaction that is expected to close in the second quarter, Rayonier and FIA will distribute the timberlands to various entities, ultimately resulting in Rayonier owning an identified portfolio of 61,000 acres of the Menasha timberlands for a final purchase price of approximately $263 million.

***

The Menasha acquisition (average plantation age of 22.4 years) complements the age-class profile of the company’s existing Pacific Northwest portfolio (average plantation age of 19.0 years). The property is comprised of approximately 85% operable lands and contains merchantable timber inventory of approximately 326 MMBF (2.6 million tons), of which an estimated 83% is Douglas-fir. The acquisition is expected to increase the company’s sustainable yield by approximately 38 MMBF (305,000 tons) per year and increase the company’s average annual harvest over the next five years by approximately 40 MMBF (320,000 tons). Washington Disposition: The second transaction involves the sale of approximately 55,000 acres of timberland located in Washington to FIA for approximately $130 million. The Washington disposition (average plantation age of 12.6 years) evens out the age-class distribution of the company’s existing Pacific Northwest portfolio. The property is comprised of approximately 75% operable lands and contains merchantable timber inventory of approximately 44 MMBF (350,000 tons), of which an estimated 28% is Douglas-fir. Excluding the effect of the Menasha acquisition, the Washington disposition would decrease the company’s sustainable yield by approximately 25 MMBF (200,000 tons) per year; however, average annual harvest over the next five years is expected to decrease by only 9 MMBF (70,000 tons) from this disposition due to the younger age-class profile of the property.

|

|

Scooped by

Prentiss & Carlisle

March 7, 2016 12:39 PM

|

Global forestry group Rayonier posted a 28% drop in earnings from its New Zealand division as softer Chinese demand kept a lid on export prices, and returns from domestic sales were eroded by a weaker kiwi dollar. Source: Scoop NZ Rayonier manages Matariki Forestry Group, the country’s third-biggest forestry company with 13,000 hectares of plantations across New Zealand. Last month the Jacksonville, Florida-based company said its New Zealand division reported adjusted earnings before interest, tax, depreciation and amortisation of US$33 million in calendar 2015, down from US$46 million a year earlier.

***

Rayonier received lower prices in both domestic and export markets from the New Zealand division, with domestic saw timber down 18% selling at US$64.05 a ton, domestic pulpwood prices falling 15% to US$32/ton, and export saw timber dropping 21% to US$88.59/ton. Since the start of 2016, New Zealand log export prices have been benefiting from cheap oil providing lower shipping costs, offsetting the muted demand from China.

***

The group added another 1800 hectares of forestry rights in 2015 at a cost of US$9.9 million. Last year, Rayonier injected NZ$242 million of capital into Matariki to increase its stake to 77% from 65%.

|

|

Scooped by

Prentiss & Carlisle

November 4, 2015 4:12 PM

|

Interesting exchanges re valuation, timberland markets and values:

Mark Wilde - BMO Capital Markets (United States)

Okay. And then, I guess as you kind of think about acquisitions kind of going forward, it just – from the outside, it's kind of hard to see how any acquisition can – because when Southern timberland, it seems to be being valued at about 2.5% to 3% on an EBITDA basis. Hard to see how any of those acquisitions can look better than your own stock yielding above 4%? David L. Nunes - President and Chief Executive Officer

Well, and this, I think this really speaks to why we've had a fairly limited number of acquisitions that we've gone after this year. We've closed on eight acquisitions. They've generally been on the smaller side and I think the fact that in Q3 all of our capital really was allocated to share repurchases, speaks to that yield dynamic that you just referenced. But there are occasional acquisition opportunities that do present higher yields, and I think that we have seen as well on the properties that we've purchased that we don't mind paying up for properties that are highly productive. And I think that's another element of the higher yield properties is they tend to be on higher quality properties. So we look at it as having bought stronger factories, if you will. Mark Wilde - BMO Capital Markets (United States)

Okay. All right. Then the last question I have, Dave, is just on sort of what's going on in terms of the M&A market right now. You've had two big deals out there in the market, Foley and CalPERS both of which I think have a little bit of hair on them, but what's your sense of those deals and then what's in the sort of what seems to be in the pipeline beyond them? David L. Nunes - President and Chief Executive Officer

Well, I'd say there is a fair bit of transactions that are out there in the pipeline. Foley is still working its way through and we understand that there was a sale in the works out of a portion of the CalPERS properties in Louisiana and really until we learn more about the values on those, it's hard to comment from a qualitative standpoint. *** I also would say that there are quite a number of acquisitions that were made a decade ago by a number of TIMOs that are starting to near the end of their 10-year term. And so, we anticipate that we're going to continue to see properties put out on the market. And for those that have a good fit with what we're looking for, we'll take a hard look at them.

***

Mark Wilde - BMO Capital Markets (United States)

Okay. And then the last question I had is just a little longer term one for Dave. And I wondered if you would just comment on this sort of disparity that exists out there from a valuation perspective between kind of public market and private market and how you think that disparity might move over time? Because it seems to me it's kind of ebbed and flowed a bit. David L. Nunes - President and Chief Executive Officer

Yeah. And I think you also have to recognize, Mark, that I think there have been times where that disparity has been influenced from a data standpoint that perhaps people have drawn the wrong conclusions on. For example, there was a period over this last cycle where a lot of people were comparing NCREIF results to private market results or to public market results and NCREIF appeared to be defying gravity, if you will. But at that time, NCREIF was allowing companies to do internal valuations. And so it contributed to some of that gap in value. NCREIF has changed that policy now to where all properties in the index have to go through a third-party appraisal. But recognize third-party appraisals aren't always perfect, and so I think you still have noise on that front. And then even in the transactions market, you're going to see differences in terms of stocking level and productivity that may or may not be apparent to the outside player. And then as it relates to the public market valuations as we and others have talked about, the South in particular is not a homogeneous market. You've got big differences in value. And I'm not sure that we're a believer in what you hear of, say, a new normal of pricing. I think it really depends on the attributes of the property, the stocking, the growth rates, et cetera.

|

|

Scooped by

Prentiss & Carlisle

June 30, 2015 10:24 AM

|

Rayonier Inc. RYN, -0.51% announced today the company has acquired approximately 18,000 acres of high-quality timberlands in southwest Louisiana and northwest Oregon in two separate transactions from BTG Pactual Timberland Investment Group. Both properties are located near existing Rayonier landholdings:

The Louisiana property – known as the King parcel – consists of approximately 12,200 acres of high quality, well managed southern pine timberland located in strong timber markets. The property was purchased for $25.5 million. It contains merchantable inventory of approximately 560,000 tons, is comprised of approximately 86% plantable lands, and is expected to improve the company’s sustainable yield by approximately 45,000 tons per year. This acquisition expands Rayonier’s ownership in Louisiana to approximately 150,000 acres.

The Oregon property – known as the Scappoose parcel – consists of approximately 5,600 acres of highly productive, well-stocked and highly-operable timberland tributary to strong domestic and export markets in the northwest corner of the state, near current company holdings in southwest Washington. The property was purchased for $34 million. It complements the age-class profile of the company’s Pacific Northwest timber holdings, contains merchantable inventory of approximately 102,000 tons (12.7 MMBF) of which an estimated 95% is high-value Douglas-fir, is comprised of approximately 88% operable lands, and is expected to improve the company’s sustainable yield by approximately 35,000 tons (4.4 MMBF) per year. This acquisition expands Rayonier’s footprint into the state of Oregon and grows Rayonier’s total Pacific Northwest ownership to approximately 374,000 acres.

|

|

Scooped by

Prentiss & Carlisle

May 8, 2015 11:07 AM

|

Collin P. Mings - Raymond James & Associates, Inc.

Hey. Good morning, guys. I guess my first question, both for Dave and Mark, just as it relates to the balance sheet and cap allocation priorities, clearly you bought some more Timberland during the quarter, but just given the weakness in the stock price, you're down 7% year-to-date. What's the latest thinking as far as maybe looking at buying back some stock? Mark McHugh - Chief Financial Officer, SVP & IR Contact

Yeah, Collin, we don't currently have a buyback authorization in place, but with our stock around $26 per share, we certainly believe that it's trading well below net asset value. So, share buybacks are something that we are actively evaluating. Ultimately, we have to evaluate share buybacks versus other uses of capital like acquisitions and make judgments about where we believe we have the best opportunities to drive shareholder return. We recognize that from a pure NAV standpoint, our current stock price implies a value per acre that is cheaper than where we can acquire Timberlands in the M&A market today.

***

Collin P. Mings - Raymond James & Associates, Inc.

Okay. And then well, I guess just going back to this theme, Dave, of value that's being implied by the public markets right now versus what we're seeing on private deals that are getting done. Just any thoughts about how you think about the potential M&A in this space, the Timber REITS, a couple of the other timber-focused companies that are out there and just maybe just your thoughts about the NAV disconnect right now we're seeing in the marketplace? David L. Nunes - President, Chief Executive Officer & Director

Well, I think that you have to be very careful in an environment like this where we've seen less deal flow as we've started 2015 relative to where we started 2014. And so you have to be really careful drawing too many conclusions from that because you've got quite a wide range of quality in terms of the properties and so I don't pay as much attention to those few comparable sales because they just not representative of broad market averages, and I think I'd repeat what Mark talked about.

***

Paul C. Quinn - RBC Dominion Securities, Inc.

Yes. Thanks very much. Good morning. Just a question on the M&A front, you guys were successful with the 12,000 plus acres in Q1. How was that done? Were those auction processes and what's your assessment of the current competitive landscape out there? David L. Nunes - President, Chief Executive Officer & Director

We continue to have a mix of participation in both negotiated and auction deals. That particular one was through an auction process. And again, our view is that we're going to be more competitive on transactions that have a fair bit of complexity to them. We have a strong HBU rural land sales effort. And so, whenever we have a property we will have our Real Estate sales guys assess it as part of our due-diligence efforts. And we think in that particular example that helped us be more competitive. We are also, we also are tending to look for properties that we've got an existing presence from a geographic standpoint to keep our management costs low. And so most of the acquisitions that we've done over the last year, year and a half have all been in areas that are – I would consider to some degree bolt-on transactions.

|

|

Scooped by

Prentiss & Carlisle

November 18, 2014 10:00 AM

|

On Monday, along with announcing its 3rd quarter results, Rayonier also announced: - That it had erred in its inventory as stated on the 2013 10-K.

- That it had been harvesting at a rate higher than the sustainable rate on its Pacific Northwest properties, and would henceforth lower the harvest rate in the Pacific Northwest.

- That it would reduce its dependence on non-strategic timberland sales to generate cash.

- That it would reduce its dividend from $.30 a quarter to $.25.

- That because of the inventory error, it had under-reported its depletion expenses for the 1st and 2nd quarters of 2014, and would take an additional $2.6 million expense in the 3rd quarter to correct this.

For these grievous crimes, its market price dropped from $33.90 to $26.09 today, a 23% drop.

*** - I'll sum up my view on Rayonier's mea culpa as follows:

- The inventory issue is unfortunate but not that important in the big picture.

- The harvest drop in Washington is unfortunate but not out of the ordinary in the world of forest inventories and forests with older age classes.

- Reducing reliance on non-strategic timberland sales is a good thing.

- Reducing the dividend is unfortunate but understandable.

- Depletion, who cares.

Of all the things listed above, only numbers 4 and 5 were necessary from a legal standpoint. Issues 1, 2, and 3 could have been handled as internal management issues. It is only, in my opinion, because of Dave Nunes, the new CEO's strong belief in transparency that they were reported. Had that not been the case, I believe the 23% drop in unit price would not have been as bad. I think transparency is good but sometimes too much is not.

Let's look at Rayonier's land holdings. Counting Rayonier's 65% interest in 300,000 acres in New Zealand, Rayonier owns about 2.6 million acres of land. Using $1,800 per acre for southern timberlands, $3,000 per acre for northwest timberlands, and $2,000 per acre for New Zealand lands, Rayonier's timberlands are worth about $5 billion dollars, or about $39 per unit. Take away the $605 million long-term debt and you get about $34 per unit.

So, if Rayonier shuts down today and sells itself on the open market, it would be worth about $34 a unit. It is selling now for about $26. If I had a little cash lying around, and was a long-term investor, I might be tempted to pick up some RYN at $26 and get a 3.8% dividend to boot.

|

|

|

Scooped by

Prentiss & Carlisle

September 10, 2018 1:12 PM

|

The battle for Phaunos Timber Fund (PTF) has intensified with CatchMark Timber Trust (CTT.N), a US real estate investment trust, announcing it is considering a $0.57 per share equity offer.

The potential bid beats a rival offer of $0.49 per share in cash from Phaunos’ former manager Stafford Capital Partners and would see shareholders receive around $284 million in CatchMark shares.

Phaunos, which holds its annual general meeting in Guernsey this afternoon, has responded by saying it will ‘engage with CatchMark to understand fully its proposal’ which represents a 16.3% premium to Stafford’s offer.

Jerry Barag, CatchMark president and chief financial offer said: ‘The Phaunos portfolio fits our existing strategy for acquiring institutional quality assets with superior productivity that can generate durable growth for our stock holders. It presents a compelling opportunity worth our study and analysis.’

***

Liberum analyst Conor Finn said CatchMark’s indicative offer looked attractive but questioned whether CatchMark shares would be a good fit for Phaunos investors.

‘We believe most of the Phaunos share register would not be long-term holders of CatchMark. This is likely to create downward pressure on CatchMark’s share price,’ he said.

***

Phaunos' board has rejected Stafford's bid as undervaluing the company, saying it will deliver more value for shareholders with an orderly wind-up and sale of its investments. Stafford has denied this saying the board's asset realisation programme will be slower and far more uncertain than its offer.

The bid tussle has embroiled Phaunos in a legal row with Rayonier, the majority investor in New Zealand's Matariki Forestry Group which represents three quarters of the company's assets. Rayonier says Phaunos breached a confidentiality agreement by publishing a valuation of Matariki in its formal response to Stafford's offer. It claims it now has the right to buy the rest of Matariki at a 20% discount, which if true would diminish the break-up value the board is seeking.

|

|

Scooped by

Prentiss & Carlisle

August 2, 2018 4:48 PM

|

Ketan Mamtora And last question, there has been some press recently around reworking the Endangered Species Act. Do you think there was any possibility that the federal lands could be opened again on the Pacific Northwest for harvest I mean for most of us we haven't seen that at all in the last 25 to 30 years but do you think there is any possibility that could happen? David Nunes That would surprise us. I think that recognize that you have virtually no manufacturing capacity in place that could even handle that wood if it were to occur. And I think that we've just gone too far down that line you know from a policy standpoint. So I think that that's not something that we think is really on the horizon.

***

Mark Weintraub Two quick questions one on the Timberland sales that you're seeing out there. Is this primarily an auction type processes or are you talking about more situations where it's you and maybe a contiguous owner et cetera? David Nunes It's really both. We're always in discussions with neighbors whether it's on the buy side or the sell side. Those are obviously logical situations and then there's always a decent mix of negotiated sales versus auction situations and different sellers have different preferences around doing that and it's our job to sort of understand both the landscape there in terms of properties that may or may not be for sale as well as the preference of those owners in terms of how they take it to market. Mark Weintraub And in those situations where it is more auction process, is there any shift that you could describe as to what seems to be going on in the processes relative to what we've been seeing in the last couple of years? I know that's a tough question to answer but any color you could give? David Nunes I am sorry, what do you mean by that Mark in terms of what's going on in those processes. I mean they remain very competitive I mean we certainly haven't seen demand for timberland properties trailing off and in fact we haven't been very successful in auction processes in the last couple years. Mark Weintraub And that's really what is trying to get out is I mean you haven't been very successful because it's been so competitive. Is there any reason to think that you're that much more likely to be successful in the auction type processes or I assume if it still remains very competitive. It's more likely you're going to be in the more private type of negotiated transactions? David Nunes I'd say the bulk of the activity that we have acquired has been and negotiated transactions. No question, that doesn't mean that we don't still take a crack at auctions and we have a low batting average there that we're proud of. You don't want to have a high batting average in auctions frankly.

|

|

Scooped by

Prentiss & Carlisle

June 15, 2018 11:15 AM

|

Yulee-based Rayonier Inc. bought about 18,000 acres of timberland last week in St. Johns and Flagler counties for almost $24 million.

It bought the land from Wilson Green LLC, part of Greenfield Partners, a Connecticut real estate investment company, according to our Jacksonville Daily Record news partner.

Rayonier hasn’t said what it will do with the land.

“As a public company, we don’t comment on acquisitions or divestitures outside of our ordinary public disclosures or other public release,” said Alejandro Barbero, director of strategic development and communications.

Barbero said in February, after a sale of timberland, that “We are a timber REIT and we continuously evaluate our portfolio.”

Rayonier, through Rayonier Atlantic Timber Co., paid $16 million for almost 12,416 acres of timberland in southern St. Johns County and almost $8 million for about 5,392 acres in Flagler County.

The purchase works out to about $1,347 an acre.

The St. Johns County property is near Interstate 95 and Florida 206 West in Hastings and St. Augustine. The Flagler County land is just south of that.

|

|

Scooped by

Prentiss & Carlisle

February 9, 2018 5:13 PM

|

*** Ketan Mamtora - BMO Capital Markets (United States) All right. That's helpful. And then, just turning to U.S. South, my final question. Do you still think that 1.3 million, 1.4 million housing starts is about where the inflection point is for Southern log pricing? Or there has been any rethink around that or maybe in terms of just lumber consumption in the U.S. South? Any thoughts there will be helpful. David L. Nunes - Rayonier, Inc. I think the message that we have been trying to communicate with investors is it really depends on the market that you're in. And recognize that the U.S. South really consists of a series of smaller markets and we believe that there are subsets within the South, particularly today, in that Atlantic coastal region where we are essentially at a fairly tensioned market where we see price elasticity such that when we have changes in lumber prices we see that translate more rapidly into changes in log prices, whereas in other parts of the U.S. South, we're not seeing that as much. We believe that the inflection point in some of the softer markets in the U.S. South is probably above the 1.5 million housing start level. So there will be parts of the U.S. South where you probably won't see meaningful price increases for a couple of years.

***

Steven Pierre Chercover - D.A. Davidson & Co. Thanks. Good morning. So I too had a question on New Zealand. Only a couple years ago, the guidance for the region was less than $30 million at the high end and now the midpoint is triple that. So is that a function of increasing consolidation as you've increased your stake or is profitability changed that much? David L. Nunes - Rayonier, Inc. I think it's been a number of things, Steve. There has been modest increases in the footprint, but I'd say it's more driven by a combination of strong markets and favorable shipping, logistics costs. You had a period where we had an abundance of vessels that service the log trade, combined with low oil prices that translated in some of these periods record low shipping rates at a time when you had very strong demand across the spectrum. We saw as well increasing substitution within China, particularly on the plywood side, where we saw more radiata flowing into plywood, so that today roughly 30% of radiata goes into plywood. We also saw the ban on the harvest of native forests in China, due to overharvesting over a period of time. So that translated into a restriction on domestic supply at the same time that you had a strong growth in demand. And so the China market for logs has grown, while the domestic supply has shrunk and New Zealand has just been very well situated to compete in that market, both in terms of where those logs compete both geographically and product wise and then to combine that with very favorable shipping rates. So across that spectrum, I'd say it's a much heavier mix from a margin standpoint.

|

|

Scooped by

Prentiss & Carlisle

May 9, 2017 8:51 AM

|

Dave Nunes - President & CEO Before discussing our results for the quarter, I'd like to briefly address our recent equity offering and portfolio moves in the U.S. south. On March 16, we announced that company had entered into three transactions to acquire approximately 95,100 acres of high quality industrial timberlands located in Coastal Florida, Georgia and South Carolina. We recently closed on the transactions for a final aggregate purchase price of $214 million or roughly $2250 per acre. We're very excited about these acquisitions as they meaningfully increase our footprint in some of the strongest markets in the U.S. south. Further, these properties are highly productive with an average site index of 78 feet and average productivity of 4.7 tons per acre per year. Over the next five years we expect that these properties will contribute on average roughly 13 million of incremental adjusted EBITDA per year to our Southern Timber segment. So while these properties transacted at a relatively high per acre value reflective of their high quality, we expect them to generate a strong cash yield and an attractive long-term return for our shareholders.

***

Mark Wilde - BMO Capital Market Okay. And then finally Dave if I could one of the trade papers recently had an article suggesting some cooling in the Southern timberland markets I assume you seen this and I wondered if you had any thoughts on that? Dave Nunes - President & CEO Our view is always been that it really is quality dependent and I think that you’re seeing a mix of quality assets there's plenty of deal flow right now but there's a mix of assets. Certainly at one end of the spectrum you have the transactions that we recently completed, that were very high quality assets in high quality markets. There are other assets that are going to be at lower quality and I think that depending on how you look at markets and which of those assets you're looking at, it’s going to color your view of markets. But I think we still are seeing strong market dynamics in terms of capital trying to get into the asset class and I don't know that we espoused to the markets cooling as much as we do really been driven by the quality of the assets that are out there.

***

Steve Chercover - Davidson My last question again, forgive me if I might've missed it, but in southern sawtimber, the price is about as flat as a board. So when do you expect tension in that market that will help elevate prices? Dave Nunes - President & CEO I think it's quite variable. In our discussions with investors, we are focusing on the relative build in inventory across the U.S. south and we continue to believe and see that there is going to be very variable price elasticity going forward. And in some of our more tensioned wood baskets, we're experiencing that price elasticity now and in other wood baskets that are less tensioned, we're not. And I think it it's been to some degree exacerbated by the weather factors and the demand reductions associated with these two pulp mill incidents that Doug referenced that I think have exaggerated perhaps some of the effects. The La Niña conditions that have currently translated to a lot of dry weather in abundance of supply, as well as the demand reduction, neither of those two things are going to be long-term in nature.

***

Chip Dillon - Vertical Research And then maybe lastly when you think about the 95,000 acres you bought they all seem to be relatively close to I95 and I know there is some very empty spaces still along the highway. But that doesn't mean that in five or 10 years whether it’s warehouses or other types of development could occur. Is there some optionality on these 95,000 acres in your mind, you might not have valued it as such when you made your deal, but do you think it's reasonable that if things progress that you could see some HBU potential among these acres? Mark McHugh - SVP & CFO I expect that we’re going to sell probably 20,000 to 30,000 acres a year into those HBU markets. And you kind of see the price premiums. I think the last couple years we've averaged 2500 to 2750 an acre, so that kind of gives you a sense as to our kind of run rate expectation for that business and I think it was generally kind of translate into a similar range to what we're forecasting for this year. And so as it relates to the upside potential in the recent acquisition you know it’s absolutely something that we see is creating some upside over time. We didn’t underwrite it into our acquisition underwriting. We didn’t need to. This was a property from a timber standpoint really supported the valuation without that but clearly these markets are again in that sort of path of growth in the I95 corridor and so we do see some upside there over time keeping in mind that because the timber value here is so high it’s sort of hurdle rate to actually sell into that HBU market is going to be materially higher as well. Dave Nunes - President & CEO Chip another thing to think about it is that there's a portion of those assets that actually have HBU value from an agricultural conversion and that's not something that you see very often, but it speaks to when you have site index that’s that high and you see surrounding lands that are in active agriculture, it’s suggestive of that.

|

|

Scooped by

Prentiss & Carlisle

February 28, 2017 12:25 PM

|

The Hancock Timber Resource Group has completed the acquisition of approximately 25,000 acres of timberlands in Alabama from Rayonier Inc. This transaction is a follow-on to another transaction completed in late 2016 where Hancock Timber acquired approximately 37,000 acres of timberlands in Mississippi and Alabama from Rayonier. "We are very pleased to secure additional high quality timberlands for our clients," said Hancock Timber Resource Group President Brent Keefer. "These properties are located in an area of the US South with deep and diverse markets for forest products. We will be able to supply solid wood and fiber to a variety of facilities in southern Alabama, western Georgia, and northern Florida. We look forward to managing them to their highest potential." As with the previous acquisition, the timberlands are stocked with well-managed southern pine plantations and hardwoods. The timberlands will be managed by Hancock Forest Management, the organization's integrated property management group. Hancock Timber has approximately 280,000 acres of timberland under management in Mississippi and Alabama, 1.8 million acres in the US South and almost six million acres globally.

|

|

Scooped by

Prentiss & Carlisle

August 4, 2016 7:04 PM

|

Chip Dillon - Vertical Research Partners Yes. Hi. I just had a general question about you gave a great slide on your M&A acquisition strategy or timberland acquisition strategy. When you look at today's like interest rate environment, if you were to debt finance timberland sort of at some of the asking prices you're seeing in areas that might be of interest to you, would you say the spread looks good to you, or it's not very favorable? How do you sort of compare the cap rates and the returns you're seeing with the financing costs? Mark McHugh - Senior Vice President and Chief Financial Officer Yeah. I mean we continue to think that in the M&A market sort of the going rate from a DCF, a discount rate standpoint, is in probably the 5% to 5.5% range. And that could swing on – 5% to 5.5% real, which would be net of inflation. And the deals I'd say that we're more focused on tend to be deals that are delivering the majority of that or vast majority of that in cash flow. And so we're frequently looking at deals that have relatively strong cash yields relative to that discount rate. Certainly with where we're able to finance in the debt markets today, there is a pretty healthy spread, call it, 200 basis points to 300 basis points to our debt financing rates.

***

Mark William Wilde - BMO Capital Markets (United States) Yeah. I think you might have answered a big part of my question when you answered Chip's. I was just curious with these very low interest rates whether you're seeing any kind of downward pressure on discount rates? David L. Nunes - President, Chief Executive Officer & Director I'd say that they've held relatively firm in the last – probably in the last 18 months. Again, what we've seen is differential discount rates for different quality transactions. Again, I think on average, across the U.S. South we think the going rate is in that 5% to 5.5% real, but we've seen people pay up for very high quality properties. Likewise, we've seen some no sales and some transactions that certainly traded above that just relative to the risk of the particular portfolio or the inventory mix and the maturity of the age class. Mark William Wilde - BMO Capital Markets (United States) Okay. Mark, I know over time there have been points where a lot of the activity with the TIMOs has come from kind of offshore money and with rates so low over in Europe right now, are you getting a sense that the TIMOs are seeing more offshore money coming in? David L. Nunes - President, Chief Executive Officer & Director I think that's probably true, Mark in both the private equity as well as some of the public equity. I mean I think you're seeing more of it as well in the context of investors into the timber REIT space, but I think that we're continuing to see fairly healthy demand for timber from offshore capital for all of the reasons that you would expect, sort of flight to quality, the low interest rates in Europe as an example. You're seeing yield, people coming here for safe yield, and so I don't think we've seen any dissipation of that type of capital flow. Mark William Wilde - BMO Capital Markets (United States) Okay. And then last question, kind of along the same lines. Dave a while back you mentioned to me that you thought that actually discount rates were still wider down in New Zealand. Have you seen any tightening there? David L. Nunes - President, Chief Executive Officer & Director New Zealand has less deal flow certainly than the U.S. And so you don't have as many data points. I think that there have been some recent transactions in New Zealand where we've seen lower discount rates than what you typically see in a lot of appraisals. So I think one of the things to keep in mind with New Zealand though is that a lot of the land in New Zealand is tied up in long-term leases or in forestry rights. And so those leases, I think, tend to contribute to a higher blended discount rate in New Zealand, relative to say, to the U.S.

|

|

Scooped by

Prentiss & Carlisle

March 31, 2016 11:01 AM

|

Phaunos Timber Fund Ltd on Wednesday said its partner on the Matariki Forestry Group project in New Zealand has provided capital to refinance the company.

Rayonier Canterbury LLC, the majority owner of Matariki, has provided the capital for the repayment of all outstanding amounts owed under Matariki's NZD235.0 million credit facility.

The move will result in Matariki's annual interest costs falling around NZD15.0 million, Phaunos said.

Following the recapitalisation, Phaunos' stake in Matariki will be diluted to around 23% from 35%, but the company said the value of its investment has not been diluted.

Phaunos shares were down 4.2% to 0.34 pence.

|

|

Scooped by

Prentiss & Carlisle

February 15, 2016 1:26 PM

|

Collin P. Mings - Raymond James & Associates, Inc. Do you think that there could be any risk to some downward pressure in timberland values just as that timeline – particularly in the U.S. South is that timeline for a recovery in the South continues to extend? David L. Nunes - President, Chief Executive Officer & Director Well, certainly that potential exists. I think that this going to be a function of the capital flow – recognize you have offsetting elements to that with net capital inflows coming into this sector, particularly in these uncertain market conditions, I think we tend to see timber as a flight to quality and that have some offsetting impact. As we have looked at market clearing prices on recent transactions it does not appear that those values are moderating as you suggest. But it certainly always remains a potential in any market.

***

Steven Pierre Chercover - D. A. Davidson & Co. Great. And then a lot of these things have already been addressed, but the way you consider repos versus new land acquisitions, when you consider that a repo eliminates a 5% dividend yield, I can't imagine that you could buy land with a discount rate lower than that. Mark McHugh - Senior Vice President and Chief Financial Officer I think market discount rates in timberland today continue to be in the range of 5% to 6% real. Now, that's a kind of all-in discount rate which will count for a number of other assumptions that go into it. But I'll say that we have generally been focused on properties that are more productive than average. And so, I think that the cash yield that we're seeing on the properties that we've been buying have generally been in that same type of zip code Steve.

***

Mark McHugh - Senior Vice President and Chief Financial Officer I think that our U.S. South acreage is trading below $1,300 an acre today. That is pretty cheap by any measure over the last decade or so. The NCREIF Index, even in the face of the housing crisis, I think the lowest that it got in that period was about $1,475 per acre. And what was driving that economic crisis was a downturn in the – collapse of the housing market – which had a much more direct impact on timberland values than kind of what we're seeing in today's market. And so, by any measure, it certainly feels as though the stock is cheap and certainly feels as though it's trading at a significant discount to NAV. But we are constantly refining our views around NAV, and again, we're not indifferent to kind of looking it, stress testing kind of different pricing scenarios with different sort of outlooks for the economic situation. David L. Nunes - President, Chief Executive Officer & Director George, I'd just add to that too, that I don't think that we're seeing a net reduction in capital flows coming for this asset. We are continuing, this asset class is continuing to mature and I think as it does so and becomes more of its own unique asset class, it's attracting capital from other regions and other sectors of the market. And we see that in the context of the asset values as we discussed earlier in the call, you know, we're just not seeing the fall off that you described as being a potential, but we certainly look for that.

***

Chip A. Dillon - Vertical Research Partners LLC Got you. And then just real quickly, I am sitting here thinking, 10 years ago, 12 years ago, you had sort of a rush of pension plans going into timberland, is it asset class, and that created a real pushup in values. And I guess our concern have been that as they – these partnerships come to an end, you might see a lot of, or maybe some excess supply in the market. Although, today in the real world, if I'm running a pension plan, my choices are, I can pay the German government to take my money, or I am getting a 1.59% for 10 years from the U.S. government. And you, I think Mark mentioned the discount rates, my guess is that, that fear is completely off the table. And maybe what I think is different about timberland is that it's a 50-year to 70-year asset and the durations really long, and kind of doesn't matter where lumber is today. And I guess my question is, are you starting – when you think about those realities, are you starting to actually see increasing interest from, pensions has been down, but you really have very few other places to go? David L. Nunes - President, Chief Executive Officer & Director Chip I think that you hit it right on the head, and to some degree this gets back to what I was talking about earlier in the call. You have to look and try to get a grasp of the net capital flows in the market. And I would say that we're still at a stage where there are lot of pension plans and other long-dated endowments and the like, there are lot of those sources of capital that are in timber, but there is a lot that that are trying to get into timber.

And I think we see that in the context we're not seeing a lot of decline in asset values on transactions, because you know while you have some of those transactions from a decade ago coming back to market and may be in some cases people exiting the market, I think you've got plenty of others coming on to the market. And certainly, as you look at negative interest rate environment in Europe, I think we're seeing a continued growth in European capital in this asset class. We see it on the TIMO space, more and more capital flowing into the TIMO is European capital, and I think it's a flight to quality, it's a yield, it's a yield play as you described.

And so, we think that helps kind of buttress the asset class that we're in and keeps those private market values at a relatively stable level notwithstanding the broader uncertainty in the rest of both capital markets and product markets.

|

|

Scooped by

Prentiss & Carlisle

August 12, 2015 9:44 AM

|

Phaunos Timber Fund Ltd on Thursday said it has reached an agreement in principle with Rayonier for a capital infusion into their Matariki Forestry Group joint venture in New Zealand, which will allow the venture to repay all outstanding amounts under its existing NZD235 million credit facility.

The deal is expected to close by the end of the year and should generate NZD15 million a year in cost savings, Phaunos said.

"The reduction of the Matariki joint venture debt has been a key objective for both the directors of Phaunos and Stafford Capital Partners since the latter became manager in July 2014," said Stephen Addicott, a partner with Stafford Capital Partners, the manager of the Phaunos fund.

"The transaction, based on Matariki's net asset value, is not expected to involve any loss of value or loss of rights under the existing shareholders agreement," Addicott added.

|

|

Scooped by

Prentiss & Carlisle

June 17, 2015 12:16 PM

|

Rayonier (NYSE: RYN) announced that the company’s board of directors has approved the repurchase of up to $100 million of the company’s common shares. Repurchases may be made at management’s discretion from time to time on the open market or through privately negotiated transactions. The repurchase program has no time limit and may be suspended for periods or discontinued at any time.

"This share repurchase authorization is an important component of our capital allocation plan, underscores our commitment to creating value for shareholders, and demonstrates our conviction in the underlying net asset value of the company relative to the current share price," said David L. Nunes, president and CEO.

|

|

Scooped by

Prentiss & Carlisle

April 1, 2015 4:46 PM

|

The Nature Conservancy has purchased 3,184 acres of Rayonier timberlands in the Hoh River drainage in a $7 million acquisition that is part of a broader forest-restoration effort on the Olympic Peninsula.

The land sale, which closed Monday, will help in the creation of a 32-mile conservation corridor extending from the Olympic National Park to the Olympic Coast National Marine Sanctuary.

The river corridor provides critical habitat for marbled murrelet, northern spotted owl, bald eagle and bull trout, and supports native salmon and steelhead runs, according to a statement released Monday by the Nature Conservancy. Plans for the conservancy land includes planting trees, restoring fish and wildlife habitat and some long-term rotation timber harvests.

|