Your new post is loading...

Your new post is loading...

|

Scooped by

Linda Holroyd

March 16, 2016 11:59 AM

|

The CDO role is changing dramatically. Here are the skills today’s world demands. In the alphabet soup that is today’s crowded C-suite, few roles attract as much attention as that of the chief digital officer, or CDO. While the position isn’t exactly new, what’s required of the average CDO is. Gone are the days of being responsible for introducing basic digital capabilities and perhaps piloting a handful of initiatives. The CDO is now a “transformer in chief,” charged with coordinating and managing comprehensive changes that address everything from updating how a company works to building out entirely new businesses. And he or she must make progress quickly. SidebarDo you need a CDO? Given these demands, it’s not surprising that the number of people in CDO roles doubled from 2013 to 2014 and is expected to double again this year.1We find that companies bring in a CDO for two primary reasons. The first is when they need to approach the complex root causes that must be dissected, understood, and addressed before any substantive progress on digitization can be made. And the second is when the CEO realizes the organization can’t meet the primary challenge of creating integrated transformation within its current construct (see sidebar, “Do you need a CDO?”). In fact, the true measure of a CDO’s success is when the role becomes unnecessary: by its very nature, a high-functioning digital company does not need a CDO (however, it may want its former CDO to be the CEO). Of course, the vast majority of organizations are not yet at that point. And while there are numerous actions companies can and should take to help these executives work themselves out of a job—such as providing sufficient resources and active CEO support—this article focuses on five areas CDOs themselves must get right if their organizations are to successfully transition to digital. 1. Make digital integral to the strategy Digital isn’t merely a thing—it’s a new way of doing things. Many companies are focused on developing a digital strategy when they should instead focus on integrating digital into all aspects of the business, from channels and processes and data to the operating model, incentives, and culture. Our analysis of how companies with a high Digital Quotient (DQ) operate shows that 90 percent of top performers have fully integrated digital initiatives into their strategic-planning process.2 Getting the strategy right requires the CDO to work closely with the CEO, the chief information officer (CIO), business-unit leaders, and the chief financial officer; the CDO also needs to be an active participant in and shaper of the strategy. An important foundation for CDOs to establish credibility and secure a seat at the strategy table is providing detailed analysis of market trends and developments in technology and customer behavior, both inside and outside the sector. Yet CDOs can’t stop there. They need to bring a bold vision: 65 percent of companies that are “digital leaders” in our DQ analysis have a high tolerance for bold initiatives; among average performers, 70 percent of companies don’t see support for risk taking. This vision could include starting new businesses, acquiring technologies, or investing in innovations—one CDO we know made it his mantra to drive agile as a new software-development methodology for 40 percent of the company’s projects. No matter how it’s branded, CDOs need to be known within their organization for something that is courageous, new, and adds value. In addition, CDOs must be specific about their goals. One international publishing house, for example, set a target of generating 50 percent of its revenue and profit from digital media within ten years, and it wound up doing so in almost half that time. Similarly, several banks that set the objective of increasing digital-channel sales to more than 50 percent are seeing that specific and measurable goal rally the organization. Read more about Digital Quotient

2. Obsess over the customer While most companies say they know their customers, CDOs must make it a driving passion and core competency of the organization. With technology and customer habits changing so quickly, developing a deep and detailed view of customer behavior across all channels provides a common reference point in any business discussion and arms the CDO to challenge the status quo and make changes. For example, one CDO used the concept of customer journeys and big data mapping of these paths to show her peers where opportunities and pain points existed—and, in doing so, destroyed several myths. This type of analysis is critical, to be sure, but an equally important part of the CDO’s job is communicating how essential the customer is to the organization. One CDO created clear and visually compelling dashboards on the customer journey and made a habit of consistently referencing them in meetings and when making decisions. Another set up a digitally enabled “war room” with real-time reporting on several key digital metrics, which soon will be piped to the tablets and smartphones of other C-suite executives. Yet another CDO sends regular company-wide emails highlighting customer breakthroughs, insights, and “voice of the customer” anecdotes. Such actions can help the business start to think more specifically about the customer so that everyone approaches all issues with a single crucial question: How will this affect the customer? Digital capabilities ultimately provide an important foundation for improving the customer experience. It’s up to the CDO to identify those functions where digital is critical: for example, investing in automation capabilities to rapidly respond to customer interactions, developing sophisticated reporting and analytics capabilities to interpret customer needs, building innovative interfaces to gather customer data (for example, an alternative payment method), and creating mechanisms to deliver content and offers across all relevant channels. While the CDO will need to work closely with marketing and IT leadership, he or she should define the customer-experience journey and identify the requirements for developing and then supporting a dynamic system that is constantly learning and evolving. 3. Build agility, speed, and data CDOs can build strong foundations for change by creating a “spirit of digital” throughout the organization. That could include setting up coding days for the board or holding company-wide hackathons—one company we know even had drones flying around the atrium of its headquarters. Core to building this spirit, however, is increasing the “metabolic rate” of the organization. That starts with changing basic habits, such as having strategy leadership meetings weekly or even biweekly to help ingrain the idea of moving at a faster pace. CDOs must look at how the organization operates and find ways to inject speed into processes. In some cases, it could be as straightforward as working with IT to automate existing development processes. But in others, it will require radically changing how the company works, such as setting extremely aggressive goals—as few as six weeks—for getting a product to market. Some CDOs do this by setting up “digital factories,” which are cross-functional groups focused on developing one product or process using a different technology, operational, or managerial methodology from the rest of the company. Embedding these factories in business units has the advantage of spreading the new culture and making the digital-factory approach the norm. Managing a portfolio of these types of initiatives requires leaders to be decisive. If the data show a prototype doesn’t work, the CDO must be ruthless about killing the project, incorporating anything learned from the experience, and moving on. On the other hand, CDOs should establish flexible budgeting processes so that projects that show signs of success can get resources to scale quickly. 4. Extend networks In a digital world, threats often do not come from established competitors but rather from innovative technologies that enable new businesses, start-ups that undermine established business models, or new developments outside the way the company defined its competitive space. For example, one of the big trends in the payments sector is the merging of commerce and payments functionalities in the same app—so, being able to pay for your restaurant meal using the OpenTable app you used to reserve your table. Successful CDOs are keenly aware of such trends. They build networks of people, technologies, and ideas far outside of their company, constantly scanning the small-business landscape to identify possible acquisitions or partners that can provide complementary capabilities. Some CDOs spend as much as 50 percent of their time working with external partners to build effective working relationships that take advantage of every organization’s capabilities. To help bring these outside voices into the organization, many CDOs establish advisory boards of start-up leaders or create “challenger” boards of people with digital experience and expertise to review corporate initiatives and strategies. At a more pedestrian level, they regularly invite technologists or entrepreneurs to team lunches. Building an internal network is just as important because company systems and technologies need to be flexible enough to work with outside parties. In particular, CDOs need to work with IT leaders to develop application programming interfaces and cloud-based architecture that works with a broader ecosystem of providers. Some CDOs realize too late that functions such as compliance, finance, human resources, legal, procurement, and risk also need to change to support a more digitally focused company. At one company, for example, an effort to accelerate time to market is in full swing, but procurement still insists it requires six months to approve a vendor. Changing such supporting processes isn’t easy—functions often have good reasons for why processes are undertaken as they are. But brokering compromises and testing new ways of operating that are necessary to make progress will be virtually impossible if a CDO doesn’t build internal networks early and engage with leaders across the business. 5. Get stuff done CDOs are ultimately judged not by the quality of their ideas but by their ability to lead different types of teams, guide projects, overcome hurdles, and deliver integrated change. Getting stuff done often requires hard-nosed negotiating skills. Consider the CDO at a financial-services company who wanted to stop business units from draining IT resources on independent projects that didn’t align with the overarching strategy. The CDO worked closely with the CIO and agreed to use her new budget to fund some of his projects; she also helped him retain and motivate key people by staffing them on important digital initiatives (which also assured him visibility into what she was doing). In return, the CIO agreed to stop supporting initiatives that the CDO didn’t explicitly approve. Both won in the end, and they now have a close working relationship. A new CDO will benefit from the early establishment of near-term goals that can yield quick wins and wow moments that help build enthusiasm and momentum. Some CDOs find that building the marketing-commerce function is a great way to quickly demonstrate value, while others embark on accelerated cost cutting by automating core processes. It pays to define how success is measured, whether it’s tracking key digital and business metrics—such as digital-media revenue as a percentage of total revenue—or creating a full digital profit-and-loss statement (or both). To be meaningful for the business overall and to build credibility, key performance indicators must be aligned with those used by established business units. Within his first month, for example, the new CDO at one financial-services company defined clear, discrete digital initiatives; developed a long-term vision in partnership with an anchor business-unit leader; and got his budget approved. Within six months, he hired a handful of key employees, launched several initiatives, identified gaps in the organization, and pulled together teams to fill them. A year and a half into the job, he was able to claim some solid wins and moved from a “shadow” profit and loss to an explicit one. Of course, the projects CDOs commit to must be core to the business—such as developing new revenue streams, cutting costs, or getting to market faster—and not peripheral experiments, which could end up marginalizing their efforts. We’ve actually found it works best when a CDO’s budget is funded through the efficiencies and growth that he or she drives. In addition, we believe that budgeting is critical to ensuring that things get done. Successful CDOs not only time their actions to maximize budgetary flexibility but also change how funding is allocated. One CDO shifted from annual approval of large capital expenses for IT to a more venture capital–like monthly cycle, ensuring he could get more projects funded and launched. This approach also served to maintain funding momentum, with small bites over the course of the year predicated on demonstrated effectiveness. Defining characteristics of the new CDO When hiring a CDO, people often agonize over finding someone with experience that is just right. Yet we’ve found it’s the ability to lead transformation across an organization that is the true indicator of likely success in the role, and that requires a combination of hard and soft skills. Hard skills include the ability to articulate a strategic vision, the means to take on problems by identifying root causes across functions and making the tough decisions necessary to resolve them, experience in “pure play” digital and larger company transformations (typically in the consumer and technology sectors), and the managerial ability to lead and see programs through to fruition. The importance of soft skills should not be understated: some CDOs estimate they spend 80 percent of their time building relationships. In our experience, successful CDOs have the patience to navigate the complex organizational structures of large businesses; additionally, they collaborate to get buy-in across functions and are able to diplomatically challenge the status quo and solidify relationships with a broad group of people. They also demonstrate leadership and charisma that excites the organization to drive change forward. Of course, companies would be lucky to have executives in any function with this skill set. But driving organization-wide change isdifferent from the mandate for other senior roles. A recent Russell Reynolds Associates survey found that CDOs are meaningfully different from other senior executives across five categories: they are on average 34 percent more likely to be innovative and 32 percent more likely to be disruptive, and also differ with regard to determination, boldness of leadership, and social adeptness.3Leading an organizational transformation is messy work that requires masterful social skills to implement digital initiatives that create disruption by their very nature. Indeed, a CDO’s strong bias for action, bold thinking, and high tolerance for risk requires someone who can also manage the ruffled feathers, bruised egos, and flaring tempers that are common fallout from his or her activities. As the digital age scrambles the traditional organizational structure, CDOs must not only launch the organization on its digital trajectory but also help it fundamentally evolve. The role requires a “bifocal” approach: achieving the near-term imperative of getting things moving quickly, while setting in place the longer-term conditions of success so the organization can compete digitally. Those CDOs that succeed will truly have earned their place in the already-crowded C-suite. About the Authors Tuck Rickards is a managing director at Russell Reynolds Associates, where he coleads the executive-search company’s Digital Transformation Practice. Kate Smaje is a director in McKinsey’s London office, and Vik Sohoni is a director in the Chicago office.

|

|

Scooped by

Linda Holroyd

March 16, 2016 11:38 AM

|

Chinese consumers continue to grow relentlessly in number and wealth. This is a well-studied economic trend. But what people are missing is how the changing behavior of these consumers is now regularly shaking the world.

Suddenly, when Chinese consumers change their minds about something, it ripples outward into the global economy. And this phenomenon is going to get a lot more noticeable in the next years.

The economic trend underlying this is the steady advance of China's urban middle class families. This is the group to watch. According to McKinsey & Co., Chinese urban household disposable income will reach $8,000 a year by 2020. This will be about the same level as South Korea, but in a much, much larger population. After Middle Eastern oil, Chinese urban middle class families are arguably the most valuable natural resource on the planet.

But within this big trend, an important shift is now occurring. Urban families are rapidly transitioning from "value hunters" to more emotional, aspirational and free-spending consumers.

Price-focused consumers have dominated the China story thus far. They typically have had little brand loyalty and tend to shop around for the best deals, mostly for life's necessities. Chinese companies such as Haier Group and China Vanke have done very well selling these consumers air conditioners and apartments at affordable prices.

The more emotional group now emerging, called "new mainstream" consumers by McKinsey, already has life's basics. And they have enough disposable income to buy discretionary items such as lattes and trips to Thailand. What they care about is quality, brands and how products make them feel. So they want real iPhones, not cheap alternatives, and they are able and willing to pay for them. What is fascinating about this group is that they behave similarly to consumers in developed markets.

And here's the factoid that matters. These "new mainstream" consumers accounted for about 5% of China in 2010, with value seekers then accounting for the overwhelming majority. But according to McKinsey, the new mainstream will represent at least half of urban middle class families by 2020. This is the important transition that is happening right now.

It means Chinese consumers are rapidly becoming much more emotional and unpredictable. Suddenly, when Chinese consumers like a movie, such as "Star Wars: The Force Awakens," they become one of the biggest source of revenue for it.

In 2015, McDonald's, KFC and other U.S. fast-food chains got a painful lesson in this phenomenon after media reports of alleged contaminated food in their Chinese outlets. Their global financial results took significant hits. While reported as a food scandal, this incident was really about urban Chinese families caring more about food safety now than in the past.

Overwhelmed

Conversely, if Chinese consumers decide that a particular brand is safe or better than its rivals, foreign companies can suddenly be overwhelmed with orders. This recently happened to Swisse Wellness Group, one of Australia's leading vitamin and supplement companies.

During the first half of 2015, Swisse, which had virtually no operations in China, suddenly found its sales there growing very rapidly. It turned out that Chinese consumers had begun ranking its products highly on Tmall. Revenues for the year (ended in June) jumped to A$313.1 million ($235 million) from A$125.6 million a year earlier. And unsurprisingly, a Chinese company (Biostime International Holdings) quickly bought Swisse in A$1.39 billion deal.

Another example is the story of the Bobbie Bear, a bright purple teddy bear stuffed with lavender and sold by a farm in Tasmania. This small lavender farm, a retirement project of owner Robert Ravenus, became inundated with orders after Chinese model / actress Zhang Xinyu posted a photo of her Bobbie Bear online. Orders surged to more than 45,000 and the farm was forced to suspend online sales, as it could not handle the demand from China.

The company then had to place limits on how many bears could be bought by visitors to the farm's gift shop. Chinese tourists were showing up in Tasmania in droves to make purchases. Annual visitors to the farm exceeded 60,000. At one point, a hacker, presumed to have been Chinese, broke into the farm's computer system to try to place orders.

My point is that increasingly emotional Chinese consumers (i.e., less pure value seeking) are now regularly causing events such as this around the world.

Increasing mechanisms

A second important factor is that the mechanisms through which Chinese consumers can impact companies around the world are increasing. The Swisse vitamin example was possible because cross-border e-commerce, known as "haitao" in China, now lets consumers there buy overseas goods online and get them delivered. Both Amazon and Tmall are charging after this cross-border opportunity right now.

Another mechanism is real estate. Every six to 12 months, Chinese consumers seem to discover a new favorite place and start buying huge numbers of homes there. This phenomenon started in Hong Kong a few years ago. Buying then switched to Vancouver and Toronto. In the last year, we have seen heavy Chinese purchasing of homes in New York and California.

Tourism is another powerful mechanism. The number of trips abroad by Chinese tourists now exceeds 120 million a year and their travels tastes can be unpredictable as well. For example, following the 2012 hit movie "Lost in Thailand," Chinese tourists started flooding into Chiang Mai, the main tourist hub in the area where the movie was filmed. Arrivals to the city were reportedly up 500% in 2013 alone.

So in 2016, two important factors are coming together: the increasingly emotional behavior of Chinese consumers (who are growing in power) and a multiplication of the mechanisms by which this influence can impact the world, often in real-time.

What this means for markets and businesses around the globe is that they can now be directly impacted by what is discussed at dinner tables, in offices and online in China. My recommendation is to start paying attention to those conversations.

|

|

Scooped by

Linda Holroyd

March 15, 2016 5:55 PM

|

July 2015, during the championship round of the World Surf League’s J-Bay Open, in South Africa, a great white shark attacked Australian surfing star Mick Fanning. Right before the attack, Fanning said later, he had the eerie feeling that “something was behind me.”1 Then he turned and saw the fin.

Thankfully, Fanning was unharmed. But the incident reverberated in the surfing world, whose denizens face not only the danger of loss of limb or life from sharks—surfers account for nearly half of all shark victims—but also the uncomfortable, even terrifying feeling that can accompany unseen perils.

Just two years earlier, off the coast of Nazarre, Portugal, Brazilian surfer Carlos Burle rode what, unofficially, at least, ranks as the largest wave in history. He is a member of a small group of people who, backed by board shapers and other support personnel, tackle the planet’s biggest, most fearsome, and most impressive waves. Working in small teams, they are totally committed to riding them, testing the limits of human performance that extreme conditions offer. Instead of a threat of peril, they turn stormy seas into an opportunity for amazing human accomplishment.

These days, something of a mix of the fear of sharks and the thrill of big-wave surfing pervades the executive suites we visit, when the conversation turns to the threats and opportunities arising from digitization. The digitization of processes and interfaces is itself a source of worry. But the feeling of not knowing when, or from which direction, an effective attack on a business might come creates a whole different level of concern. News-making digital attackers now successfully disrupt existing business models—often far beyond the attackers’ national boundaries:

Simple (later bought by BBVA) took on big-cap banks without opening a single branch.

A DIY investment tool from Acorns shook up the financial-advisory business.

Snapchat got a jump on mainstream media by distributing content on a platform-as-a-service infrastructure.

Web and mobile-based map applications broke GPS companies’ hold on the personal navigation market.

No wonder many business leaders live in a heightened state of alert. Thanks to outsourced cloud infrastructure, mix-and-match technology components, and a steady flood of venture money, start-ups and established attackers can bite before their victims even see the fin. At the same time, the opportunities presented by digital disruption excite and allure. Forward-leaning companies are immersing themselves deeply in the world of the attackers, seeking to harness new technologies, and rethinking their business models—the better to catch and ride a disruptive wave of their own. But they are increasingly concerned that dealing with the shark they can see is not enough—others may lurk below the surface.

Deeper forces

Consider an insurance company in which the CEO and her top team have reconvened following a recent trip to Silicon Valley, where they went to observe the forces reshaping, and potentially upending, their business. The team has seen how technology companies are exploiting data, virtualizing infrastructure, reimagining customer experiences, and seemingly injecting social features into everything. Now it is buzzing with new insights, new possibilities, and new threats.

The team’s members take stock of what they’ve seen and who might disrupt their business. They make a list including not only many insurance start-ups but also, ominously, tech giants such as Google and Uber—companies whose driverless cars, command of data, and reimagined transportation alternatives could change the fundamentals of insurance. Soon the team has charted who needs to be monitored, what partnerships need to be pursued, and which digital initiatives need to be launched.

Just as the team’s members begin to feel satisfied with their efforts, the CEO brings the proceedings to a halt. “Hang on,” she says. “Are we sure we really understand the nature of the disruption we face? What about the next 50 start-ups and the next wave of innovations? How can we monitor them all? Don’t we need to focus more on the nature of the disruption we expect to occur in our industry rather than on who the disruptors are today? I’m pretty sure most of those on our list won’t be around in a decade, yet by then we will have been fundamentally disrupted. And how do we get ahead of these trends so we can be the disruptors, too?”

This discussion resembles many we hear from management teams thoughtful about digital disruption, which is pushing them to develop a view of the deeper forces behind it. An understanding of those forces, combined with solid analysis, can help explain not so much which companies will disrupt a business as why—the nature of the transformation and disruption they face rather than just the specific parties that might initiate them.

In helping executives to answer this question, we have—paradoxically, perhaps, since digital “makes everything new”—returned to the fundamentals of supply, demand, and market dynamics to clarify the sources of digital disruption and the conditions in which it occurs. We explore supply and demand across a continuum: the extent to which their underlying elements change. This approach helps reveal the two primary sources of digital transformation and disruption. The first is the making of new markets, where supply and demand change less. But in the second, the dynamics of hyperscaling platforms, the shifts are more profound (exhibit). Of course, these opportunities and threats aren’t mutually exclusive; new entrants, disruptive attackers, and aggressive incumbents typically exploit digital dislocations in combination.

We have been working with executives to sort through their companies’ situations in the digital space, separating realities from fads and identifying the threats and opportunities and the biggest digital priorities. Think of our approach as a barometer to provide an early measure of your exposure to a threat or to a window of opportunity—a way of revealing the mechanisms of digital disruption at their most fundamental. It’s designed to enable leaders to structure and focus their discussions by peeling back hard-to-understand effects into a series of discrete drivers or indicators they can track and to help indicate the level of urgency they should feel about the opportunities and threats.

We’ve written this article from the perspective of large, established companies worried about being attacked. But those same companies can use this framework to spot opportunities to disrupt competitors—or themselves. Strategy in the digital age is often asymmetrical, but it isn’t just newcomers that can tilt the playing field to their advantage.

|

|

Scooped by

Linda Holroyd

March 15, 2016 1:53 PM

|

Technologists from across the globe recently gathered in Barcelona for the Mobile World Congress, the annual conversation on connectivity and celebration of new gadgets. While the conference traditionally focuses on phones, the discussions about mobile—in Barcelona and beyond—have grown increasingly wide-ranging as mobile technologies continue to seep into more areas of daily life. As one journalist covering the conference eloquently noted, "The Internet is becoming an invisible fabric—like air—that enables all the services we’ve come to depend on." In this schema, mobile devices and their apps are the stitches weaving together these services that help us work, play and live.

Indeed, the rise of mobile technologies has spurred the transformation of industries once considered sleepy into areas where some of the hottest new startups are operating. Uber and Lyft drivers have largely displaced cabbies; Airbnb has won over travelers who had previously booked hotel rooms; Postmates couriers have sped past the bike messengers of yesteryear with their promise of any local product delivered to your door in under one hour.

Looking at the common denominators of these startups gives us some clues about where the next mobility-enabled disruption might occur. First, these companies all offer services characterized by high time-sensitivity. After all, it's far more likely that someone waiting for a ride they've requested will return to a service that supplies a driver in four to five minutes as opposed to ten. By bypassing the dispatching step of traditional cab companies with location-based data capabilities, Uber et al. have cornered that competitive edge.

Second, these companies invest in technology but stay capital light by relying on assets that are already owned by the independent providers they partner with: Cars, bikes, houses and apartments. This low barrier to entry for service providers—no pricey taxi medallion to buy or hotel to maintain— results in the greater supply that drives down costs for consumers and thereby renders these services more desirable.

Finally, these companies are able to use technology to turn what I'll call "serendipity" into operating efficiencies. Theoretically at least, Lyft drivers or Postmates couriers accept jobs close to where they already are when the job comes up. Jobs are done more quickly, which means that workers make more money in less time and customers are more satisfied.

While a variety of industries have one or more of these features of providing time-sensitive services, possessing the option to rely on shared assets, and capitalizing on serendipity, I believe three more traditional areas especially ripe for mobile-enabled disruption are healthcare, staffing and banking. Watch these spaces if you're looking for the next company to have its "Uber moment."

Healthcare

Pioneers in telemedicine are improving access to care for patients who live in underserved areas or who can't otherwise travel to their doctor's offices. Startups like American Well and Doctor on Demand offer live video doctor visits via mobile app for a relatively small patient fee, and they're starting to gain momentum in part by making inroads to employer-sponsored plans. These services might be especially valuable in the arena of mental health, where on-demand offerings are growing and a shortage of face-to-face appointment availability means that patients are often unable to get the timely help they need to avoid crisis.

Staffing

Many of today's contingent workers find project-based "gigs" and other short-term work using mobile workforce platforms like Upwork, Fiverr and the company I co-founded, Gigwalk. The rise of such platforms has changed the game not just for independent workers, but also for HR departments and staffing agencies, which must now bolster their technological capabilities to stay competitive. The employers of today want to work with staffing partners who can anticipate and meet constantly and rapidly shifting staffing needs. The day when the average staffing agency employee wakes up and glances at an app on her phone to get that day's work location and assignment is closer than we think.

Banking

Brick-and-mortar and online-only banks alike have been quick to offer mobile apps that let their customers check balances, transfer funds and deposit checks from their phones, but there's still room for innovation in the key area of cash transfer. While mobile apps like Venmo and Circle let users send or receive cash instantly via text at no charge, we still haven't seen this capability offered at large scale and integrated with other banking services. The area is ripe for players who can wrap these services together at a low price point.

Just like EBay changed the garage sale to a large-scale virtual goldmine in the '90s as it used the Internet to match far-flung buyers and sellers, mobile is causing another wave of disruption that will reward a new crop of innovative players. Wherever they emerge from, they promise to further ease the "life on-the-go" that is our 21st century reality.

|

|

Scooped by

Linda Holroyd

March 7, 2016 5:22 PM

|

What Will The Next President Do About Obamacare?

With the presidential elections less than a few months away and the race to the White House heating up, it is a good time to take stock and assess the future of healthcare in the United States. The election of a Democrat for president is widely expected to result in a continuation and expansion of the goals set out by the Affordable Care Act (ACA), while the election of a Republican will most certainly result in a roll back of some, if not all, of the act’s key initiatives. What we can expect from either of these electoral outcomes depends entirely on the individual in the Oval Office, the amount of Congressional support he or she is able to generate, and the overall healthcare objectives outlined by the next administration.

Precinct captain Christa DeHerrera, left, puts a band on voter Janell Lindsey after she checked in at a Democratic caucus late Tuesday, March 1, 2016, in Denver. (AP Photo/David Zalubowski)

Scenario 1: Assessing the Healthcare Landscape Following a Democrat Victory

Hospitals will Continue to Benefit from Rise in Insured Population

A Democratic presidential victory will broadly result in the continuation of the ACA with potential to increase the scope, subject to favorable congressional approval. In this scenario, patients will benefit greatly through greater state-based adoption of health exchanges, enhanced federal subsidies from policies purchased on national exchanges and removal of exclusion criteria by insurers. This continued growth in insurance patient base will reduce declining hospital volumes and increase revenues. As per a Moody’s assessment of hospital financial performance in 2015, an increased insurance base has resulted in not-for-profit hospitals witnessing rising revenues (compared to a decline in 2014), while the financial status of for-profit hospitals has shifted from “stable” to “profitable.” Hospitals will use these revenues to provide high-quality acute care services, as well as play a greater role in pioneering novel therapies such as genetic medicine, nano medicine and 3D printing health technologies.

Retail Clinics: The New Linchpin of Care Provision

Rise of ambulatory care providers such as retail clinics and urgent care centers will be critical in transitioning chronic and non-critical emergency care away from hospitals. Hospitals will leverage the rise of these service providers to further decongest emergency wards, reduce operating costs and transition chronic care management of patients outside the hospital. At the same time, ambulatory service providers will also act as patient referral nodes for hospitals. As of 2015, over 100 partnership agreements had been signed between various hospitals/health systems and ambulatory care providers. The number of deals will extend significantly post-2017 as hospitals seek greater collaboration with ambulatory care providers. With an average cost of $100 to $150 per consultation in retail and urgent care clinics, insurers will seek to incentivize patients covered by their plans to seek care from these providers whenever possible.

Primary Care: In Desperate Need of an Overhaul

While primary care will continue to play a key role in the healthcare value chain, with over 60% of primary care practices acquired or in partnerships with hospitals or health systems, the high cost of primary care services and an expected shortage of 46,000 to 90,000 primary care doctors over the next few years will experience the adoption of primary care technologies, such as telemedicine and virtual consultation services, to improve efficiency of care provision.

CMS Spending will Continue to Remain the Bedrock of U.S. Healthcare Spending

While Medicare reimbursements will continue to decline across healthcare providers, greater statewide adoption of Medicaid expansion services will play a key role in financing care, especially for elderly patients and those suffering from one or more chronic conditions requiring care in a specialty long-term care hospital or in residential, semi-residential and nursing facilities. With 283 rural hospitals at risk of closure, Medicaid expansion will be critical in ensuring financial stability of rural hospitals. As of 2015, only 8.3% of rural hospitals were at risk of closure in Medicare expansion states, compared to 16.6% in non-Medicare expansion states. With a rapidly aging population and increase in chronic diseases, enhanced Medicare expansion will be critical in ensuring greater affordability and accessibility to care.

Scenario 2: Assessing the Healthcare Landscape Following a Republican Victory

Reduced Insurance Coverage, Lower Inpatient Volumes and Falling Hospital Revenues Sound the Death Knell for Hospital-Based Innovation

A Republican presidential victory will most likely result in a rollback of some ACA elements, if not the act in its entirety. Rollback of health insurance exchanges, including public, private, state and federal, will likely be the first step, which will result in the reintroduction of exclusion criteria and high co-payment plans for those suffering from pre-existing conditions. This will result in a reduction of patient base, which, in turn, will cause a steep decline in hospital inpatient volumes. This reduction in volumes will undermine and eventually erode the revenue gains made by not-for-profit hospitals over the past year. Traditionally, for-profit hospitals have been more adept at responding to market changes. In the coming years for-profit hospitals will be capable of holding on to patient volumes but will witness reductions in profits. These reduced revenues, coupled with ongoing Medicare cuts, will prevent hospitals from offering high-quality acute care services. Research of novel therapies such as genetic and nano medicine will remain within academic institutions, with large-scale utilization delayed by several years.

Ambulatory Care Providers: Overburdened, Underfunded and Stretched

In this environment, ambulatory care providers will become the de facto providers of choice for the increasing number of uninsured patients, most of which suffer from chronic conditions. Lack of insurance coverage for these types of patients will result in patients having to pay for services out of pocket. This will lead to sluggish revenue growth and will impact the rate at which these providers expand service lines and increase geographical coverage. In this scenario, hospitals will find it increasingly difficult to transition chronic care to these providers, resulting in increasing operating costs, which will impact hospital emergency wards the most.

No Country for Old Men (and Women)

The biggest impact of a Republican victory will most likely be rollback of Medicaid expansion across individual states. While existing Medicaid expansion states may not choose to roll back services, chances of adoption by non-Medicaid expansion states will reduce significantly. This will adversely impact financial health of rural hospitals and LTC providers, resulting in serious gaps in healthcare provision, especially for those patients living in remote areas and those who require 24/7 oversight and care management. With a rapidly aging population and rising incidence of chronic diseases, care providers will become ill-equipped and ill funded to handle the demand for LTC services, resulting in a huge economic burden on caregivers and patient family members.

Placing Pragmatism before Emotion and Rhetoric

Should a Republican win the presidency, he must take steps to ensure that the ACA will continue to be enforced. Rollback of elements of the act, while appealing to conservatives within the party, would most certainly create serious long-term damage to healthcare systems’ ability to cope with the increased demand for care services while continuing to be at the forefront of global medical innovation. It is absolutely imperative that a careful study be conducted to assess the efficacy of the ACA on various aspects of care in order to understand how to make the act more efficient and align it closer to the goals of the next administration.

This article was written with contribution from Tanvir Jaikishen, Senior Research Analyst with Frost & Sullivan’s Transformation Health Program.

|

|

Scooped by

Linda Holroyd

March 1, 2016 6:15 PM

|

There’s been so much change in the way companies, leaders and businesses work with each other and together, so it’s difficult to plan your future, whether you’re new to the workforce, returning to the workforce or planning how to remain gainfully employed in later years. Here are my thoughts on the type of work that’s available and how to embrace these opportunities and and prepare for the challenges to come. - The tech-philic worker will be favored, and those who reject or deny this fact will be much less employable. Technology will help workers to gather and interpret data and information so that they can be more productive and better serve the customer, both of which are critical to the performance of any company.

- The learning-agile worker will be favored. Those who are resistant to learning new ways of doing things will be left behind, especially as automation will replace the need of workers-who-perform-repetitive-tasks.

- The communicative worker will more likely succeed as it would be easier for them to work with all the internal and external stakeholders involved in any job – from colleague to teammate, from partner to customer.

- The patient, helpful, service-oriented worker will be better positioned to serve demanding customers. There will always be jobs for people who know how to make even the pickiest of customers happy.

- Collaboration between people and companies will more likely succeed. Leaders will be those who can envision the benefits of collaborating across roles, companies and industries, and create and facilitate those successful partnerships.

- If you combine the 5 traits above, you will find a worker who may be able to tailor products and services to the needs of the customer. There will always be a role for people who can succeed in doing this well.

- Company leaders will be more focused on data and analytics, and there will be more meritocracy-based cultures and less politics.

- Along those same lines, productivity of people and product/service lines will be based more on data and information, and less on politics and agendas.

- Company leaders will help make it easy for adiverse population of workers to succeed – whether it’s making remote work possible or providing tech tools to support an aging or disabled or other non-standard worker.

- The bottom line is that companies and leaders will acknowledge that they are only as good as their people, and think, speak and act accordingly.

Those are my thoughts on the Future of Work. How will these things impact YOU? Your comments are welcome.

|

|

Scooped by

Linda Holroyd

February 18, 2016 6:10 PM

|

Thanks to NewCo, I’ve gotten out of the Bay Area bubble and visited more than a dozen major cities across several continents in the past year. I’ve met with founders inside hundreds of mission-driven companies, in cities as diverse as Istanbul, Boulder, Cincinnati, and Mexico City. I’ve learned about the change these companies are making in the world, and I’ve compared notes with the leaders of large, established companies, many of which are the targets of that change. (First published at NewCo. Get the NewCo newsletter here) As I reflect on my travels, a few consistent themes emerge: 1. Technology has moved from a vertical industry to a horizontal layer across our society. Technology used to be a specialized field. Technology companies sold their wares to large companies in large, complicated IT packages and to consumers as discrete products (computers and software applications). In the past decade, technology has dissolved into the fabric of our society. We all can access powerful technology stacks. We don’t need to know how to program. We don’t need a big IT department either. Now, technology is infrastructure, like our physical systems of highways and roads. This levels the playing field so new kinds of companies can emerge, and it’s forcing big companies to respond to a new breed of competitor, as well as a newly empowered (and informed) consumer base. 2. Big companies are on the precipice of the most wrenching transformation in history — and tech is only part of the reason why.BigCos change very slowly. They are cautious by nature and extremely suspicious of “the new.” BigCos study new developments and wait for proof before they change. As digital technology spread through society over the past three decades, big companies were slow to get a web page, slow to conduct business over the web, slow to lean into mobile and social, and slow to respond to new types of startup competition. Of course, now that the web is mature and consumer platforms like Facebook and Google are massive, BigCos have shifted resources to digital. But that last point — responding to startup and business model competition — is far more problematic, because responding to new kinds of competition isn’t something you can outsource. It requires a fundamental shift in corporate social structure — and culture is hard to change. 3. The next generation’s leaders don’t want to work at BigCos (if they don't have to). In the past year I’ve met with senior executives at massive companies like Nestle, Publicis, P&G, Walmart, Visa, and McDonald’s. When I ask what keeps them up at night, all of them answer “hiring the next generation of leaders.” The best and brightest now see “launching a company,” “working at a startup,” or “working at a digital leader like Google or Facebook,” as a preferable career choice, starving BigCos of their most valuable asset: talent. While one might dismiss young professionals’ penchant for startups as a fad or a phase, there’s something far deeper at work, namely … 4. A job is table stakes. To win talent, companies must compete on purpose, authenticity, and organizational structure. Millennials are now the largest force in the global economy, and they have a markedly different view of work: Purpose and “making a difference in the world” are central in their work-related decisions. They’d rather work at The Honest Company than Unilever, if given a choice — and the best and brightest always have a choice. Members of the next generation want to be at a company where work means more than a paycheck. They believe work can be a calling (Reich) or an expression of our creativity (Florida). BigCos aren’t currently organized to enable their workforces in this way (human resources, anyone?), but NewCos — even the very largest ones like Google — most definitely are. 5. Today’s consumers are newly empowered and are making decisions on more than price. If millennials are choosing employers based on purpose and authenticity, it follows that they decide how they spend their money in similar fashion. Convenience, selection, and price are important, but new kinds of competitors are exposing weaknesses in big companies’ essential truths, and that’s an existential threat. Dollar Shave Club questions Gillette’s core premise,MetroMile questions Geico’s core premise, Earnest does the same to large financial institutions, HolaLuz to energy companies, and the list goes on. Companies profiting from practices or products that demonstrably create more harm than good in the world are threatened in an age of transparency and accountability. Regardless of good intent or excellent marketing, if your business makes people unhealthy, or depends on exploitation of vulnerable workers, or can be laddered to climate change, it’s at risk of mass consumer migration to businesses with better narratives. 6. The platform economy means traditional competitive moats are falling away. Today’s largest consumer companies earned their power by consolidating and optimizing their access to commodities (what their products were made of), manufacturing (how their products were made), and distribution (where their products were sold and how people became aware of them). They were built on humanity’s first global platforms: television and mass transportation networks. We all know that the Internet undermined this hegemony; physical distribution is no longer a surefire competitive advantage (just ask Walmart). But what’s not well understood is how quickly other parts of the product stack have become platform-ized. Just as startups can now access technology as a service, they can also access sourcing and manufacturing as a service (Dollar Shave doesn’t make its blades, for example). This of course bolsters point #5 above: If any company can access the same economies of scale, brands must compete on more than price or distribution, they must compete on voice, innovative (and information-first) approaches to markets, and purpose. 7. Cities are resurgent. I just returned from Mexico City, which earlier this month hosted its first NewCo festival. While there, I heard a refrain consistent with my visits around the world: The city is changing for the better and new kinds of companies are at the heart of that change. When people gather at NewCo meetups or inside NewCo sessions, I keep hearing “There’s just no way these kinds of companies could have made it in this city ten years ago.” Coupled with the horizontal force of technology and the rise of a purpose-driven zeitgeist, cities have become both the epicenter of humanity’s greatest challenges, as well as the birthplace of our greatest innovation. One generation ago, one-third of humanity lived in urban centers. Today, it’s more than 50 percent. One generation from now, more than two-thirds of us will reside in the tangled banks of a city center, and that number will surpass 80 percent by the end of this century. Cities offer access to capital, education, regulatory frameworks, and a collaborative density of human curiosity and connections. It’s where great companies are born and grow. 8. BigCos are deeply aware of all this — and a massive shift is about to reveal itself. For as long as I’ve been in the media and technology business, I’ve heard big company executives proclaim they were committed to change. But it always rang hollow: Large companies expended far more resources preventingchange than they ever did committing to it. Over the past year, however, I’ve sensed a deep shift in the tone of my conversations with BigCos. These are some of the smartest people in the world, and they understand the technological, generational, and social tectonics at play. In their board rooms and C-suites, conversations are already underway about changes so significant, they’ll be viewed as “calendar reset” moment: Before Shift and After Shift. We’re already seeing leading indicators — Walmart’s commitment to sustainability, GE’s move to Boston, Publicis’s rewritten purpose statement and organizational structure — but in the next year or two, the pace will quicken. New CEOs at category-leading companies like McDonald’s, Ford, and P&G will most likely announce stunning new initiatives that would have been inconceivable a decade ago. 9. The best NewCos realize there’s a lot to learn from the BigCos. After years of feasting on BigCo markets, “established upstarts” like Google, Facebook, Uber, Zenefits, and Square are transitioning from cultures based on “move fast and break things” and “ask for forgiveness, not permission.” Their leaders are now turning to questions like “How do I build a company that will last for generations? How can I maintain a strong corporate culture when I have thousands of employees? How do I work productively with regulatory and policy frameworks, now that I’m an established player?” Turns out, BigCos have decades, if not centuries, of experience in answering these kinds of questions. In my conversations with leaders of both NewCos and BigCos, I sense a new kind of detente as each side realizes how much it has to learn from the other. In the coming months and years, I expect we’ll see a lot more cooperation between the two. In the coming months, NewCo will be focused on exploring these business trends, with new media and event products. If you’d like to join the conversation, please follow us on Facebook or Twitter, hit “Like” below, and/or sign up for our daily newsletter. We believe this the most important story in business, and we’re committed to covering it for you.

|

|

Scooped by

Linda Holroyd

February 10, 2016 10:00 AM

|

After a long list of mergers and acquisitions in healthcare, what does Shire’s acquisition of Baxalta mean for the industry?

Research suggests approximately 95% of the estimated 6,000+ rare diseases are yet to have a single FDA-approved drug treatment. However, this could be a thing of the past, going by the current trends in the market.

The acquisition of Baxalta by Shire being a case in point, following the trodden path of the Sanofi-Genzyme and the Roche-Genentech deals. With this successful acquisition, Shire is moving to consolidate its position in the orphan drugs market across therapeutic segments ranging from gastroenterology to lysosomal disorders.

Understandably, the orphan drug segment has enjoyed a longer exclusivity status from FDA, with companies spending less on shorter trials with smaller patient populations, along with a provision for a maximum pricing power to the invested pharma company, has made this segment a sweet spot for pharma mergers and acquisitions.

With the minimized patient population available for clinical trials, the market is also open to the adoption of genetic biomarkers and clinical endpoints for orphan drug clinical trials, a major step towards personalized medicine.

The orphan drugs market is very attractive: it’s worth $100+ billion and has a CAGR of 12%, almost twice of the general drugs market. Of the top 10 projected best-selling drugs worldwide in 2015, almost seven bear the orphan status. Additionally, the market has had favorable regulatory environment, having witnessed a record year for FDA/EU/Japan orphan designations in 2014.

Baxalta’s acquisition is very logical, as the company’s assets complement Shire’s rare disease platform, which made up 40% of Shire’s 2014 revenue. Additionally, it follows Shire’s recent portfolio expansion with the purchase of NPS Pharmaceuticals and its drugs for a rare disease, short bowel syndrome.

The combined entity can be shaped as a global leader in rare diseases with multiple billion-dollar franchises in high-value therapeutic areas with substantial barriers to entry. It puts Shire in fourth spot, very close to Celgene and within reach of the market leaders of orphan drug sales, Novartis and Roche. Building a strong diversified portfolio and achieving market leadership is very crucial for Shire to compete in this market, estimated to be worth $180+ billion in 2020!

This acquisition is in line with large platform acquisition activity like Abbvie-Pharmacyclics (2015) Amgen-Onyyx (2013) and Sanofi-Genzyme (2011), and also helps access a lower effective tax rate for the combined entity by 2017-2018.

This piece was written with contribution from Sangeetha Prabakaran, Program Manager and Nitin Naik, Vice President of Global Life Sciences with Frost & Sullivan’s Transformation Health Program.

|

|

Scooped by

Linda Holroyd

February 8, 2016 1:23 PM

|

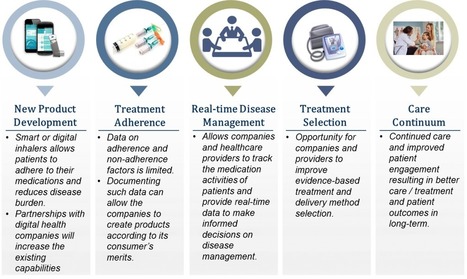

The Internet Of Medical Things: Digitization Revolutionizes Respiratory Care Management

During this time of year, incidences of severe chronic obstructive pulmonary disease (COPD) escalate. Today there are 60 million people with moderate to severe COPD and an additional 235 million who live with asthma worldwide. The total direct costs associated with COPD were approximately $40 billion in 2015 and are estimated to reach $49 billion by 2020. The economic burden of COPD and asthma in the European Union was estimated to be more than 80 billion euros in 2013.

Adherence is the biggest challenge with any chronic disease, especially COPD. According to World Health Organization (WHO), the rate of non-adherence varies from 30% to 70% for asthmatic patients. Hence, there is a need to prioritize the role of patient adherence in improving patient outcomes and reducing the associated costs.

The transformation of the healthcare industry toward a patient-centric model, coupled with the rise of digital health, is set to transform respiratory care management. Many pharmaceutical companies are revitalizing their capabilities and operative models through digital health technologies and are transforming themselves toward prevention, precision, personalization, consumer engagement and improved patient outcomes to remain competitive.

The Big Pull: Next-Generation Inhalers

Next-generation inhalers, often known as smart inhalers, are rapidly emerging as the key focus area for pharmaceutical companies. These devices enable patients and healthcare entities to access data in real time and utilize the data to improve the treatment outcomes using digital technology. Leading pharmaceutical companies such as AstraZeneca, Novartis, Boehringer Ingelheim and GlaxoSmithKline (GSK) already recognize the role of digital health in connecting to the patients and improving medication adherence.

In July 2015, AstraZeneca partnered with a New Zealand-based digital health technology provider, Adherium, to incorporate digital health technology into its products. Adherium’s Smartinhaler products are cleared for marketing by the U.S. FDA and European CE marking, as well as TGA and MedSafe in Australia and New Zealand. Furthermore, the company is in the process of CFDA registration in China.

Another U.S. based, FDA-approved digital health technology provider, Propeller health, entered into a partnership with Boehringer Ingelheim and GSK for their inhaler device to enhance product value by improving patient adherence and gathering insight on patients, and thereby personalizing treatment for its consumers. Propeller health received FDA approval for its system to be used in association with Boehringer Ingelheim’s Respimat device and GSK’s Diskus device.

Additionally, Novartis entered into a partnership with QualComm to incorporate digital technologies in its COPD device, Breezhaler, in January 2016.

What Does this Mean for Patients and Providers?

The new products enable patients to adhere to their medication by continuous reminder and dosage information. Patients receive alerts through their mobile or electronic devices as a part of the adherence program. The information empowers healthcare providers and companies to monitor patients as well as make informed decisions on choice of treatment and medication changes. Evaluating the patient information allows companies and providers to quantify the factors on medication adherence and better understand the patient to improve the quality of healthcare.

The drive toward integration or a connected healthcare environment will rapidly change the clinical workflow of physicians and providers. As consumer engagement and data increases, physicians will need to enhance their skills and tools to interpret the results as well as broaden their consultations with patients to support them more often in their choice of treatment. Patients will become more empowered to make decisions for themselves based on the data generated from digital inhalers.

Eventually, the goal with digitization is to increase adherence, reduce costs and improve quality of life. Digital health is not only transforming patient care, but also allows companies to innovate and create opportunities.

The impact of digitization of healthcare is clearly visible in the respiratory care management segment as pharmaceutical companies are developing a collaborative culture in embracing digital technology. Digitization allows pharmaceutical companies to gather patient data, connect with patients and providers to make informed decisions, and continue to innovate ideas needed to stay ahead of the competition. For companies, the next five to 10 years will be essential as they manage the data from patients and incorporate this into the physician’s workflow.

This article was written with contribution from Brahadeesh Chandrasekaran, Industry Analyst with Frost & Sullivan’s Transformation Health Program.

|

|

Scooped by

Linda Holroyd

January 26, 2016 5:24 PM

|

How private-equity owners lean into turnarounds

PE-backed companies outperform their public counterparts during periods of distress because the owners play a more active role in management.

January 2016 | byHyder Kazimi and Tao Tan

It’s well known that the boards of the best private-equity (PE) firms create value by using financial leverage to increase their returns on equity, by improving the strategy and operations of their target companies, and by exiting at higher multiples. Proponents of PE further argue that management incentives, strong board governance, and a concentrated shareholder base are critical for long-term success.

Struck by recent difficulties in sectors such as oil and gas (not to mention mining) in the wake of collapsing commodity prices, we decided to find out whether more disciplined PE practices can make a difference during troubled economic times. To that end, we compared the performance of 659 PE-backed and publicly owned enterprises across different sectors over the last nine years. Our finding: PE-backed companies outperformed their public peers when recovering from business distress, even taking into account a higher risk of bankruptcy.

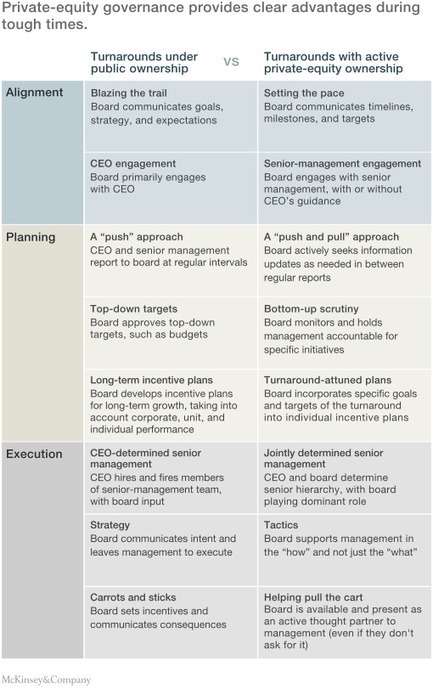

Exhibit 1 shows that PE-backed companies with more than $250 million in revenue at the time they got into trouble recovered their EBITDA margins significantly faster than their public counterparts did for the turnaround’s duration—typically, up to 18 months. On average, they succeeded in recovering their pre-distress margins during that period, regardless of their size.1

PE ownership does provide some natural advantages over public ownership. Our recent experience working with both types of companies during episodes of economic pressure indicates that the key differences are the active role PE boards play in setting the ground rules and their willingness to hold management teams accountable for driving a turnaround. We have found, for example, that the most successful PE-backed company boards quickly and significantly change the rules of engagement, clearly communicate specific performance targets, set an explicit timetable for action, and decide whether the CEO and management team have the mind-set and capabilities required to execute the plans (Exhibit 2). These successful PE boards, we have found, are also very effective in shifting their behavior from normal-working mode to crisis mode as planning moves into execution.

Not all company boards must follow these prescriptions. Some may lack the time to do so; others have incentives different from those of PE directors. Nonetheless, we believe that the boards and leadership teams of public companies can learn from the energy, urgency, and hands-on involvement of rapid owner-assisted transformations. PE governance provides clear advantages during tough times, as well as the less tangible benefits of active board leadership and direct owner accountability. These can truly change the game.

|

|

Scooped by

Linda Holroyd

January 4, 2016 12:55 PM

|

Tesla is at the forefront of the electric car industry, however, Michigan automakers are quickly jumping on board on the electronic movement with partnerships with Silicon Valley businesses.By Rick Haglund

LOS ANGELES — You can go to the mall on a Sunday afternoon to buy a pair of shoes in Southern California and come home with a Tesla Model S electric car.

That is, if you can afford the $76,200 selling price.

Tesla sells directly to consumers in California and about 20 other states. Michigan isn't one of them. Our state requires new cars and trucks be sold through franchised dealers, a system Tesla is fighting to upend.

But the long-held dealer franchise system isn't the only part of the auto industry California companies are seeking to disrupt.

California is competing, and in some cases, partnering with Michigan companies to transform the automobile from a mechanical to an electronic marvel.

Ford Motor Co. and other automakers and suppliers have established research operations in Northern California's Silicon Valley to develop various automotive software technologies.

Dragos Maciuca, the director of Ford's new California operation, recently told the Los Angeles Times that Ford is there because of a profound shift away from mechanical engineering — Detroit's forte — in the auto industry.

"Now, there is the shift to software — and the mecca of software is Silicon Valley," said Maciuca, a former Apple engineer.

Ford and Google, which has been testing self-driving cars for years, are rumored to be in talks to jointly build an autonomous vehicle.

This isn't the first time Detroit has come to California seeking new knowledge about the auto industry.

California, the largest auto market in the country, long has been a social and style trendsetter. The hot-rod culture that developed here after World War II, for example, influenced cars from Detroit for decades.

In the 1980s, General Motors jointly operated an assembly plant with Toyota in Fremont, California, that GM used to learn about Toyota's manufacturing techniques.

The plant, known as NUMMI, closed in 2010. Tesla now owns it.

California's auto industry is not a threat to Michigan's in terms of size. Michigan dwarfs California in auto employment, manufacturing plants and engineering centers.

California companies often rely on Michigan businesses when they get ready to build products.

Roush Industries in Livonia is building Google's test fleet of self-driving cars. Last year, Tesla purchased Riviera Tool in Grand Rapids for its metal-bending expertise.

But Michigan's auto supremacy isn't assured just because state automakers have been designing, engineering and building cars for more than 100 years.

Crain's Detroit Business recently asked retired Visteon CEO Tim Leuliette what advice he would give new executives in the auto industry.

"Face reality," he said. "Don't work for a company that makes mechanical parts in an electronic world."

That should send shivers down the spines of those working to ensure Michigan's automotive future.

|

|

Scooped by

Linda Holroyd

November 24, 2015 1:26 PM

|

Why do start-ups routinely outperform incumbents when it comes to catching the next wave in disrupted markets? Because they are not conflicted! So what would happen if the established leaders could sort out their internal (and external) conflicts? What if they could organize in a way that let them leverage their size and use it to their advantage? What if an aging gorilla could become Godzilla? That is the outcome Zone to Win seeks to enable—to help established enterprises organize to compete in an age of disruption. Its key principles include the following: - The resource allocation conflicts that paralyze established enterprises derive from competing ROI time horizons. To resolve them companies must organize into zones defined by which horizon is being targeted.

- Three of the four required zones are typically already in place and function reasonably well—although they could do better. These are the Performance Zone, the Productivity Zone, and the Incubation Zone.

- The fourth zone by contrast, the one that enables an established enterprise to onboard a disruptive business model and scale it to material size, is typically neither organized nor funded to succeed. This is the Transformation Zone, and it requires a very specific set of disciplines if its transformational goals are to be achieved.

- Transformational initiatives put enormous pressure on each of the other three zones, so in fact the entire enterprise must reorganize and reprioritize across all four zones in order to succeed.

- Finally, such transformations can be entered into voluntarily in an effort to catch the next wave ahead of the competition—what we call playing Zone Offense, the case study for which is Salesforce.com—or reactively in an effort to keep the next wave from catching you—what we call playing Zone Defense, for which the case study is Microsoft.

Zone to Win overall is a playbook. It is highly prescriptive and pulls no punches. Its BHAG is indeed big, hairy, and audacious—namely, to reengineer conventional management principles to compete successfully in an age of disruption. If this is something you would like to learn more about, please click here. One last note: Initial versions of each of the chapters in Zone to Win were test driven early this year in this blog, and it was my pleasure to give a shout out in the Acknowledgments section to those readers whose comments made a material change to the book’s argument. Thanks again to all who participated.

|

|

Scooped by

Linda Holroyd

October 22, 2015 11:07 AM

|

Search giant Google today is taking the next step in its bid to rehabilitate its relationship with the news and publishing industry.

In Europe today, the company is opening up applications for startups and others who are interested in receiving grants from Google’s Digital News Initiative Innovation Fund: Google has put aside €150 million ($170 million) for startups and others building new services, products and technologies for the news industry, and it will give out in grants twice a year, typically ranging from €50,000 to €1 million, but occasionally higher, with no strings attached, Google said today:

“We’re looking for projects that demonstrate new thinking in the practice of digital journalism; that support the development of new business models, or maybe even change the way users consume digital news,” writes Ludovic Blecher of Google, who heads the DNI Innovation Fund. “Projects can be highly experimental, but must have well-defined goals and have a significant digital component. There is no requirement to use any Google products. Successful projects will show innovation and have a positive impact on the production of original digital journalism and on the future sustainability of the news business.”

At the same time, Google said that it now has over 120 news organizations in its Digital News Initiative, the European umbrella group for the fund, which was first announced in April with 11 members and a pledge to work on projects and products focused on high quality journalism. It includes publishers like Die Zeit, FAZ and Der Spiegel, the Guardian, Financial Times, the BBC, The Economist, La Stampa, El Pais and Les Echos.

Since then, the DNI has been working on training by way of projects like the Google News Lab. And some of the work that the DNI has been running and funding also formed a cornerstone of Google’s recently announced AMP (accelerated mobile pages) project, tech that Google has developed to produce faster-loading sites for smaller screens.

The €150 million fund was actually first made public in April, but now, as part of the application process opening up, Google is laying out more details about how it will work, who is eligible and more.

Grants will be open to any individual or organization working on innovations in online news — and that can range from startups through to established news publishers. Google says that application rounds each year with the first starting today and closing December 4. (The next will be in Spring 2016.)

Google says that funding will fall into three categories:

Prototype projects that need up to €50,000 of funding. “These projects should be very early stage, with ideas yet to be designed and assumptions yet to be tested. We will fast-track such projects and will fund 100% of the total cost,” Google says.

Medium projects that need up to €300,000 of funding. “We will accept funding requests up to 70% of the total cost of the project,” it notes.

Large projects open to organisations that need more than €300,000. “We will accept funding requests up to 70% of the total cost of the project. Funding is capped at €1 million,” says Google.

There may be exceptions to the €1 million cap, Google says. All of this is irrespective of whatever other funding a company or person may get for the work in question. That means you may also be getting VC backing. Google does not take any equity as a result of the DNI grant.

Google is, in general, making quite some effort here to make sure that it’s as unbiased as it can be when considering and awarding grants.

Google says it has “consulted widely to ensure that the Fund has inclusive and transparent application and selection processes. Confidentiality is critical; applicants should not share business-sensitive or highly confidential information.”

It adds that initial selection for the first two tiers of projects will be done by a Project team, which will be a mix of Google staff and external industry figures. Then the Fund’s Council (12 people currently, listed below) will review and decide further. The Council will both sift and decide on the “Large” projects.

While there are a number of ways of getting funding for startups today — indeed we’re in something of a high water mark for VC funding more generally — the idea here is to try to give some oxygen to projects in the lesser-explored corners of Europe and the wider ecosystem. At a time when there is a huge emphasis on the news industry dying, this might be a ripe moment to step in and offer a little lifeline in the form of some money for new ideas.

Google has come under fire for having a fractious relationship with the news industry, with many publishers criticising the search giant and its own content efforts for effectively making it too easy to bypass their own sites (and business models) to provide consumers with news. Some have held out against Google while others have caved in somewhat reluctantly to a company that essentially dominates how people navigate to information on the Internet today.

But Google has had a lot of heat both in terms of bad publicity for being a giant bully, and from regulators, and it is now looking for a more conciliatory approach, one perhaps less evil.

|

|

|

Scooped by

Linda Holroyd

March 16, 2016 11:52 AM

|