THE CORPORATE REPUTATION OF THE PHARMA INDUSTRY IN 2015: THE PERSPECTIVE OF 90 PATIENT GROUPS with an interest in HEART AND CIRCULATORY CONDITIONS (2nd edition) London, Monday 7th November 2016. This report is based on the findings of a PatientView November 2015-January 2016 survey exploring the views of 90 patient groups with an interest in heart-and-circulatory conditions. These patient groups came from 35 countries (14 of the 90 were based in Denmark). The report provides feedback (from the perspective of these patient groups) on the corporate reputation of the entire pharma industry during 2015, as well as on the individual performance of 15 pharma companies at six key indicators that influence corporate reputation. The 2015 heart-and-circulatory results are compared with the responses received in 2014 from patient groups in the same therapy area, as well as with those provided by patient groups from across all therapy areas in 2015. For the purposes of this report, the phrase ‘corporate reputation’ is defined as the extent to which pharma companies are meeting the expectations of patients and patient groups.

The 90 heart-and-circulatory patient groups responding to the 2015 ‘Corporate Reputation of Pharma’ survey were more positive about the pharma industry’s corporate reputation than heart-and-circulatory patient groups responding in 2014 (but not as positive as urinary and diabetes patient groups in 2015).

As many as 51.2% of the 90 patient groups with an interest in heart-and-circulatory conditions and responding to the 2015 ‘Corporate Reputation of Pharma’ survey stated that the pharma industry as a whole had an “Excellent” or “Good” corporate reputation that year. The equivalent figure for patient groups from across all therapy areas in 2015 was 44.7%. Patient groups with an interest in heart-and-circulatory conditions ranked the pharma industry 4th out of 8 healthcare-industry sectors for corporate reputation in 2015—ahead of private healthcare, generics, and both not-for-profit, and for-profit health insurers. In 2014, heart-and-circulatory patient groups also ranked pharma 4th out of 8 healthcare-industry sectors, but with a much lower average score. Pharma was ranked 5th in 2015’s global results.

Why has pharma’s corporate reputation improved among heart-and-circulatory patient groups? One reason may account for the rise in pharma’s approval ratings among heart-and-circulatory patient groups—pharma’s growing output of innovative medicines. When asked about pharma’s ability to perform specific activities, as many as 80% of 2015’s respondent patient groups with an interest in heart-and-circulatory conditions stated that the industry was “Excellent” or “Good” at making high-quality, useful products. The equivalent figure from heart-and-circulatory patient groups in 2014 was 57%. Patient groups with an interest in heart-and-circulatory conditions ranked Pfizer overall 1st out of 15 pharma companies for corporate reputation in 2015 (for a second year in a row). They also ranked Pfizer first for two of the six indicators of corporate reputation: patient safety, and the ability to create high-quality products. Regarding the other four indicators of corporate reputation: AbbVie ranked 1st for patient centricity (the company was not included in 2014’s analyses); Novartis ranked 1st for the provision of patient information; and Sanofi ranked 1st for both transparency and integrity. The PCRI data for the heart-and-circulatory league tables in 2015 and 2014, and for patient groups from across all therapy areas in 2015, show that Sanofi, Novartis, AstraZeneca, Lilly, and GSK all improved their corporate reputation among heart-and-circulatory patient groups between those two years. The biggest leap was made by Sanofi, which went from 7th out of 11 companies in 2014 to 3rd out of 15 companies in 2015.

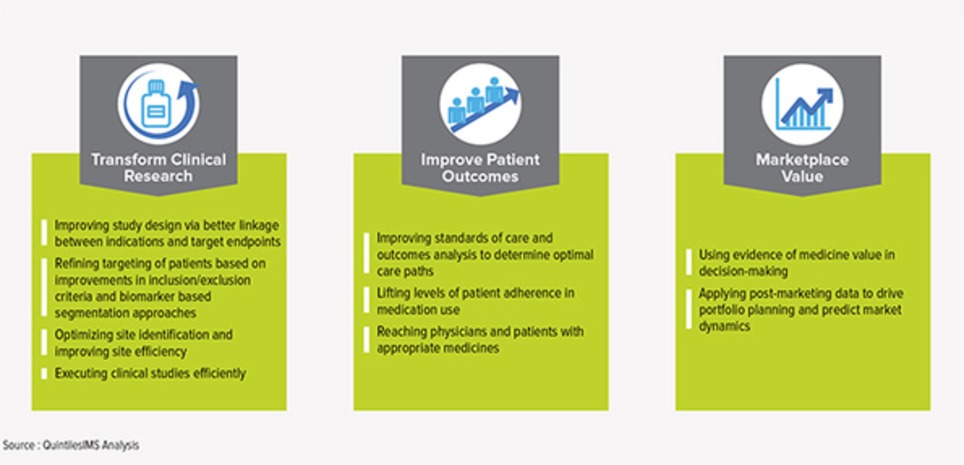

Discover what matters to health care consumers and what it means for health care providers. Gaining an understanding of what drives the choice-making for health care consumers is complex. The journey is complicated and multi-tiered, and differs greatly from the consumer experience in other industries. But as the health care industry continues to shift from volume to value, and as consumers take a more active role in managing their health care, the need to understand what matters most to them grows.

In Deloitte’s 2016 Consumer Priorities in Health Care Survey, we explored a number of interactions consumers face throughout their health care experiences. Their expectations in these health care interactions are being shaped by the customized and convenient experiences they have grown accustomed to in other industries, like retail and banking.

As a result, they are demanding greater personalization; transparency in network coverage, medical prices, and bills; convenience; and more engaging digital experiences and capabilities. From doctor’s appointments to lab visits and even hospitalizations, consumers seek high quality service tailored to their specific needs from health care providers and administrative staff.

As technology advances in other areas, consumers expect the same of health care. If they can book a flight from their mobile device, why not a doctor’s appointment? Increased convenience could be facilitated at the point of patients’ self-research, scheduling, intake, and the discussion and scheduling of follow-on treatment needs. While this process remains largely manual today, despite significant investment in health IT, expanding the digital connection to providers could enhance convenience and personalization for the health care consumer.

The engaged health care consumer is proactive about their care management and cost considerations, and takes the time to understand larger aspects of the health care ecosystem that pertain to them. Therefore, consumers are increasingly expecting more out of the services they receive from their providers.

In response, players across the health care ecosystem are developing strategies to better meet the demands of the engaged consumer. Providers are working more collaboratively with health plans, technology companies, pharmacies, retailers, and device makers to streamline processes. While digital tools are not yet the highest priority or concern of health care consumers, as evidenced in recent Deloitte studies, their usage will be vital to the future of consumerism.

Survey findings revealed a series of top-tier priorities expressed by consumers with regards to their providers:

Consumers want to be known and understood in order to get a personalized health care experience; providers are in the best position to deliver it.

According to Deloitte’s Survey of US Health Care Consumers, 75 percent of consumers seek a partnership with their providers to determine the most effective treatment decisions. And one in three consumers wants their provider to push them to be more active in researching and questioning their prescribed treatments.

We found that the number one preferred interaction is having a doctor or other health care provider spend sufficient time with the patient and not rushing through exams.

Relationships with providers can be complex, often emotionally charged, and become increasingly crucial over time as older patients often find themselves with increased face-to-face care and support needs. The most attuned providers can steer consumers effectively by focusing on the element of human touch.

Download the survey to read in detail the health care interactions that stood out in each of the four thematic clusters.

rob halkes's insight:

Good to see that patients know best about their own demands:

The first is trust and dedicating enough time to the right decisions for the patient personally. Although digital support is valued, the basic principle is empathy and attention.

NICE, regulator and NHS should work together, according to review.

October 24, 2016

The government has published its long-awaited Accelerated Access Review, a report that aims to cut up to four years from the process that gets a drug from the lab to use on England’s National Health Service.

Commissioned by the government and led by an independent chair, Sir Hugh Taylor, the review covers diagnostic tools, drugs, digital healthcare and medical technologies.

Originally due to be published earlier this year, the Accelerated Access Review is the brainchild of former life sciences minister George Freeman, but was delayed because of the EU referendum.

Developed in partnership with the Wellcome Trust, the review aims to speed up and simplify the process for getting promising new treatments and diagnostics from pre-clinical development to patients.

The scheme will join up clinical development, regulation and assessment of cost-effectiveness.

This will be through a new partnership including NHS England, NHS Improvement, NICE and the regulator, the Medicines and Healthcare Products Regulatory Agency (MHRA).

Patient access to drugs could be brought forward by up to four years if a scientific opinion from the Early Access to Medicines Scheme is used, saving 12-18 months, there is no delay at the NICE appraisal stage, which takes two years, or during the process for NHS commissioning and adoption, which takes two years or more.

There will be a simpler process for regulating digital technologies, often developed by smaller companies, such as healthcare apps for managing long-term solutions.

A new Strategic Commercial Unit should be created within NHS England, the report said, to create “win-win” scenarios where innovators benefit through early access to the NHS market and increased, perhaps guaranteed sales. Innovators would offer better value to the taxpayer.

Patients will also have a greater say in determining what innovations to prioritise.

Other proposals include:

Improved horizon scanning for innovative new products, and a systematic approach to prioritising the best innovations coming down the pipeline,

A national ‘Accelerated Access Pathway’ for the most transformative products, where the system works together to bring these exciting innovations to patients more quickly, including for digital products which are often developed by SMEs,

More streamlined local routes to market for all innovators, making the whole system clearer and simpler

Stronger commercial capabilities within the NHS so that it can have the right conversations with innovators and secure the best deals for patients,

An ‘Accelerated Access Partnership’, bringing together the key national health bodies in a collaboration focused on bringing forward innovation,

Better data on the impact of technologies on patient outcomes and more easily accessible data on the uptake of innovative technologies,

Local support for the spread of innovation, through Academic Health Science Networks,

Stronger incentives for local NHS organisations to use and spread the benefits of innovation.

rob halkes's insight:

Accelerated Access to new drugs in the UK. Will the NHS succeed in its intentions to reduce time and speed up and simplify the process for getting promising new treatments and diagnostics from pre-clinical development to patients. New organizational structures (partnership) between NHS, NICE and others in regulation, as well as as "new strategic commercial unit should should be created (among other things to do the trick of reducing the normal time to healthcare of new drugs by 4 (!) years.

I just cannot help being a little skeptic having seen publications and information about the bureaucracy of NHS, messages about failing finances of the NHS (Brexit related) as well as my own experiences in getting several authorities to work together in such undertakings.

There is more to it then just a review.. But I wish them all good luck and best of success! (May a sincere co-creative process might help here)

This report explores how connecting disparate streams of data can create valuable insights that can make the difference in today’s biopharmaceutical marketplace. While these opportunities for connections exist across all disease and therapeutic areas, they may be most acutely needed in the complex and dynamic area of oncology. This report makes the case for the process by which a looming crisis in oncology can be averted, by applying the science—and art—of connecting healthcare insights.

rob halkes's insight:

"Data" might be the "disruptive" driver to create collaboration and partnership between sets of stakeholders to develop care to integrated and co-created care paths. Let's hope that. Is will be complex enough, but with that needed and not to be avoided!

The diversified company is collaborating with Texas Medical Center, the largest medical center in the world, to launch a medical device incubator where internal research projects as well as those working with outside entrepreneurs.

Johnson & Johnson is teaming up with the Texas Medical Center to accelerate the development of medical devices drawing from Houston’s deep engineering reserve and its large and diverse patient base.

That announcement was made at the annual conference of AdvaMed, the largest medtech lobby, in Minneapolis on Tuesday. Cardiac surgeon and serial medtech entrepreneur William Cohn will lead the Center for Device Innovation at Texas Medical Center. Cohn will not only focus on J&J internal research projects but also work with external entrepreneurs who will occupy space at CDI – the way young companies take up space at CDO.

Innovators at CDI will have access to the preclinical facilities of Baylor College of Medicine, Houston Methodist Research Institute, and the Texas Heart Institute. Be it internal J&J projects or external innovations, the center will allow for rapid prototyping and “fast failure” for early and mid-stage device development.

Texas Medical Center comprises 57 institutions with more than 110,000 employees and 60,000 medical residents, and gets more than 10 million patient visits per year, Cohn noted.

Engineers from other J&J sites will rotate through the incubator, which will house as many as eight projects at a time, added Bruce Rosengard, chief medical science and technology officer for J&J’s medtech companies. The company also plans to leverage the engineering resources at Baylor and NASA and will take advantage of the medical center’s large number of patients for clinical trials.

“We’re really going to roll it out and build it sequentially over a period of a couple of years to maximum capacity,” Rosengard said.

The incubator initiative is the expansion of a partnership for J&J and Texas Medical Center given that J&J opened one of its JLABS incubators there earlier this year. Similar such JLABS in San Diego, Toronto, South San Francisco, and Cambridge, Massachusetts.

CDI will focus on five areas where there’s globally significant unmet need for medical devices, said Gary Pruden, worldwide chairman of medical devices for the company. Those are — cardiology, obesity, oncology, osteoporosis, and osteoarthritis.

“By offering a range of different models for companies in different stages, to allow us to rotate certain projects to Houston that we think that environment can uniquely accelerate, that’s attractive,” Pruden said.

J&J will align those projects strategically, according to Rosengard.

“We think the special sauce here will be to provide end-to-end rapid development from concept to commercialization,” he said.

rob halkes's insight:

Like we ascertained in our research for EyeforPharma, (2015, also in 2013) the innovating pharma industry like J&J is seriously advancing in creating services to innovate healthcare beyond the therapy, "beyond the pill" also. The hype around "Patient Centricity" seems to have overflown this promising but difficult development. "beyoind the Pill" strategies go beyond "Patient Centricity," of which the pharma community is not yet able to define it. A strategic discussion might be in place for a company to look at how the business model might be developed according to demands from different regions in the global market and and innovative developments in health care itself. And so, exploring how working "beyond the pill" might be of the best of interests of patients, like they themselves would see this.

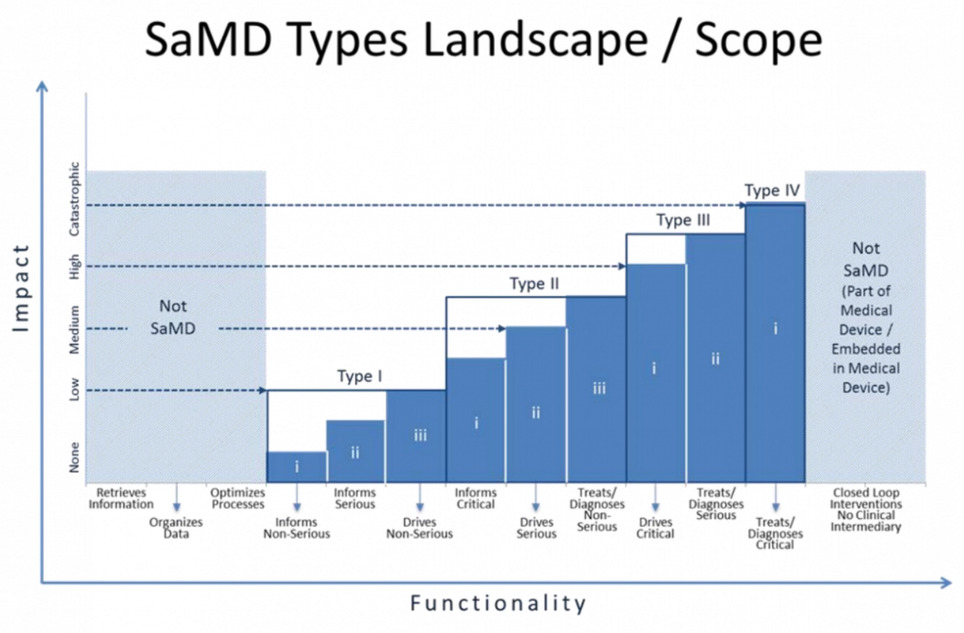

The FDA has entered into the federal register a new draft guidance pertaining to "software as a medical device" (SaMD). The guidance is presented as representing the FDA's current thinking on establishing clinical evaluation guidelines for SaMD, but is written by an international organization of device regulators, the International Medical Device Regulators Forum, of which FDA is a member.

The guidance seeks to articulate what's new and different about SaMD (a category which would include mobile medical apps) and provide a stratified guidance on how to regulate different kinds of software and what kind of evidence is needed for each regulatory category. The guidance stratifies devices on two axes: whether the device informs care, drives care, or treats/diagnoses and whether the condition in question is non-serious, serious, or critical. So software that treats or diagnoses a critical condition is in the highest risk category, while software that informs care about a non-serious condition is in the lowest.

The guidelines also call out and address the fact that software development tends to move faster than traditional medical device development and can more easily be influenced by postmarket data.

"SaMD ... is unique in that it operates in a complex highly connected-interactive socio-technical environment in which frequent changes and modifications can be implemented more quickly and efficiently," the guidance says. "Development of SaMD is also heavily influenced by new entrants unfamiliar with medical device regulations and terminology developing a broad spectrum of applications."

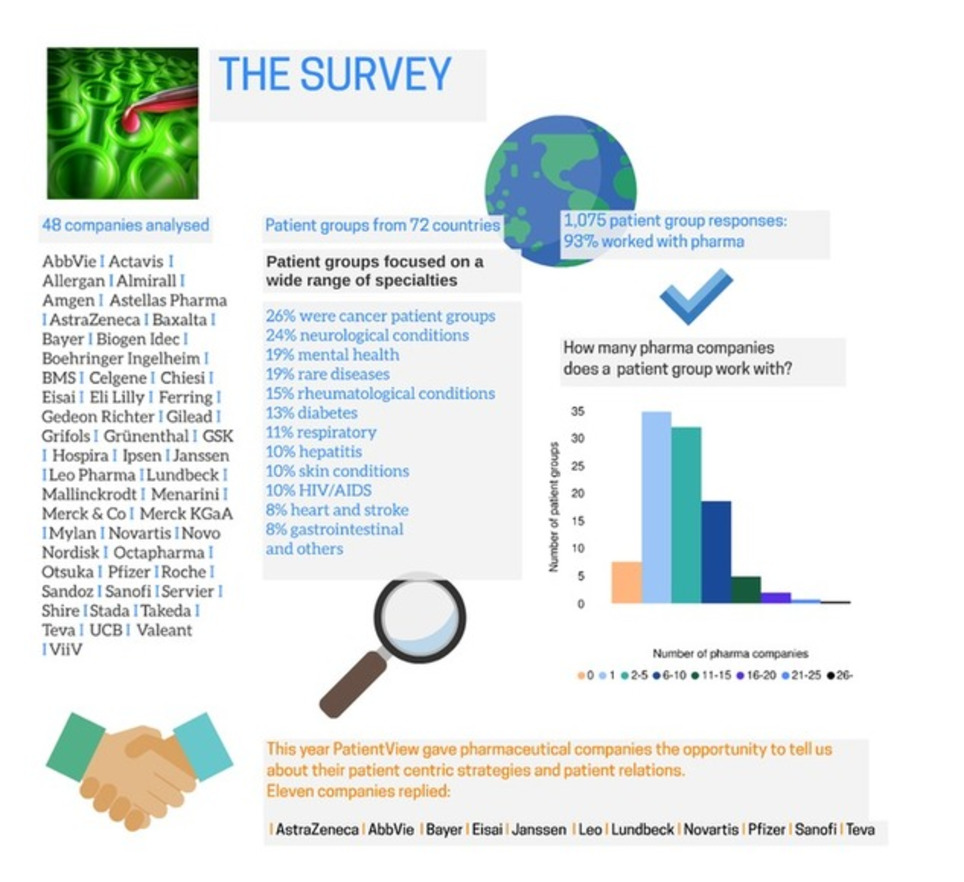

Reports published in 2016 on the Corporate Reputation of Pharma, as viewed by over 1,000 patient groups

The corporate Reputation of Pharma is growing: In 2011 there was 42.0% of patient groups stating that the corporate reputation of the Pharma industry is "excellent" or "good". Although this percentage decreased to a 34% in 2012, it has increased ever since to 44.7% in 2015!

For a quick summary about our methodology and series of reports on corporate reputation of pharma and medical devices view the powerpoint here

Of course, this global indicators must be seen from the differentiated perspectives of regions and diseases!

Reports of Pharma's Corporate Reputation over regions:

Great to seen how pharma's Corporate Reputation in the eyes of the patients is growing globally from 2011 to 2015, with a dip in 2012. Study the nuances for different global regions and Disease conditions!

Related article: “Pharma's Rep Among Patient Groups at 4-Year High”; http://sco.lt/6eoNgf It should be noted that several of the patient organizations participating in this survey receive funding from the pharmaceutical industry. Also read, “#Pharma to Patient Advocacy Groups Questioning High Drug Prices: ‘Why Are You Doing This to Us?’”; http://sco.lt/4sOB7J and “Americans Hate the #Pharma Industry Almost as Much as They Hate U.S. Gov't!”; http://sco.lt/7K6aLB

Survey results demonstrate the need for scientific information about cancer to be understandable to patients

Findings are based on a May 2016 survey of 124 cancer-oriented patient and carer organizations in 39 countries, conducted by PatientView, and sponsored by AstraZeneca.

99% of respondent patient/carer organisations report that people living with cancer want to know how their cancer treatments work.

Over 90% of patient/carer organizations report that patients must understand scientific concepts about cancer if they are to better manage their cancer.

LONDON, Friday, 7th October 2016

New survey findings indicate a significant need for scientific information that is accessible to, and understood by, people living with (and affected by) cancer. The majority of patient/carer organizations responding to the survey recognize that cancer science is complex and fast changing. As cancer science improves, and new discoveries occur, people who are living with cancer wish to learn more about the science of their cancer diagnosis and treatments. Nearly all (99%) of the patient/carer organizations surveyed “Agree” or “Somewhat agree” that patients want to know how their treatments work, and 91% of the respondent patient/carer organisations say that patients need to understand relevant scientific concepts about cancer to better manage their cancer.

The patient/carer organizations responding to the survey, however, also say that cancer science is hard to navigate for newly-diagnosed and experienced patients alike, and that currently- available patient information about cancer is difficult to understand, and confusing to people who are living with cancer [60% of respondent patient/carer organizations believe that cancer science is not well explained to patients and the public.

“An exciting new wave of cancer treatments is emerging out of the rapidly-advancing scientific concepts about cancer,” says Alex Wyke, founder and CEO of PatientView. “Yet, in the face of the advance, cancer patient information remains stubbornly hard for ordinary people to digest. The results from this 2016 survey show that over 90% of respondent patient/carer organisations believe that people living with cancer (and their families and carers) will be better equipped to manage the disease if they have a fundamental understanding of basic cancer science. Arming the cancer patient community with intelligible knowledge about cancer will allow people with cancer to understand more about the disease and its numerous diagnostic procedures and treatments. Such knowledge will empower people with cancer to communicate more effectively with doctors, nurses, and all the other health professionals who help them to fight cancer. In short, information about cancer science—carefully tailored to the needs of patients—will ultimately permit people with cancer to make truly informed decisions about their health.”

Key findings from the survey include:

99% of respondent patient/carer organizations “Agree” or “Somewhat agree” that people living with cancer want to know how their cancer treatments work.

Over 90% of respondent patient/carer organizations “Agree” or “Somewhat agree” that patients must understand scientific concepts about cancer if they are to better manage their cancer.

57% of respondents indicate that increasing the awareness of cancer treatment options among patients and the public is a top priority of their organization.

61% of respondents say that the public is unfamiliar with basic scientific concepts about cancer.

83% of patient/carer organizations have been asked by patients/carers about immuno- oncology. However, only 48.2 % of those same organizations are themselves familiar with the topic of immuno-therapies in oncology.

67% of patient/carer organizations have been asked by patients/carers about gene mutations associated with cancer and biomarkers. Again, though, only 52 % of the organizations themselves claim familiarity with the concepts of genetic testing and precision medicine.

ABOUT THE SURVEY SPONSOR This 2016 survey of 124 patient and carer organizations was sponsored by AstraZeneca, a global, science-led, bio-pharmaceutical company that focuses on the discovery, development and commercialization of prescription medicines—primarily for the treatment of diseases in three therapy areas (respiratory/autoimmunity; cardiovascular/metabolic diseases; and oncology).

ABOUT THE ORGANIZATION THAT CONDUCTED THE SURVEY PatientView was founded in 2000 out of a belief that the views of patients should be considered in every important healthcare decision (whether a new healthcare product or service, or a government change to a healthcare system). A UK-based research, publishing and consultancy group, PatientView has the capacity to reach out to 120,000 patient groups worldwide, covering over 1,000 medical specialties.

PatientView Ltd, One Fleet Place, London EC4M 7WS, UK +44 (0)1547 520 965 info@patient-view.com www.patient-view.com

Media contact

Alex Wyke, CEO, PatientView +44 (0)1547 520 965 alexwyke@patient-view.com]

rob halkes's insight:

Grt example of how big pharma supports healthcare provision, by generating significant patient needs!

The more cooperation between patient groups and health industry, the more the really relevant and significant information can be researched to better health outcomes!

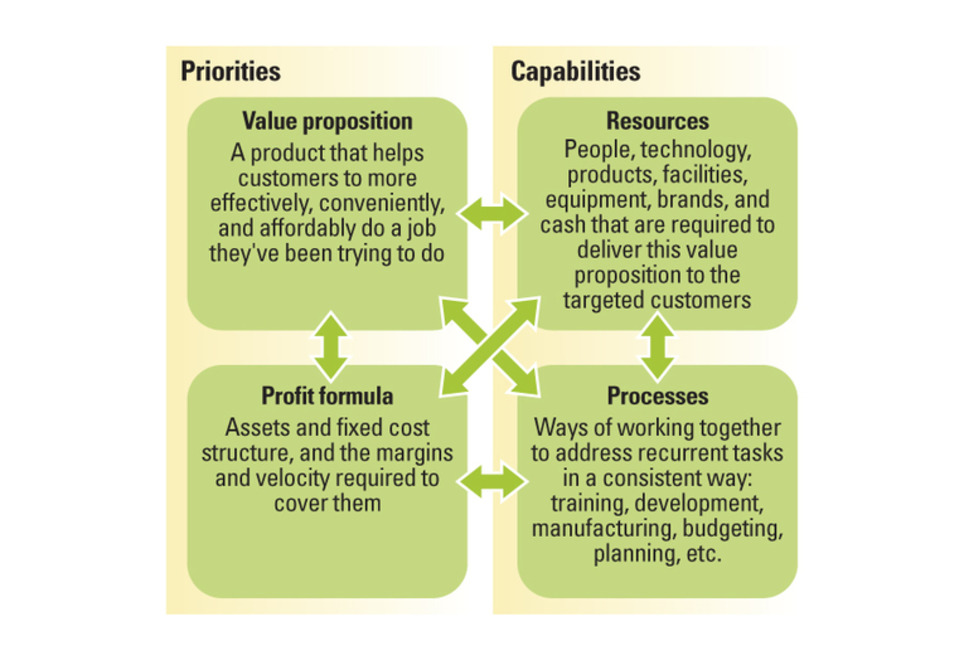

Successful business model innovation requires an understanding of how business models evolve.

Many attempts at business model innovation fail. To change that, executives need to understand how business models develop through predictable stages over time — and then apply that understanding to key decisions about new business models.

Understanding the interdependencies in a business model is important because those interdependencies grow and harden across time, creating another fundamental truth that is critical for leaders to understand: Business models by their very nature are designed not to change, and they become less flexible and more resistant to change as they develop over time. Leaders of the world’s best businesses should take special note, because the better your business model performs at its assigned task, the more interdependent and less capable of change it likely is. The strengthening of these interdependencies is not an intentional act by managers; rather, it comes from the emergence of processes that arise as the natural, collective response to recurrent activities. The longer a business unit exists, the more often it will confront similar problems and the more ingrained its approaches to solving those problems will become. We often refer to these ingrained approaches as a business’s “culture.”

rob halkes's insight:

Great article about business model innovation. I was struck by the resemblances of errors made at introducing new value added services to pharmaceuticals, "beyond the pill". The same may possibly be expected by the new "hype" (?) about patient centricity: in my mind doing things without reflection about what it is: ending up in webinars/conferences existing mainly of either pharma staff in which they share their ignorance, or even in pharma staff added with a patient or patient representative, in which the patient is commonly canonized (as in 'sainted'): understandable but not a functional way of developing new trends in a company, let alone a new trend in a business sector..

See here what patients really have to say about corporate pharma companies and its patient "centricity": PatientView.com

EphMRA develops and improves standards and techniques for market research in Europe in the field of health and healthcare. EphMRA offers training and conferences for healthcare professionals.

We are now inviting ideas for papers for the conference next year, 2017, and welcomes your submissions on a whole range of different topics. Below are some ideas for topics to get you started but we would be keen to hear from you if you have other ideas which you think will educate, inform and inspire colleagues working in our industry:

Innovative approaches

How to increase the value of MR / BI

Patient Insights

Multi-disciplinary teams

Analysis / Secondary data

Data Collection

Ideas for debates involving panels / audience participation

Please read more here about the Call for Contributors pdf which has all the information you need to make your submission. You will need to use the submission form - click here and we need your submissions by Monday 19 September so that the Programme Committee can review them all in October.

All sessions will be 30 minutes in duration (25 minutes for presentation + 5 minutes for Q&A).

We look forward to hearing from you soon with your ideas.

rob halkes's insight:

EphMRA, the European Pharmaceutical Market Research Association, is not only reflecting on the basics of its existence, but, in so doing, they are now embarking on a wider perspective on research in healthcare and healthcare markets (see here www.ephmra.org/EphMRA-Statutes ).

This is reflected in its conference themes of 2017 for which the organization is now calling for papers. Great to see there the topics of "innovative approaches" and "Patient Insights"! To orientate yourself, see for instance the "pharma corporate reputation review" by Patientview!

Based on EvaluatePharma’s coverage of the world’s leading

5,000 pharmaceutical and biotech companies, the World Preview highlights trends in prescription drug sales, patent risk, R&D spend, global brand sales and market performance by therapy area.

If there was any doubt that the pharmaceutical industry is entering a period of sustained growth it should be put to rest by this year’s World Preview 2015 showing prescription drug sales are set to advance at almost 5% a year until 2020.

Continued confidence in the sector is being driven by a number of positive fundamentals including the recent increase in R&D productivity, which has resulted in a big hike in drug approvals, and the emergence of breakout drugs such as Gilead’s Sovaldi franchise. Excitement surrounding new products including Merck & Co’s Keytruda, Bristol-Myers Squibb’s Opdivo and anti-PCSK9s from Amgen and Sanofi should ensure the sales momentum continues.

The current industry feel-good factor has also been mirrored in the amount of money businesses are raising, the number of pharma and biotech companies floating on exchanges around the world, and the healthy appetite for M&A seen across the board.

While some things are changing in the industry, others remain the same. A strong focus on oncology has helped Novartis retain its crown as the number one pharma company in terms of prescription sales. More interesting, however, has been the rise of ‘big biotech’ and specialty pharma into the ranks of the industry’s big players.

Despite setbacks from some approved and clinical biological drugs depressing the speed of change, the global sales contribution from biologic drugs is forecast to jump from 23% in 2014 to 27% in 2020.

These drugs have traditionally enjoyed greater patent protection than their small molecule relatives,but the landscape is changing with the approval this year of the first US biosimilar

Future outlook

Standing at the midpoint of 2015, the pharma and biotech industry looks as if it is in very good shape, the patent cliff is firmly in the rear view mirror, and while it might be too early to call on sustained R&D productivity, things are at least moving in the right direction. The only clouds currently on what looks to be a sunny horizon for pharma and biotech are global pricing

and market access. With many predicting that for the first time the industry could produce a series of real ‘cures’ for previously intractable diseases, it is clear that these innovative drugs will come at a price. What is also clear is the growing reluctance of both government and private healthcare providers to fund very expensive drug treatment regimens

Complimentary copies of the full report can be downloaded at:

Looks like the pharma business awaits a fruitful future. However dark clouds are emerging at the pharma skies too. Challenges to business and commercial approaches might not only concentrate on pricing, but certainly, with a rising trend in a demand for increasing health outcomes of medication, on the right applications and adherence too. Partnership with healthcare providers that goes beyond 'just' delivering drugs seems to become crucial.

Big, multihospital health care systems increasingly dominate the US market, and they are reshaping where and how vendor selection is made. Many medical-technology companies are not fully prepared for the changes taking place in purchasing dynamics. Companies that develop a top-quality KAM function will build a powerful advantage.

In this article:

US hospitals continue to consolidate, concentrating the power of big health systems over purchasing decisions.

Selling successfully to these organizations requires a deep understanding of their strategy, stakeholders, and decision-making processes.

The challenge is building an account team with requisite in-depth customer knowledge, which requires a key account management approach and an exceptional degree of coordination across a vendor’s selling resources.

A New KAM Model: From Sales Transactions to Strategic Partnerships

Main take aways:

- Centralization of purchasing is on the rise, but the structures and processes vary. The shift of purchasing authority for medtech products from clinical to economic decision-makers is well recognized. Less well understood are the structure and hierarchy in which purchasing decisions are made at each large system and the often complex role of national, regional, and local value-analysis committees. - Health system value-analysis committees rank clinical value over clinical preference. Value analysis—measuring the benefits of a device relative to its cost—has resulted in more informed and more economically sophisticated decision-making in large systems. Physicians are increasingly “picking their battles” instead of fighting hard for every clinical preference

- Develop customer-specific account plans that are built upon deep customer understanding. Best-in-class account plans reflect a deep understanding of a customer’s business strategy and objectives—and extensive knowledge of the customer’s purchasing process and key decision makers.

The challenge for medtech account teams is determining where the purchasing authority resides in each system’s structure and understanding what factors those decision makers care most about. Good account plans use this understanding, as well as a detailed analysis of the customer’s market position, market share, and growth prospects, to help articulate a clear sales strategy and how that strategy will help the customer achieve its objectives. Periodic reviews, especially after a significant customer event such as a merger, acquisition, or senior-management change, help keep the sales strategy fresh and relevant.

- Develop clear economic and clinical value propositions for core products. Medtech suppliers need to demonstrate the value that their products can deliver beyond price and clinical efficacy. Potential proof points are improving outcomes, increasing workflow efficiency, requiring fewer staff, reducing infections, adding new profitable patients, reducing readmissions, and many more. - Adopt a consistent and defensible national pricing and contracting strategy.

- Implement a sales coverage model that defines clear roles for key account managers and sales reps in the field. The most progressive medtech companies are beginning to vary their sales coverage on the basis of customer characteristics.

-Build a KAM team that possesses a new set of skills

- Provide the team with management tools that support efficient decision-making and cross-functional sales execution.

rob halkes's insight:

BCG has found out about the same as I did already since 2007: Key Account management demands crossfunctional teams, "build on the basis of customer characteristics", not only according to quantitative parameters but also on qualitative characteristics, I would add! See a summary of my experience here.

Do have me explain to you what experience tells about how to set this up!

FDA said it will ease up vetting general health and wellness apps, but it will scrutinize clinical applications and devices. Does this mean the FTC will step up?

The U.S. Food and Drug Administration has issued final guidance on “low-risk” digital health apps and devices for general health management 18 months after it came out with draft guidance.

The document offers information on the kinds of apps and devices for which it will and won’t take action. Apps promoting or maintaining a healthy weight or to assist with weight loss goals and healthy eating are OK. The guidance says that companies can make claims that their apps and devices can help with healthy lifestyle choices to reduce the risk of chronic conditions such as Type 2 diabetes, high blood pressure and heart disease or improve their management. But those lifestyle choices have to be advocated by the likes of the American Heart Association or American Association of Clinical Endocrinologist or peer-reviewed medical journals.

So what are some examples of what’s not OK? Claims that a product will treat or diagnose obesity, an eating disorder, such as bullimia or anorexia, or an anxiety disorder. Digital health entrepreneurs are also encouraged to ask themselves the following questions:

Is the product invasive? Is the product implanted? Does the product involve an intervention or technology that may pose a risk to the safety of users and other persons if specific regulatory controls are not applied, such as risks from lasers or radiation exposure?

If the answer is yes to any of the above, they need to assume their products are considered clinical applications, will be scrutinized and should act accordingly.

My takeaway from the guidance is twofold. It’s a question of resources. Although there are thousands of general wellness apps, more and more medical device and pharma companies are developing digital health devices and apps of their own. Second, the Federal Trade Commission has shown it is willing to take action against companies that it deems to be making false health claims about their apps and devices.

rob halkes's insight:

Health apps should do what they promise! At the moment they need to take a diagnostic feature and use personal physics to arrive at advice or conclusions about the health status of the person who uses the app, they are considered not to be 'just' an "app" but a medical device. At that condition they need to adhere to and be certified by several criteria attached to 'medical devices". Developers should know about this, which the more professional ones will. Rightly so!

PatientView has developed a website MyHealthApps that presents an inventory of the better Health Apps.

The first half of 2015 continued to confound the naysayers of the pharma industry, with deal making, venture funding and share price indices all showing no signs of slowing down, according to EP Vantage's Pharma & Biotech Half-Year Review 2015.

Key highlights

The year started with one of the biggest venture rounds ever with the $450 million Moderna Therapeutics managed to secure from its investors in January

VCs gifted $3.8 billion to companies at the half-year point signifying that 2015 could once again raise the bar in terms of funding totals

On average, the 32 floats in 2015 yielded only a three percent discount from the listed range, and increased in value by 23 percent since their IPOs

See download the report

rob halkes's insight:

If pharma approaches the business wisely and with willingness and capacity to innovate, then there is a lot still to be done and gained.

The market for digital dose inhalers for asthma and COPD will be worth $3.56 billion in 2024, according to a new prediction from Grand View Research.

Though connected inhalers are a new market, they've seen rapid growth in the last few years with interest from big pharma companies like AstraZeneca and Novartis, major device companies like Philips Respironics, as well as the newer, smaller players like Propeller Health that have made a big bet on the space.

Grand View sees that growth continuing into the next several years, citing an aging population and a surge in the prevalence of chronic respiratory disease as two drivers. They also foresee rapid growth for markets outside North America. The firm predicts the Asia Pacific region will grow at a 17 percent compound annual growth rate (CAGR) between now and 2024.

"As a result of impactful economic developments in the fast emerging countries, such as China, India, Brazil, Philippines, and others, there has been growth in the per capita income, which is thus expected to influence the demand for the technologically advanced respiratory devices," the firm writes in a press release. "Moreover, these technology-enabled respiratory devices are greatly sought after among the pediatric and the geriatric population so as to improve the patient medication compliance, dose tracking, and to enhance patient-healthcare practitioner connectivity that would enable real-time tracking of healthcare data; these serve as high impact rendering factors, significantly driving the market growth in the next nine years. [...]

The report names some major players in the space which include a number of companies MobiHealthNews has written about over the years, including Teva Pharmaceuticals, which bought into the space with its acquisition of Gecko Health; Opko Health, which acquired Inspiro Medical; AstraZeneca, a major investor in Australian smart inhaler company Adherium; and Propeller Health, which makes inhaler sensors for a growing number of pharma and provider partners including GSK and Boehringer Ingelheim. They also name Philips Respironics, Novartis, and Glenmark Pharmaceuticals. Glenmark launched a digital dose inhaler, which tracks usages digitally and alerts the user when it's close to empty, in May. Novartis announced in January that it would work with Qualcomm Life on a connected inhaler for COPD.

Smart inhalers might as well be the leverage of pharma to really consider and develop partnerships to healthcare. Delivering inhalers should be more about developing co-creative collaboration and taking responsibility of health therapies in action. Curious how this development will change the pharma/health market! See the customer centric pharma business model as well!

How early in the development of a new medicine should thEarly collaboration - a recipe for solutions: drug development and treatment strategies may go hand in hand.e discussion between researchers and patients occur? Can such early strategic interaction really maximize the value of the outcome? In this EUPATI webinar, a pharmaceutical industry researcher and a patient expert will present two cases describing the research questions, their interaction and the outcome of this early collaboration. Join us in listening and discussing two very interesting experiences of successful patient involvement in the development of new medicines.

rob halkes's insight:

Grt review and discussion of the actual active participation of patients in medical research, medicine testing in phases II, III.

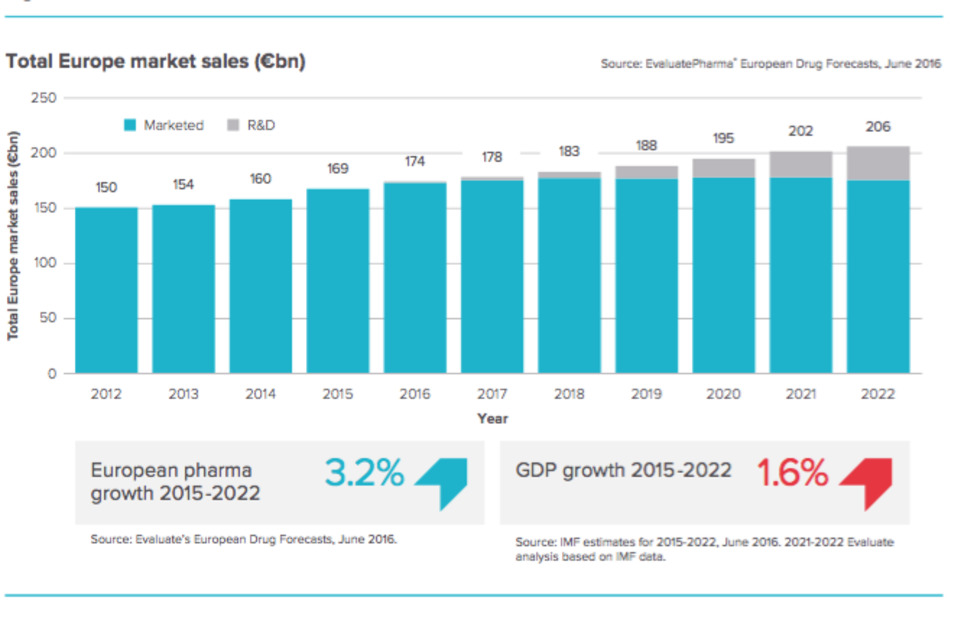

Pharmaceutical Innovation in Europe New pharmaceutical breakthroughs approaching – is the system set up to fund them all?

This report shows that the advent of new potential blockbusters in Europe is expected to position the European pharma industry with increased growth through to 2022 of 3.2% CAGR (2015-2022).

Are healthcare systems and payers ready for innovation?

The pharmaceutical industry has been going through a period of radical transformation of its business model which, coupled with scientic advances, is now resulting in a new wave of innovative treatment options that are anticipated to put additional pressure on the nancial resources of already cash-strapped healthcare systems.

If in the past the balance was primarily achieved via price-cutting policies either supported by the introduction of cheaper generic or biosimilar versions, forced rebates at national level or the application of international reference pricing rules, such a trend is no longer sustainable. It is probably time for payers and the pharmaceutical industry to work together at the same table and devise new and more e cient funding methods as opposed to the often theoretical risk-sharing and pay-for-performance schemes that have been trialled so far.

Report Author:

Antonio Iervolino – Head of Forecasting Antonio.Iervolino@evaluategroup.com

We're getting near the end of the lifetime of the traditional business model of the pharma industry. Blockbuster get scarce and personalized medicine will limit Rx of innovative drugs to smaller groups of patients.

Besides these, commercial challenges are high to traditional companies: information of physicians is not only limited by engagement ruling and closing doors to reps, but it also demands now complicated data based engagement models to create customized journeys of information for target groups via multiple and new channels.

These challenges go together with highly impacting changes of

refocusing to newly targeted customers, by quantitative and qualitative parameters;

new patterns of cooperation between departments within focused account teams;

alignment to the (key) customers' level of health care development into patient's pathways, as key criterion for customer relations development;

collaboration with patient (groups) to help co-create innovation in healthcare;

and servicing customers and patients with added value to better care with lower costs.

Although this seems hardly feasible to do for a centralized pharma company, there are indeed ways to do so, as we experience it. See here for a general introduction:

Germany's Boehringer Ingelheim is to cut more than 700 jobs across its US operations, with the axe falling hardest on its sales functions.

The 724 redundancies include 49 at the company's US HQ in Danbury, Connecticut, but according to a filing with the Connecticut Department of Labor the remainder will mostly occur in sales.

The nature of pharma sales has been changing over the last decade or so, with many companies opting for less face-to-face interaction with physicians and other healthcare providers.

Patent cliffs have also hit big pharma hard, with several firms recently announcing major restructures in a bid to make savings and funnel money into R&D.

Boehringer said in a statement: “The actions we are taking now will help us reinvent the way we serve the needs of our patients, and enable us to continue to make significant investments.”

Boehringer has made a number of recent changes to its operation worldwide in a bid to make itself more competitive. Last year the company announced it was to leave the generics sector by making an asset swap (consumer health interests in return for an animal health business) with Sanofi and a $2.6bn deal with specialty firm Hikma.

From this month Boehringer's R&D operations are to be renamed the 'Innovation Unit', handling all stages of development up to clinical proof-of-concept. Its Prescription Medicines Business Unit will be responsible for the subsequent 'highly market-oriented development' of products.

The US pharma industry has been hard hit in the last year, and the company is not alone in making cutbacks. As part of a move to save $1.5 billion worldwide, AstraZeneca has already pledged to close a manufacturing plant in Westborough, Massachusetts. Other measures will involve shutting a site in Bristol, UK.

… and Arena also plans US and Swiss cuts Meanwhile Arena Pharmaceuticals is also slashing headcount at its workforce in the US by 35% - around 80 staff - in a bid to save $11m. Arena also said it was to make “reductions” at its Swiss manufacturing facility to create further savings.

Harry Hixson, Arena's interim CEO, said: “This initiative supports our strong desire to create a more streamlined and efficient organisation focused on key priorities designed to add both near- and long-term value to the organisation.”

rob halkes's insight:

The new pharma business model does certainly something to the REP! Multi-channel and Account management will overtake their place. However, innovating pharma sales, will not do the trick by just changing it to multi-channel. A new thought through approach needs to focus on accounts based on chances for success, adapt to the level of account relations and must add value that is specific to the customer's development of care. A challenge! Connect to be explained in depth: http://bit.ly/pharma_business

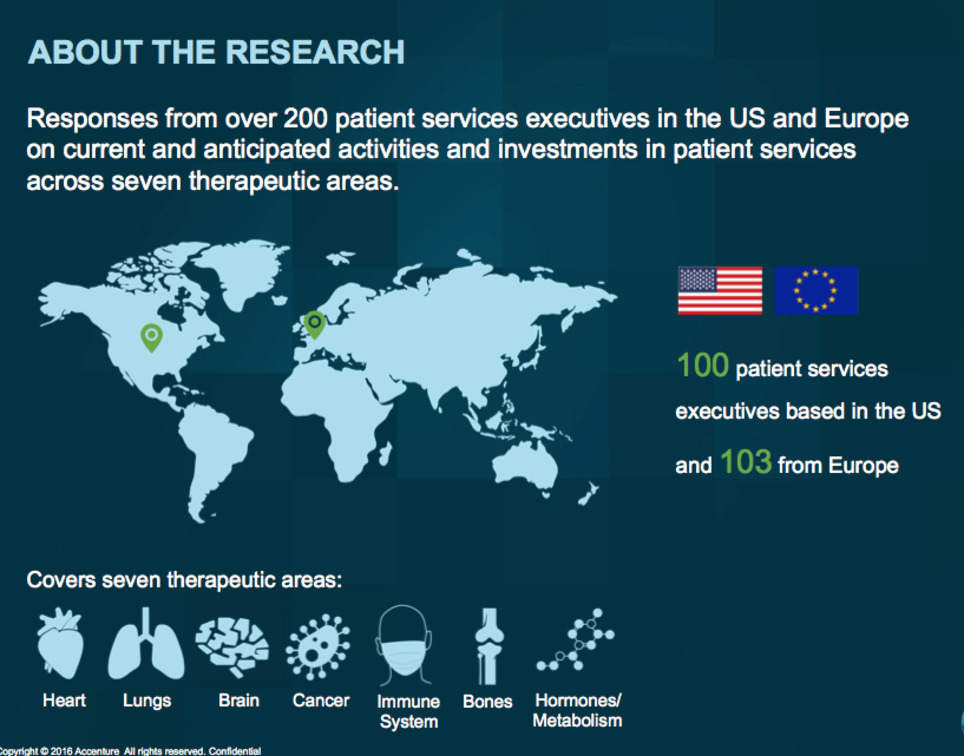

We surveyed 200+ patient services executives in the pharma industry to understand where their companies are in developing patient services

The future of patient services is bright.

Patient Services offˆers pharmaceutical companies a tremendous opportunity—for those willing to invest in the right places and let patients know about them in the right way. We surveyed 200+ patient services executives in the pharma industry to understand where their companies are in developing patient services and where they intend to go over the next two years and contrasts that with patients told us they want, value and expect from patient services.

Our survey covered seven therapeutic areas: heart, lungs, brain, immune systems, bones, hormone/metabolism, and cancer. And guess what? Our study revealed that the future of patient services is bright—for both pharmaceutical companies and patients.

KEY FINDINGS:

Patient Services are delivering value with a significant increase in focus and investment expected over the next two years.

Companies are going big with investments in digital engagement technologies and supporting analytics.

Much of this investment (but not all) is aligned to what patients value

POTENTIAL BENEFITS:

Companies primarily make patients aware of their services through healthcare professionals, however, less than 1 in 5 patients are aware of the services.

The majority of companies are not able to precisely measure the impact of patient services on outcomes.

Heads of patient services/experience are rapidly emerging but without full ownership of the patient experience.

This research report is intended to help pharmaceutical companies’ hone in on the services that present the highest potential—for them and the people who use their therapeutics—so they can take a leadership role in shaping this rapidly evolving market and prepare for the shift from delivering products to delivering better patient and health system outcomes.

rob halkes's insight:

Great insight from this research in what patients want and how pharma tries tof fulfill these needs. However, as this research shows too, only a less than optimal approach is chosen to disseminate and implement the services: a finding we already acknowledged in our own research of pharma's value added services. (See http://bit.ly/ValueAddedServices) The right approach to patient services is to create and disseminate them with them instead of to them. You need to align with patient groups to know what patients want in their region within their care. Next, you may align with both physicians and patient (groups) to create local applications in healthcare. See here for more information: http://wp.me/p4pqUp-Li

Measuring influence – how we used the Healthcare Social Graph® Score to determine PM Society’s Digital Awards winner The PM Society’s 2016 Digital Awards Winners!

The PM Society’s 2016 Digital Awards took place last month in London, and we were again asked to do the analysis and present the winner of the Social Media Pharma Company of the Year award.

In order for a company to have an effective social media presence it must know where the relevant conversations are taking place, the style of messaging that resonates among the participants, and most importantly who the influencers are within those networks of individuals. We used the Healthcare Social Graph® algorithm to determine weather a company was able to reach their audience from engaging key opinion leaders and their spheres of influence.

The five companies shortlisted for the award were AbbVie, Bayer, Boehringer, Novartis and Pfizer. [...]

But before we get to the winner, let’s walk through how we computed the data.

From the 606 million healthcare tweets collected during 2015 we analyzed the conversations around the top 10 diseases with the highest mortality rates in the U.K.; Breast Cancer, Lung Cancer, Prostate Cancer, Stroke, Dementia and Alzheimer’s Disease, COPD, Heart disease/failure, Lymphoma, Bowel Cancer and Pneumonia. Over 500 different hashtags were part of the dataset covering these 10 diseases.The pharma accounts with the highest influence and engagement were identified by the Healthcare Social Graph Score. [...]

Social Media Pharma Company of the Year is – Boehringer

It is our hope, that from the transparency on how this algorithm works, more companies will see the value in not only engaging stakeholders with traditionally strong voices, but including everyone in healthcare.

rob halkes's insight:

@Boehringer Ingelheim wins again the social media award for Pharma compnay of the Year! #pharma

It's the subject that just won't go away. Which medicines should Europe's health systems pay for – and how much should they pay?

No apologies for returning to the issue, because Europe's authorities have seized on it once again, putting drug pricing at the top of the bill at a meeting of Europe's health ministers in mid-April. Pharmaceutical executives never tire of the discussion either — because they know that if it goes the wrong way, they could be out of a job, and that in the current tough economic climate, nothing can be ruled out.

Even Sanofi's CEO Olivier Brandicourt, the strong man of France's drug industry, was ready to admit — on his home turf, at a meeting in Lyon, on the eve of the health ministers' meeting — that he was "not optimistic" that the industry was getting its message across. [...]

So there is fertile ground for the health ministers' discussions of pricing — clothed in the modest figleaf of "Innovations for the benefit of the patient", as a concession to the traditional member-state insistence on keeping these decisions at national level. And Dutch health minister Edith Schippers scattered plenty of seed in advance of the meeting, with a hard-hitting paper outlining the need for action.

"The current pharmaceutical system is out-of-balance", it says, and "It is time to set a new course." Explicitly and with no apology for its radical break with tradition, it says baldly: "We should take measures to better control the price of medicines."

The paper highlights the problems that governments face. "Member states deal on an individual basis with global pharmaceutical companies, in a context of great information asymmetry between governments and industry," it points out. "Companies benefit from fragmented procurement and budgeting of medicines in Europe," and patients, people who are insured, and taxpayers throughout the European Union "are the victims." So one of the main aims should be for cooperation that can increase information-sharing and transparency about products, markets and prices, and can make better use of joint health technology assessment for reimbursement decisions is also fruitful. "If member states work together more closely," says Schippers' paper, "the imbalance at the negotiation tables can be reduced."

The industry is the culprit, despite its often helpful innovations, the paper makes clear. "The profit-oriented industry does not make drugs pricing very transparent," and "this makes a sensible discussion regarding socially acceptable drugs prices much more difficult." Drug prices no longer take account of anything else, it suggests. "The relationship between innovation and a reasonable, socially acceptable price is absent." In addition, the industry's enthusiasm for maximizing profits leads it to make "undesirable use or even misuse" of protection mechanisms linked to intellectual property.

The result, the paper alleges, is that essential medicines - including orphan medicines and oncolytics - are not affordable or not even marketed in some countries, demonstrating how "commercial interests prevail over public interest." This, says the paper, can be considered as market failure. And it provides the justification for something akin to a declaration of war: "We should therefore aim at achieving a stronger negotiating position for the purchaser in order to compel that the price of a product better reflects its actual development cost and added value."

The mechanisms envisaged are not so clearly spelled out. But the paper before ministers speaks of European cooperation as "an important condition for a system of sustainable provision of medicines" and a way of taking a stance "to bring about the necessary changes in the market authorization framework, in regulations governing supplementary market protection in addition to patent law, and reimbursement."

This isn't going to be a straightforward confrontation between governments and industry, either. The background to the debate is the growing chorus of complaints and criticisms from patients and influential civil society organisations, to which governments — ever alert to the grass-roots, and ever sensitive to the need to placate the voluble — have been paying increasing heed. [...] Read further at the orginal article HERE

rob halkes's insight:

The theme of pricing new drugs will not go away. The pharma industry needs to make a clever and a responsible response to concerns of healthcare payers. Governments however too have to acknowledge that this is (in the end) not a power issue, of governement over industry or vice versa, rather a problem of colaboration between all stakeholders in care.

Patient groups in the US were more positive about pharma in 2015 than in previous years. Even so the approval ratings by US patient groups remain significantly below those given pharma by patient groups elsewhere in the world. Reports published in 2016 on the Corporate Reputation of Pharma, as viwed by over 1,000 patient groups

rob halkes's insight:

#Pharma reputation increased in 2015, but still uch to be done! Specifically in the US, patient groups rate pharma lower than elsewhere!

Learn about the drugs discovery breakthroughs in pharma industry in the past 12 months from all around the world.

Immunotherapy for Cancer Treatment

In an international trial conducted by various organizations, 945 patients with advanced Melanoma (a type of skin cancer) were treated using the drugs ipilimumab and nivolumab. The treatment was able to delay the advancement of the cancer cells for nearly a year in 58% of the cases, with tumors stable or shrinking for an average of 11.5 months, researchers found. (...)

Entresto (TM) for Cardiovascular Diseases

Novartis’ new FDA approved medicine Entresto reduces the strain on the failing heart, and is prescribed for reducing the risk of cardiovascular death and heart failure. It is usually administered in conjunction with other heart failure therapies, in place of an ACE inhibitor or other angiotensin receptor blocker. (...)

Amgen Inc.’s Repatha (Evolocumab) for High Cholesterol

Evolocumab belongs to a new therapeutic class known as PCSK9 inhibitors. These inhibitors limit the liver’s ability to remove bad cholesterol (LDL – low density lipoprotein) from the blood.(...)

Ibrance (Palbociclib) for Breast Cancer

Cancer cells grow in uncontrolled fashion. Ibrance (FDA approved) is a cyclin-dependent kinase 4/6 inhibitor. A kinase is a type of protein in the body that helps control cell division. Ibrance works by interfering with the kinase and stopping cancer cells from dividing and growing. Ibrance is specifically indicated for use in combination with letrozole for the treatment of postmenopausal women with advanced breast cancer as initial endocrine-based therapy for their metastatic disease. (...)

Rexulti (Brexpiprazole)for Schizophrenia

Co-developed by Otsuka and Lundbeck, Rexulti is now FDA approved for the adjunctive treatment of major depressive disorder and the treatment of schizophrenia. (...)

rob halkes's insight:

Lots of progress in new directions of scientific research developments now paying of.

To get content containing either thought or leadership enter:

To get content containing both thought and leadership enter:

To get content containing the expression thought leadership enter:

You can enter several keywords and you can refine them whenever you want. Our suggestion engine uses more signals but entering a few keywords here will rapidly give you great content to curate.

Your new post is loading...

Your new post is loading...

Pharma's reputation is rising in heart and circulatory conditions. Pfizer ranks first. See for the full report here: http://www.patient-view.com/corp-rep---pharma-therapy-areas.html