Your new post is loading...

Your new post is loading...

|

Scooped by

Linda Holroyd

August 25, 2016 11:28 AM

|

Software, content, and just about everything else you see online today has been designed for the masses. Apple builds one Mail app for millions of people to use; EA expects a wide swath of people to enjoy the video games it creates; journalists write news stories intended for mass consumption. And this makes sense; it’s how most products are made these days. After all, it’s not feasible to craft a custom offering for every individual, right? In fact, we’re just barely scratching the surface of personalized products. A/B testing and variants let us target increasingly granular demographics with the content most likely to convert them, but this isn’t true personalization — at least, not yet. But what if every piece of software, every article, and every video strived to be what each person wanted it to be? It’s already happening in journalism, e-commerce, financial services, and business intelligence. In fact, a pioneering automation company in the Research Triangle of North Carolina called Automated Insights is working on just that. Robbie Allen, its founder and CEO, claims the company is the largest content producer in the world, having written more than 1 billion articles in 2014 alone. “We flip the traditional content creation model on its head,” he says. “Instead of one story with a million page views, we’ll have a million stories with one page view each.” The same is coming to video games and other software. One day, we’ll have applications that can adapt themselves to each user’s needs. Automation and AI will make this a reality, and the game will change not only for consumers, but also for entrepreneurs. What the Future of Automation Means for Startups There’s a reason companies like Atlassian, for instance, focus on project management for developers and don’t branch out to project management for construction or financial services: If you go after too broad a market, someone will build a more specific — and more personalized — system that better serves the needs of your niche. This is how markets fragment, and it’s why businesses are advised to target one very specific part of their market. Going forward, though, you should expect to be able to target individual people and companies using automated development systems that can tailor a piece of software to fulfill a customer’s precise need. Targeting usually takes place at the marketing level, but you’ll soon see that moving to the product development level as well — when software products become able to self-modify in order to better suit individual users. Automated capabilities will affect hardware, too. Standby Screw, a custom parts manufacturer in Ohio, is already reaping the benefits of having intelligent machines perform custom operations that originally took hours of manpower. The company uses Baxter, a Rethink Robotics’ product, to perform a variety of tasks — even repositioning parts bumped out of place — without having to stop or be reprogrammed. Baxter has freed up valuable time for employees to do tasks that require more creative intelligence and has cut down on the production time needed to build custom parts and packaging. In the future, enhancing customization will be the bare minimum for companies looking to remain competitive — startups, and even larger businesses, will have to differentiate themselves through other means, such as price and customer service. What this means for entrepreneurs is that the barrier to entry will be considerably lower: Fewer employees will be needed to complete increasingly complex tasks, rendering startup costs, even for manufacturing, relatively negligible. How to Prepare for a Brave New Personalized World So how do existing tech companies prepare for this future of ultrapersonalization? What’s the best way to stay on the cutting edge of the automation revolution? Here are three ways to stay on top of the customization game: - Don’t be late to the party. Begin looking at ways to adopt automation and personalization technologies as soon as you possibly can, including partnering with other companies and products that can help you get to that next level. Mercedes, for instance, has taken advantage of Nest’s developer program, and its cars can now let your smart thermostat know what time you’ll be home. Nest can get your home to the optimal temperature before you pull into the driveway.

Lest you think only tech companies in Silicon Valley need to worry about this issue, a recent survey found 60 percent of businesses across a variety of industries are already seeing returns on their investments in personalization tools. Nearly every industry will be deeply affected by this movement toward greater personalization — to remain competitive, it’s best to prepare now, regardless of your area of expertise. - Expect the rules to change. The hard and fast rules of the startup world (i.e., find a specific target market, build one product that works for that group, and market it accordingly) are going to change. A core product that’s good at accounting, project management, or payroll, for example, could adapt and personalize itself to fit the needs of a broad range of individual prospective users.

In the near future, many businesses will allow each consumer to customize, and in some cases, design his or her own product from scratch — even if it’s digital. Something as mundane as breakfast cereal is already being hyperpersonalized: Muesli now allows you to create your own mix on its website. Creating something that’s perfect for just a percentage of the population is no longer a requirement; automation and AI will allow you to paint with broad strokes. - Implement automation in product testing. Thanks to automation, the timeline of going from idea to implementation will be dramatically decreased.

Many companies that have shifted from a completely manual testing process to a hybrid of automated and human testing are already seeing efficiency improvements in product development. The shortened time frames that result would be a huge boon to startups, which are more often than not limited on time and resources. A future where nearly every product and service is customized to fit the individual is closer than you might think. By preparing for this future and incorporating automation wherever possible, entrepreneurs and existing startups can ensure that they remain one step ahead of the competition.

|

|

Scooped by

Linda Holroyd

July 22, 2016 10:44 AM

|

Why Leaders Need to Know What Machines Can't Do

by Geoff Colvin @geoffcolvin JUNE 20, 2016

Some jobs really must be automated; others need the human touch.

When stock markets plunged early this year, managers at USAA’s investments division noticed something odd. Customers who routinely conducted business online were suddenly lighting up the phones. USAA had nothing new to tell them—its fundamental advice hadn’t changed, and they could have found that guidance online. Yet clients deeply wanted to talk to a real human being, and never mind why. They just did.

That reality illustrates a high-stakes decision that confronts managers in every industry: choosing which employees must be replaced by technology and which must not be. Growing numbers of jobs at every level can be performed by machines—not just faster and more cheaply than humans can do them, but better. In many of those jobs, such as in factories, failing to replace people could doom a company through uncompetitive costs. Yet in other jobs that machines can do well, such as giving financial advice, replacing too many humans could be a fatal error. How to decide? Three situations in particular seem to justify the costs, and quirks, of people.

When customers value the human touch. Many decisions that in theory are calculable—where to invest, whether to sue, how to respond to a medical diagnosis—are in fact laden with emotion. Many people need to interact with a person before choosing a course of action. In finance, law, medicine, and other fields, workers who handle those interactions most adeptly will be the least susceptible to replacement.

When constituencies must be represented. All organizations are run ultimately by and for humans, and most are complex matrices of desires, incentives, budgets, and myriad other factors. If marketing can’t get along with sales, or management with labor, nothing good can happen. Technology could optimize the whole intricate machine, but it will seize up if humans can’t agree on how to make it go.

When someone must be accountable. So long as humans and not machines are in charge—let’s assume that’s a long time—societies will demand that people be made to answer for decisions, even if technology recommends those decisions. Government officials, military officers, judges, business managers, basketball coaches, and others in leadership roles will remain where the buck stops. Technology may reduce the number of people in such roles—it’s already taking over tasks of middle managers, for example—but responsibility will ultimately end up in human hands.

As machines grow more powerful, deciding who must go and who must stay becomes harder. A guiding principle: Just because technology can do a job brilliantly doesn’t mean that it should.

|

|

Scooped by

Linda Holroyd

July 5, 2016 2:35 PM

|

Combine velocity and volatility with the 24/7 global business cycles and it becomes virtually impossible for any leader to stay on top of his or her game. For Chief Marketing Officers (CMOs), staying on top can spell the difference between success and failure, for them as well as their companies. Marketo funded a qualitative study looking into emerging marketing trends. A wide range B2B and B2B2C Chief Marketing Officers (CMOs) participated, representing companies ranging in size from the Fortune 10 to early stage start-ups across financial services, manufacturing, high technology and SaaS industries. Only 24 Hours in the Day

A common refrain heard in the study were the challenges of juggling multiple demands on time, while trying to keep up to date. Andy, a CMO of a Fortune 15 healthcare services company summed it up well, “I have internal goals to meet and pressures to address that are not based on best practices or what is happening in the marketing discipline. Seventy percent of my time is spent on internal constituents.”

And when the question of travel came up, CMOs said they needed to define priorities.

Andy shared a sentiment that was echoed by most CMOs, “Conferences don’t do it for me; networking with peers is more useful. But it needs to be local.” Katy, another study participant is the CMO with a high profile Fortune 1000 social technology vendor, shared, “When I’m out of town or at conferences, I’m with customers. They are my priority.” CMOs want to network with peers, but LinkedIn Groups, exclusive meetups, CMO-only conferences and CMO tracks at conferences offer little perceived value and require valuable time out of office. If they have to travel, CMOs opt to meet with prospects and customers before sitting in a conference or dinner meeting, regardless of how prestigious the group is. When do CMOs find time to read from the daily deluge of posts and articles available? They don't. Not from lack of interest or motivation, but from a lack of time. Just as customers are overwhelmed and fatigued by the constant bombardment of information, so too is the CMO. CMOs regularly scan a handful of publications including Fast Company, Harvard Business Review, Wall Street Journal, Forbes and McKinsey reports. The topics of interest vary based on the issues facing them and the company. Andy summed it up with “if a topic peaks my interest, I’ll read more.” 4 Strategies, 1 Secret

CMOs employ 4 strategies to stay on top: 1. Routinely visit customers to understand market shifts and new expectations.

2. Network with a handful of trusted peers by scheduling periodic calls or meet ups.

3. Stay in touch with trusted consultants and influencers.

4. Hire right.

The CMOs who succeed at staying current share a common secret: they rely heavily on their teams. “I’m constantly blasted with ideas from my team and they educate me,” shared Katy. “I’m very focused on hiring a good team and giving them room to grow and experiment.” By adding new roles — many of which didn't exist five years ago — CMOs are rapidly evolving their teams’ competency portfolio: - Social engagement and community managers

- Chief content officer, evangelists, editors, chief listener, chief storyteller

- Data scientist, marketing operations, business analyst, center of excellence managers

- Chief customer officers, customer experience analysts, customer marketing specialist, employee engagement strategist

- Digital/growth acquisition, digital experience marketers, lifecycle marketers, marketing technologist

Hiring the right candidate is challenging, regardless of company size or industry. It's difficult to find the right person out of a large candidate pool who fits the culture, offers the right expertise and is interested in joining the company. Marketing leaders of large and small companies resort to hiring from their network. The candidate quality is higher and frequently a better fit. Larger, established companies face an additional obstacle of not being considered ‘hot’ enough. This reduces the pool of candidates substantially for key positions in analytics, data science, modeling and digital marketing. Millennials — who make up the majority of the candidates — feel that large or mature companies would restrict their creativity, mobility, opportunities and need for flexibility. To keep competitive, established company CMOs evolve their culture, structures and spend a lot of time selling their vision of the company. CMOs with brand cache companies have the reverse problem: retention. Their employees are constantly being recruited away with lucrative offers, creating in one case 20 percent annual turnover. These CMOs retain top talent by regularly moving people between roles and increasingly offering high performers more latitude, responsibility and opportunities to do new things. One irony in this growing reliance on teams is that anyone seeking to woo the CMO as their ideal target buyer, need to redirect the marketing and sales strategy to win the hearts and minds of their subordinates. Building the Business Case for Marketing Hires

Any discussion of adding headcount brings with it the age old conundrum of how to justify hires in environments where the business case is based on revenue ROI. Unfortunately many of the new marketing competencies required to build awareness, reach, engagement, credibility and loyalty in this "age of the customer" are either indirectly linked or are too new for anyone to have hard data on their impact on quantifiable revenue. CMOs cited two strategies on how to justify new hires: 1. Contract with candidates to complete a high visibility project

Engage the candidate as a contractor for a project that has high visibility with key constituents and let the value-add and impact of the project’s results "sell themselves." This approach is effective for some positions such as videographer, sales enablement, field marketing/ops and digital branding, but doesn't apply to all positions. 2. Redefine traditional roles with new competencies

Reduce traditional marketing headcount in print advertisement, etc. and repurpose them for new competencies. This approach is used to bring in data scientists, social managers and digital branding where the link to revenue is not directly measurable. CMOs are building networks made of employees, contractors, Martech vendor specialists and influencers to gain the agility that companies. Clark, a CMO with a Fortune 1000 SaaS Financial Software provider, values this approach as it “enables me to have continuous access to the best and brightest while easily adjusting the mix in response to market and business changes.” The CMOs who stay on top of their game know, this is no one person job. Creative Commons Creative Commons Attribution 2.0 Generic License Title image by garryknight

About the Author

With more than 25 years of marketing and leadership experience, Christine Crandell, President at New Business Strategies, is a recognized thought leader, expert, practitioner, speaker and author regarding corporate strategy and customer experience. Christine’s Forbes blog, “Outside the Box” focuses on helping the C-Suite understandhow to drive faster revenue growth through innovative business strategy, practices and models.

|

|

Scooped by

Linda Holroyd

June 28, 2016 4:33 PM

|

Here are some cold, hard social media truths: likes, follows, shares and hashtags aren’t communities. The newsfeed is little more than a way to consume news and maintain relationships with people you already know. Hashtags are often ineffective.

As much as we love it, social media doesn’t make it easy to build new communities around a shared identity or interest. Legacy products such as Facebook Groups and the like only scratch the surface of what’s possible in a digital world where three billion people are connected by supercomputers in their pockets.

When software’s never been smarter nor have we been more connected, the lengths we ask people to go to in order to meet new people around the things that matter most to them are absurd. To many, a web forum is still held up as state-of-the-art. To truly harness the power of social networking, we need to think beyond views, likes, follows and hashtags.

My A-Ha Moment

Most of my professional career has centered on creating software platforms dedicated to building communities. And by communities, I mean networks that build real, tangible relationships between people who share an identity or interest, whether it be a profession, medical diagnosis, political candidate, sports team, social cause or subculture.

Back in 2007 I launched Ning, a platform for niche networks on the web. From the moment we offered “your own social network for anything,” I saw the excitement of pez collectors, teachers, Brooklyn artists, Dallas Mavericks fans, DIY Drone enthusiasts and Offbeat Brides connecting for the first time live in their own communities.

I was hooked.

I loved that people could create networks around anything that mattered to them, no matter where they lived, what they looked like, how popular or unpopular they were in the real world or how much money they made. These were communities created around strong identities and interests. But as social networks evolved, the world naturally and collectively gravitated to more familiar connections. As more people joined networks and connected to high school friends, extended family, college classmates and professional colleagues, the people we already knew started to consume the majority of our time online.

Since 2007, a few things have changed. I left Ning and started Mightybell to create a new generation of mobile-centric identity networks. Maxed out with connections to people we know, I believe we are at an inflection point where the social-networking world is ready to connect and build new relationships in smarter, more natural ways with new people who share a common identity or interest.

Don’t hashtags bring together people around interests? The most popular hashtag movements aggregate people’s perspectives in one place. They are fantastic at demonstrating energy around an idea, but they are missing the opportunity to build towards concentrated, sustained action, support, learning and real relationships. It’s not for lack of organizing savvy by leaders. It’s the limitations of the software. We can do better than platforms that require a convoluted combination of hashtags and poorly organized numbers for questions and answers to “have a conversation.” No one should have to work this hard to chat.

The difference between real community building and the current state of “communities” built on the dominant networks is evident in this comment from a member of Beyond Type 1’s new network dedicated to navigating Type 1 diabetes:

For people trying to connect with those who share their identity or interest, sifting through junk to get to something valuable is simply wasting time. That an app dedicated to building relationships between people navigating Type 1 Diabetes didn’t already exist was a missed opportunity that Beyond Type 1 is filling.

In this new, more effective definition of what it means to create a community, likes, follows, shares and hashtags are the means to attract members, and these new identity networks are the end, offering the opportunity to bring together a coalition of the motivated to build strong relationships with each other, not just with you.

For brands with a passionate customer base, advocacy organizations, not-for-profits, authors, influencers and anyone with the desire to build a community, these identity networks create a powerful engine of sustained action and durable relationships that outlast any individual campaign, book or hashtag.

A New Way to Think About Engagement

If you are not coupling views, likes, follows and shares with a destination, you’re missing the opportunity to craft a powerful network of your most motivated fans and followers.

This isn’t throwing people together in an empty channel or forum online. Imagine a new world where the network plays the role of a host. A new member joins an identity network like Beyond Type 1 for those touched by Type 1 diabetes or OWN IT for small business owners and is instantly connected to those members near them in real life, those members who share the same specialty and those members who share an interest in the same topics.

As this same new member shares more about their interests, their feed becomes more personalized and they see the most popular and highest quality conversations happening in the topics they care about. The most relevant members are not only surfaced by location, profession or stage, but can also message similar members based on how they answer polls, which live chats they attend or the groups they opt-into within the network.

Organizing and connecting your community more deeply in the same place also removes the friction and arduous work currently needed to connect the right people to each other or organize events. Imagine tapping the most active members in a particular geography to host a meetup. An identity network already knows which members are in the same location and can take care of inviting, managing replies and – through APIs – can even suggest a venue without requiring the network host to lift a finger.

With these new models (and the powerful technology behind them), we can finally retire the simple, chronological group comment thread, event page or chat room paradigms created when we accessed the internet from a dial-up connection. Facebook Groups will remain for small groups and Meetup will still be there for local groups not connected to a larger network, but when you want to build an army, the savviest leaders will turn to the organizing power of identity networks to build stronger, deeper relationships at scale.

A Better Way to Create a Community

The key to translating your likes, follows and shares from a hashtag to an identity network is reframing your definition of success from big numbers alone to one that includes, at its core, a more deeply engaged community of your most motivated fans or followers. Once you wrap your mind around this, the mechanics of growing an identity network are straightforward:

It’s about them, not you. If you want to build real connections and sustained engagement between members, share the spotlight. At Mightybell, as we’ve introduced new features like polls, questions and groups, we’ve seen the percentage of contributing members double across our roughly 50,000 networks. More contributing members trigger more interesting and diverse notifications that bring more members back frequently. Then, as more of your members engage in the network, you as the host can step back and see a self-organizing community emerge.

Encourage members to share ideas, stories and experiences, not advice. The one thing dead communities have in common? Advice. It’s not inviting as a reason to join a new network. Much more inviting are similar people sharing their practical ideas, stories, experiences and current dilemmas with each other in a convenient mobile app. Create the conditions for sharing stories and practical ideas, and your network will become more valuable almost immediately.

Choose icebreakers over listicles. The biggest mistake we see over and over again is a host repurposing generic “content” they’ve created for content marketing. The sad truth is that a listicle built to drive sharing on LinkedIn doesn’t spark conversation among new members in a community. Rather, we’ve seen dramatically better results with a portfolio of conversation starters – or “engagement strategies” – that seek to offer members multiple ways of contributing to and participating in the network.

In addition to things like multiple choice polls, live chats, hangouts and meetups, the best engagement strategies include introductions, topics, hot or cold polls, percentage polls, questions and prompts. Think about them as a portfolio to use in rotation to bring in more members to contribute and share their stories. As we use these today, we regularly see over 50% of members contributing to an identity network. That’s a far cry from the accepted rule that says only 1% of people contribute to networks while the rest of us consume.

Likes, shares, views, hashtags and follows are no way to organize in a live, social and mobile-first world. Given the intelligence of software and the sophistication of algorithms, they are downright pedestrian. To build powerful, effective, sustained communities, we need to think beyond them. Identity networks are already unlocking new connections across the three billion-strong graph of humans on mobile. The technology is here. The only thing you need is to know who you’re going to bring together.

|

|

Scooped by

Linda Holroyd

June 14, 2016 1:35 PM

|

JUNE 11, 2016

Our M&A Wish List

Here are the types of companies CB Insights is interested in acquiring.

By Anand Sanwal (@asanwal), CEO / Co-founder / Customer Service

In the last 6 months, we’ve looked at 3 acquisitions. Two of them came to us and one we sought out. Unfortunately, none of them worked out for various reasons. Some deals died quickly and some at the diligence stage, but through these 3 experiences, we’ve learned a lot about what we want and what type of acquisitions makes sense for us.

So we decided to do something atypical and publish a list of the types of things we’d like to acquire and why. It offers some visibility into our playbook so we were a bit reticent to do this for fear of competitors copying us. We then read a great quote by Jeff Bezos which changed our mind.

“If we can keep our competitors focused on us while we stay focused on the customer, ultimately we’ll turn out all right.”

So with that bit of angst/preamble out of the way, here are the types of things we’re looking to acquire as of June 2016. We will add to this over time.

Acquisition interest #1 - Vertical media / niche B2B media

When we boil down what has worked for us, it comes down to two things:

We have an amazing research team that develops content that generates a lot of interest in CB Insights

That research gets people to try out an amazing product (sign up for a free trial)

Recently, we’ve been going from a more general research strategy to one that is more industry or vertical specific. The results have been amazing for us. We started with insurance tech, then launched auto tech and have several others in the works.

Each of these verticals has their own newsletters with thousands of subscribers that, in very short order, include senior executives from all the big players in both industries. And they are helping us grow quickly.

But building these verticals up takes time.

As a result, we are interested in getting there quicker by acquiring vertical media sites which are focused on a very specific industry or topic and whose readership is largely B2B. For vertical media sites, we are looking for a few things:

The site should be covering technology or emerging industry trends within the space

A team with deep domain expertise and intense passion for the space

A highly engaged readership. The readership need not be big (although that is of course nice), but the content/research must be great.

If this resembles you, we’d love to hear from you.

Of course, a fair question you should probably ask yourself is “Why would CB Insights be a good home for us?”

Here is what we bring to the table.

A better way to monetize – Most vertical media are reliant on advertising or events revenue as their primary sources of revenue. Of course, many are also doing native advertising and paid reports. We offer a better way to monetize a B2B audience through subscriptions to CB Insights. These subscriptions start at $20k and increasingly are in the six-figures per annum with extremely high annual retention. Our only “ads” are what can be thought of as ‘house ads’, i.e. they are suggestions to sign up for the CB Insights platform. You’ll see examples of these house ads to the right of this post or at the bottom which encourage you to sign up for a free trial. An example is below.

The reality is that there is massive gap between how we can monetize 10,000 or 100,000 readers on thoughtful content/research with our subscriptions than what traditional ad units can offer. This arbitrage is big and offers you a much better way to monetize.

The ability to focus on your content – Because we can monetize content better, it will allow you to focus on what you do best – great research and writing, increasing domain knowledge, building relationships in the industry, etc. You’ll never think about Facebook’s algorithm again.

Our growth team is phenomenal at finding new ways to get increased exposure on content via newsletters, webinars, podcasts, reports, whitepapers and more which we can provide.

In addition, we have data that can open up new types of content opportunities. And with that data comes a team of data scientists, analysts and graphic designers who can help you find new interesting content angles and ways to present that data.

Exposure & influence at highest level – Through the CB Insights newsletter with 167,000+ subscribers (and which is growing by 1300 per week), we reach:

SVP level+ executives at the entire global 5000 including almost 100 publicly traded company CEOs

Partners at every VC firm worth knowing

Journalists at all the leading newspapers and blogs (our press page is testament to this)

Executive of tomorrow’s big companies (yes – those much talked about unicorns)

In other words, we can get your writing in front of people who won’t just read it but who are in a position to use it to make major strategic decisions.

The screenshot below from our press page highlights the number of press mentions our data has received in the world’s most respected publications.

Acquisition interest #2 - Vertical newsletters

While newsletters might often go hand & glove with vertical media categories outlined in #1, we do know of a few newsletter-only companies so wanted to call this out separately. The criteria we look for and the reasons a vertical newsletter would benefit under the CB Insights umbrella are largely the same as for vertical media / niche B2B detailed above.

We will look for a highly engaged readership in these cases and prioritize seniority of readership as much as size. In other words, a newsletter that reaches Chief Strategy Officers and Heads of Strategy with just a few thousand subscribers could be as interesting as a more general tech / industry trend conference which reaches 100k.

Acquisition interest #3 - Proprietary data

We are building software that uses data to predict technology trends. Our customers use insights into tech trends to do a few things:

Predict the next market they should enter

Predict the industries of tomorrow

Predict their next M&A target

Predict competitor strategy and likely moves

Predict their next investment

Predict the S&P 500 of tomorrow

If you have data that you believe is instructive in understanding technology trends, we’d love to talk. A few important things that we look at when evaluating datasets.

Ownership / Chain of custody – You must own the data. Data which is scraped / crawled is fine but it must not be obtained in any way that is in violation of anyone else.

“Supply chain risk” – If the dataset relies on a 3rd party, that is generally less interesting to us. For example, data that derives insights extracted from Twitter or Instagram or Facebook as examples would be less interesting to us as the rules to accessing those platforms can, do and will change.

Hard to get is good – If the data obtained requires digging into PDFs or is extracted from obscure documents or is submitted by organizations directly, we love that. If it’s a dataset available online which is dirty and which you’ve cleaned, this is a good thing.

Applicability – We are interested in datasets that are broadly useful in predicting technology trends and helping with any of the use cases above as well as datasets that are more vertically specific, i.e. data for healthcare or retail or financial services as examples.

Again, a fair question you should probably ask yourself is “Why would CB Insights be a good home for us?”

Here is what we bring to the table.

A software platform to plug your data into - It is straightforward for us to integrate new datasets into CB Insights. The platform was created to be able to do this easily.

A better way to monetize – We’re a premium provider in the market because of the quality of our product and our data. We can very effectively monetize great data.

A research and dataviz team to promote the data – Our ability to tell stories with the data is a distinctive capability of CB Insights. Of course, our newsletter serves as a bullhorn to create awareness of new data as well.

Acquisition interest #4 - Teams

If the idea of using data and probability to predict technology trends is of interest to you, we are interested in hiring teams of 2-8 people with engineering, machine learning and data science backgrounds.

That’s our wishlist for now. As it evolves/changes, we’ll update this post.

If you are part of a company that fits the bill or if you know a company or team that would be a great fit, we’d love to chat.

|

|

Scooped by

Linda Holroyd

June 13, 2016 4:11 PM

|

The stage is set for the coming battle between the big five tech giants: Google, Apple, Facebook, Microsoft, and Amazon (wait, make that four tech giants and one really tech savvy retailer). All are now heavily investing in AI. All now offer personal AI assistants poised to make your life easier.

One of the most recent announcements is from Google. The company launched Google Assistant, which is an integral part of the new Google Home device and Allo (its new messaging app).

Apple is set to announce its additional AI assistant plans mid-June but has already leaked some details. The Information reported that the company is developing its own device for the home and that Siri will open up to third party “apps.” Earlier this Spring, Microsoft and Facebook made their own announcements which put AI Assistants (or in their parlance, chatbots) front and center. And each has a clear vision for how third party bots can exist as part of their platforms.

On the surface, this looks like head to head competition around the AI personal assistant by five of the top tech companies in the U.S.

But what’s really at stake—will we eventually be paying obeisance to Siri or Alexa, while their competitors wither? Is the personal assistant the key to “the era of Artificial Intelligence”?

Here are my five immediate takeaways:

1. The AI Market Segments

One way to view the current setting is to divide what is happening into three distinct market segments (Platform, Service and Software), and you should know which segment any given company plays in to better understand its ambitions

AI Platform

Intelligent Platforms have a set of existing features that you use to build bots (Applications). These include Facebook’s Messenger platform, Microsoft’s Bot Platform (its bots can run on Skype) and all the way up to Amazon’s Echo device, which lets third parties create new skills for Alexa.

Pro: The most dramatic and most important dimension is distribution; these platforms come with easy access to hundreds of millions of users. Almost any programmer can build a bot on the platform, and the time from idea to market is short—think days or weeks.

Con: The most obvious downside is a limited opportunity to innovate outside of what the platform was designed for, which to a large degree consists of the sensors and actuators inside their environments required for the bot to exist, leaving much of the actual intelligence to the developer. And we probably have to accept that the bots are not (yet) true intelligent agents. Platform dependencies put large parts of your destiny in the hands of the platform owner. There’s very limited opportunity to optimize much on output accuracy, and so your product quality (outside of design) depends on the platform. Finally, those users are probably not going to be given to you for free, so expect an App Store like tax.

AI as a Service

These outsourced and on-demand machine learning services allow developers to build models and generate predictions in the cloud, without having to engineer and/or maintain the supporting infrastructure. These include offerings from companies like Amazon Web Services, Microsoft’s Azure and of course Google’s Cloud offerings.

Pro: You can build anything for any platform or channel and move forward pretty rapidly think weeks or months. You do not have to maintain or build your own machine learning infrastructure.

Con: This comes with some sort of recurring cost which might just hurt your unit costs or costs in general. It is likely that some ceiling to accuracy arises given the fixed constraints of the services.

AI Software

You could build your own AI infrastructure from the ground up. Even if you want to do all of this yourself, you’re likely going to end up using either proprietary software and/or open source tools like TensorFlow from Google or say scikit-learn, Theano or Spark’s MLlib. These will help you with the learning aspect of building an AI, much like the services described above, but there’s typically a whole lot more that you’ll still need to build yourself. For example, you’ll need to collect and clean your data, engineer features, evaluate your learned models, serve predictions, incorporate changes to your system and so on.

Pro: This provides the ultimate freedom and allows for very high accuracy in output. True innovation can happen here. It can provide long term cost benefits through infrastructure optimization as well.

Con: This is very time consuming and thus quite expensive as an upfront investment. Anything you build should be thought of as a months- or years-long project.

This is not necessarily a perfect segmentation, but it does provide a good backdrop. And, given that each of the five tech giants is playing in multiple segments, it suggests to me that this is indeed the era of AI. It also suggests that none of the five is immediately convinced that the personal assistant is the only way to dominate in this new era.

2. Cross Device

AI Personal Assistants will be cross device. The recent announcements also point to a scenario in which these assistants will become ubiquitous. Siri is already in your Apple TV, and at the re/code conference, Jeff Bezos announced that Amazon will license Alexa to third parties.

It’s clear that the only way for these behemoths to compete is to make their AI Assistants available across devices. This presents some interesting political challenges right away, as Siri’s and Alexa’s skills converge, Apple would seem pretty uninterested in making Alexa available on your iPhone, for example.

The funny thing is that the player who used to be the most protective about their O/S Platform, Microsoft, has been among the quickest to push its assistant across devices. You can get Cortana on Windows 10, iPhone and Android. I think this willingness could let them leapfrog the others, should they not be as forward-thinking.

3. Horizontal vs. Vertical AI

The structure of the AI Assistant space is now crystal clear: Horizontal AI will integrate with and enable vertical AI. All five companies have built what I like to call horizontal AI, which is to say AI Assistants that operate more as enablers of more focused services (like x.ai).

They’ve also all signaled that they would like third parties to develop these more focused services, just as third parties developed the apps that populate the app store and our smart phones. These are early days, so there are few fully realized vertical AI services in market. (We have built an AI personal assistant, Amy Ingram, who does only one thing: schedule meetings for you.) You should expect to see much more activity on this front. The value of these horizontal AI assistants will hinge to a large degree on the quality of vertical agents that each can enable and the seamlessness of those integrations.

But don’t expect exclusive integration deals with Siri, Cortana or the like. Any vertical AI agent will want to offer its agent up everywhere. And there is precedent for that model: popular apps go cross device quickly.

4. Conversational UI

The conversational UI, whether in voice or text, will be the dominant interface for these horizontal AI assistants, and for many, if not almost all, vertical agents as well. Whether you are texting with M or chatting with Alexa or asking Amy to set up a meeting, you will be holding a conversation rather than navigating a visual interface. Right now, those conversations can feel stilted and awkward. This is one area in which a single player could really separate itself from the pack. I’m not placing any bets, but to achieve a truly natural level of interaction, you need masses of data and the right data and the willingness to massage it. Here Apple seems to be most disadvantaged, for the moment.

5. No Winner Take All

This is not a winner take all setting. While one or two players may fail to woo consumers to their AI personal assistant, I do not see any reason for a single or even just two players to dominate the market. After all, Alexa gets only marginally better if I use her and you use her too, and this has to do with data collection (the more and more varied data, the smarter she can get).

The opposite may be true for many vertical AI assistants. For example, if Amy were to run everyone’s calendar, she could find the most convenient location for all meeting participants (not just the host) because she would know where each one has been and where each is going on any given day. That means less travel, which saves everyone time.

One thing is indisputable: the major parties in the AI battle have assembled. Now the war for consumers hearts and minds begins. This should be great for the consumer and fun to watch.

|

|

Scooped by

Linda Holroyd

June 9, 2016 2:03 PM

|

Successful CMOs Create the Structure to Innovate

By Jennifer Zeszut | Mar 18, 2015

Change conquers those who fail to receive it as a friend. And change has got marketing in a headlock these days.

Consumers engage with brands, explore products and make purchases in ever more channels and on ever more devices -- and this dizzying trend will only continue. Marketers are struggling to keep up (understatement alert).

Let’s walk through five ways CMOs can help their organizations not just adapt to the changing landscape of marketing, but thrive in it.

1. Promote and Support Specialization

The rapid changes in the marketing landscape puts a premium on specialization. The more channels that emerge, the more difficult it is for a team of generalists to bring to bear all the skills needed to function effectively. A single AOR (agency of record) gets harder to find, too.

Forward-looking CMOs will restructure their marketing organizations, creating centers of excellence for key marketing capabilities (mobile, social, analytics) and perhaps outsourcing marketing activities that require ultra-specialized skills.

Managing specialists brings with it a new challenge: disseminating their specialized knowledge to everyone across the organization who needs it. The CMO’s new role will include setting up knowledge management systems and instilling a culture that documents and shares successes as well as failures.

2. Push Decision-Making Out to the Front Lines

Back when marketing was simpler, CMOs could centralize teams, decision-making, execution and the overall marketing playbook. But the centralized model breaks down when confronted by the staggering number of individual decisions around messaging, creative, channels, marketing mix and more that modern marketers have to make across brands, products, segments and countries. Coca-Cola’s corporate marketing office, for example, can’t anticipate or dictate what mobile ads will work best in Bogota, Colombia.

What’s the answer? Decentralized decision-making paired with strong central guidance. Local marketing teams need to be able to rapidly test (experimentation and execution) and learn (data synthesis and analysis), supported by centrally managed guidelines and alignment tools that facilitate internal benchmarking and sharing of best practices.

Compelling research supports this approach. McKinsey surveyed 20 North American consumer-goods companies, and found that corporate marketing at the strongest-performing companies was primarily a center of excellence that shared information and best practices with line marketers.

At the weaker performers, corporate marketing spent more time doing global brand management, running centralized brand campaigns, and providing actual services like managing relationships with advertising agencies.

CMOs would do well to promote this sort of decentralized but loosely coupled marketing experimentation -- becoming champions of experimentation at the local level while simultaneously cultivating a strong centralized presence that provides best practices, guidance and tools.

3. Ditch Prescriptive Marketing for XPrize Marketing

Centralized marketing departments used to do their best to make brand-building formulaic. Traditional consumer packaged good brands, for instance, had product launch playbooks. The closer we followed the blueprint, the more success we’d have. If we spent X dollars in TV and Y dollars on radio, it would result in Z sales.

But the old formulas don’t work anymore, giving CMOs the opportunity to pioneer new marketing models. One idea is to create a marketing department that runs more like XPrize, an organization that challenges independent teams to solve big, audacious goals. XPrize rigorously defines the challenges and the criteria for success, then incentivizes people around the world to build effective solutions. XPrize is results-focused, yet solution-agnostic.

An XPrize-style CMO would inspire local teams with bold goals and clear KPIs -- criteria by which campaigns, product launches and evergreen efforts will be judged -- and then free those teams to meet marketing challenges creatively and independently, celebrating breakthroughs and sharing best practices quickly to elevate everyone’s performance.

4. Think Systematically

Let’s strengthen a point noted above: Near-autonomous teams innovating and making decisions on the fly will result in disaster unless we provide guidance and guardrails. In the new world of marketing, this is perhaps a CMO’s most important role. CMOs need to oversee the development of frameworks and tools that empower and align their various marketing centers -- data platforms, marketing performance measurement and reporting tools, planning tools, knowledge management portals and the like.

On the process side, CMOs should lead the charge by defining KPIs for marketing, overseeing the development of marketing scorecards, setting up a global marketing taxonomy, and standardizing campaign naming conventions and/or campaign IDs: the foundational efforts that align disparate teams and provide structure for innovation.

5. Foster Agile Marketing

Brands succeed or fail not on the decisions made once a year, like annual marketing mix models, but on the millions of tiny optimizations that marketing teams make every single day.

In a complex and dynamic environment -- the very definition of modern marketing -- speed, flexibility and agility are more important than perfection. CMOs can learn from the iterative approach of software development, where work happens in short, intense bursts interspersed by pauses to assimilate new priorities and new data.

Elevate team members who are comfortable in rapidly evolving spaces. Democratize the data. Pick tools that offer self-serve access to marketing performance data and analysis so that executional marketers can make better decisions on their own. Don’t let the perfect be the enemy of the good.

The CMO as Master Integrator

People talk all the time about the evolving complexity of marketing. We hear less about the implications for marketing’s organizational structure, processes and leadership.

But the KPIs for CMOs -- the criteria by which they’ll be judged -- are changing as well, and CMOs should welcome that development with open arms. This is the CMO’s new job description: Become the master integrator of the marketing function in all its modern complexity.

by Georgie Pauwels

About the Author

Jennifer Zeszut is CEO of Beckon—a SaaS omnichannel marketing analytics software company. Jennifer has been a marketing leader for most of her career working for top brands like eBay, Proctor & Gamble, and Cost Plus World Market. She was the trusted advisor to many more brands as head of Strategy and Analytics for digital agency Razorfish for many years.

|

|

Scooped by

Linda Holroyd

June 2, 2016 3:43 PM

|

Myopia, inertia and other vices that make incumbents victims of disruption

May 24, 2016126,532 views847 Likes126 CommentsShare on LinkedInShare on FacebookShare on Twitter

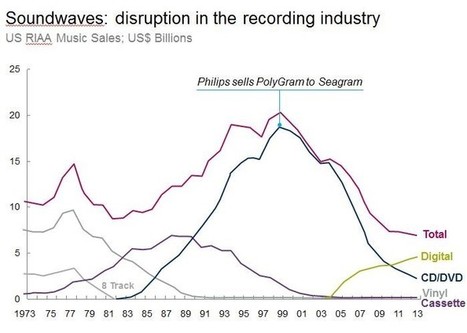

Once upon a time (in 1998, to be precise), PolyGram was a music industry leader, with a roster boasting Bob Marley, U2 and top classical artists. Yet one day Cornelis Boonstra, CEO of PolyGram’s Dutch parent Philips, flew to New York, met with Goldman Sachs, and arranged to sell PolyGram to Seagram for $10.6 billion. Why? Boonstra had come across research showing that consumers were using the new recordable CD-ROM technology largely for one purpose: to copy music.

The MP3 format had barely been invented. Napster was a mere gleam in Sean Parker’s eye. Polygram’s business was humming along. Yet Boonstra detected the first signs of transformational change and decided to act.

I often use this story when I talk to clients about digital disruption, to highlight the value of foresight and quick action. But it also prompts a question: Polygram’s competitors had access to similar research – so why didn’t they act?

Almost 20 years later, with the music industry revolutionized by digital technology, it’s easy to talk about who made the “right” decision and who the “wrong” one. Things are far murkier when you’re in the middle of disruption’s uncertain, hype-filled early stages. Under the real-world constraints of running a large company, executives tend to hope the cloud on the horizon will dissipate. So they wait. In the 1980s and 1990s, steel giants were slow to grasp the potential of mini-mills; minicomputer makers likewise underestimated the personal computer. More recently, publishers, retailers and lodging providers have all fallen victim to similar shortsightedness and inertia. “Companies rarely die from moving too fast,” Reed Hastings, the CEO of Netflix, has observed, “and they frequently die from moving too slowly.”

The good news is that many industries today are still in the early days of digital disruption. That means you still have time to act, provided you can overcome the organizational barriers and match your response to the disruption stage.

Stage 1: Faint signals amidst much noise

As with the music business, the newspaper industry had no shortage of signs that digital disruption was coming. Norway’s Schibsted was one of the earliest media companies to both anticipate the threat and act on the opportunity. As early as 1995, its leaders became convinced that “The Internet is made for classifieds, and classifieds are made for the Internet.”

It’s not surprising that most other publishers didn’t react. At this early stage of disruption, incumbents feel barely any impact on their core business except in the distant periphery. It takes rare acuity to make a preemptive move, likely in the face of opposition from stakeholders and uncertainty as to which trends will really matter.

To escape the myopia that afflicts many incumbents at this stage, you have to challenge your long-standing beliefs about how your industry makes money. As my colleagues put it in a recent article, “These governing beliefs… are often considered inviolable—until someone comes along to violate them.”

Stage 2: Change takes hold

The trend is now clear, the technological and economic drivers validated. At this point, incumbents should nurture new initiatives so they can establish footholds in the new arena. Importantly, those new ventures need autonomy from the core business, even if the goals of the two operations conflict. The idea is to act before you have to.

But with disruption’s impact still not big enough to dampen earnings momentum, motivation is often missing. Even as online classifieds began to take off, most newspaper publishers lacked a sense of urgency because their market share remained largely unaffected and the new players were small and unprofitable.

Now I know how hard it is for a company’s leaders to support experimental ventures when the core business is still going strong. When Netflix disrupted itself in 2011 by shifting focus from DVDs to streaming, its profit dropped by 90% and its share price plunged. Few boards and investors can handle that kind of pain. The vague longer-term threat just doesn’t seem as dangerous as the immediate hardship. Additionally, management teams are more comfortable developing strategies for businesses they know, and are reluctant to enter a new game with rules they don’t understand.

The upshot: Most incumbents dabble. Many newspapers built online add-ons to their classified businesses, but few were willing to risk cannibalizing their traditional revenue streams.

Stage 3: The inevitable transformation

By now, the future is pounding on the door. The new model has proven superior to the old and the industry is rapidly moving to it. The incumbent’s challenge now lies in accelerating its own transformation by aggressively shifting resources to the new ventures, even if they hurt the core business. Think of it as treating new businesses like venture-capital investments that only pay off if they scale rapidly, while the old ones are subject to a private equity-style workout.

In my experience, this is the hardest stage for incumbents to navigate, because it requires surmounting the inertia that can afflict companies at the best of times. As performance starts to suffer, tightening up budgets, companies naturally tend to cut back on peripheral activities and focus on the core. The reflex to conserve resources kicks in just when you most need to aggressively reallocate.

Which makes it all the more instructive to consider what Axel Springer did. The German media company was “a mere Internet midget” until it leapt into action in 2006. Within seven years, it acquired 67 digital properties and launched 90 initiatives of its own. The ambitious campaign paid off: By 2012, Axel Springer’s websites had almost twice the number of unique visitors as Schibsted’s. The lesson: Incumbents can win even with a late start, provided they throw themselves wholly into the race.

Stage 4: Adapting to the new normal

By now, you have no choice but to accept reality: the industry has fundamentally changed. Most incumbents find their cost base is out of line with the new (likely much shallower) profit pools and their earnings are caving in. They have little choice but to restructure – and in some cases would be best off exiting the business.

So in which stage of disruption is your industry? If it’s one of the first three, it’s not too late to act. Being a winner in a previous era is not an entitlement to being a winner in the next one – but nor need it be a hindrance.

For a deeper exploration of incumbents’ disruption challenge, please read my recent article. I also encourage you to view this animated narration, which walks you through the four stages of disruption.

I’d love to hear your thoughts on the barriers and responses I’ve described here. Do your experiences bear them out?

|

|

Scooped by

Linda Holroyd

May 24, 2016 7:00 PM

|

Article - McKinsey Quarterly - May 2016

The ‘tech bubble’ puzzle

By David Cogman and Alan Lau

Public and private capital markets seem to value technology companies differently. Here's why.

Aggressive valuations among technology companies are hardly a new phenomenon. The widespread concerns over high pre-IPO valuations today recall debates over the technology bubble at the turn of the century—which also extended to the media and telecommunications sectors. A sharp decline in the venture-capital funding for US-based companies in the first quarter of the year feeds into that debate,1 though the number of “unicorns”—start-up companies valued at more than a billion dollars—over that same period continued to rise.

The existence of these unicorns is just one significant difference between 2000 and 2016. Until seven years ago, no venture capital–backed company had ever achieved a billion-dollar valuation before going public, let alone the $10 billion valuation of 14 current “deca-corns.” Also noteworthy is the fact that high valuations predominate among private, pre-IPO companies, rather than public ones, as was the case at the turn of the millennium. And then there’s the global dimension: innovation and growth in the Chinese tech sector are much bigger forces today than they were in 2000.2

All of these factors suggest that when the curtain comes down on the current drama, the consequences are likely to look quite different from those of 16 years ago. Although the underlying economic changes taking place during this cycle are no less significant than the ones during the last cycle, valuations of public-market tech companies are, at this writing, mostly reasonable—perhaps even slightly low by historical standards. A slump in current private-sector valuations would be unlikely to have much impact on the broader public markets. And the market dynamics in China and the United States are far from similar. In this article, we’ll elaborate on the fundamentals at work, which extend beyond the strength of the current pipeline of pre-IPO tech companies, and on the funds that have washed over the venture-capital industry in recent years.

The lessons of history

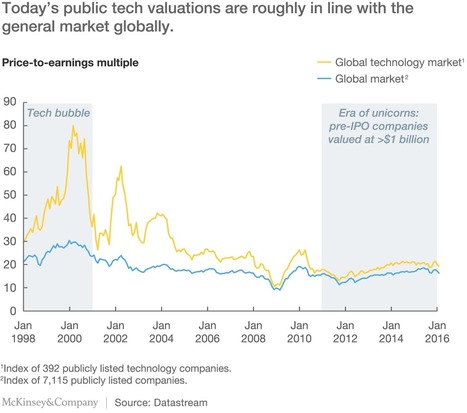

The defining feature of the 2000 tech bubble was that it was a public-market bubble. At the start of 1998, valuations for tech companies were 40 percent higher than for the general market: at the peak of the bubble in early 2000, they were 165 percent higher. However, at that point the largest-ever venture-invested tech start-up we could find evidence of barely exceeded a $6 billion valuation at IPO—a small number by today’s standards. Moreover, a considerable part of the run-up in valuation came not from Internet companies but from old-school telecom companies, which saw the sector’s total value grow by more than 250 percent between 1997 and 2000.

Equity markets seem to have learned from that episode. In aggregate, publicly held tech companies in 2015 showed little if any sign of excess valuations, despite the steadily escalating ticket size of the IPOs. Valuations of public tech companies in 2015 averaged 20 times earnings, only 10 percent above the general market, and they have been relatively stable at those levels since 2010.

By historical standards, that’s relatively low: over the past two decades, tech companies on average commanded a 25 percent valuation premium, often much more. During the technology and telecommunications bubble of 2000, the global tech-sector valuation peaked at just under 80 times earnings, more than 3 times the valuation of nontech equities. And over the five years after the bubble burst in 2001, the tech sector enjoyed a valuation premium of, on average, 50 percent over the rest of the equity market (exhibit). Even with a focus limited to Internet companies—the sector most often suspected of runaway valuations—there is no obvious bubble among public companies at present.

Nor do these companies’ valuation premiums appear excessive to the general market when viewed in the light of their growth expectations. Higher multiples are in most cases explained by higher consensus forecasts for earnings growth and margins. The market could be wrong in these expectations, but at least it is consistent.

China is a notable exception, though equity valuations in China always need to be viewed with caution. Before 2008, Chinese tech companies were valued on average at a 50 to 60 percent premium over the general market. Since then, that premium has grown to around 190 percent. Why? In part because the Chinese online market is both larger and faster growing than the United States, and the government has ambitious plans to localize the higher-value parts of the hardware value chain over the next few years.3 The growth in China’s nonstate-owned sector is another part of the story. Many of the new technology companies coming to the market in the past five years have been nonstate-owned, and nonstate-owned companies are consistently valued 50 percent to 100 percent higher than their state-owned peers in the same segments.

This time, it’s different?

Where the picture today is most different from 2000 is in the private capital markets, and in how companies approach going public.

It wasn’t until 2009 that a pre-IPO company reached a $1 billion valuation. The majority of today’s unicorn companies reached that valuation level in just the past 18 months. They move in a few distinct herds: roughly 35 percent of them are in the San Francisco Bay area, 20 percent are in China, and another 15 percent are on the US East Coast.

Notable shifts in funding and valuations have accompanied the rising number of these companies. The number of rounds of pre-IPO funding has increased, and the average size of venture investments more than doubled between 2013 and 2015, which saw both the highest average deal size and highest number of deals ever recorded. Increases in valuation between rounds of funding have also been dramatic: it’s not unusual to see funding rounds for Chinese companies involving valuation increases of up to five times over a period of less than a year.

Whatever the quality of new business models emerging in the technology sector, what’s unmistakable is that the venture-capital industry has built up an unprecedented supply of cash. The amount of uninvested but committed funds in the industry globally rose from just over $100 billion in 2012 to nearly $150 billion in 2015, the highest level ever. And where buyout, real-estate, and special-situations funds all have the luxury of looking across a range of deal sizes, industries, or even asset classes, venture capitalists have less flexibility. Many venture funds fish in the same pool of potential deals, and some only within their geographic backyard.

The liquidity in the venture-capital industry has been augmented by the entry of a new set of investors, with limited partners in some funds looking for direct investment opportunities into venture-funded companies as they approach IPO. This allows companies to do much larger pre-IPO funding rounds, marketed directly to institutional investors and high-net-worth individuals. These investors dwarf the venture-capital industry in scale and can therefore extend the runway before IPO, though not indefinitely: their participation is contingent on the promise of an eventual exit via IPO or sale.

Thus valuations of individual pre-IPO start-ups need to be viewed cautiously, as the actual returns their venture-capital investors earn flow as much from protections built into the deal terms as by the valuation number itself. In a down round (when later-stage investors come in at a lower valuation than the previous round), these terms become critical in determining how the pie is divided among the different investors.

The IPO hurdle

Private-equity markets do not exist in isolation from public markets: with few exceptions, the companies venture capitalists invest in must eventually list on public exchanges, or be sold to a listed company. The current disconnect between valuations in these two markets will somehow be resolved, either gradually, through a long series of lower-priced IPOs, or suddenly, in a massive slump in pre-IPO valuations.

Several factors incline toward the former. Some late-stage investors, such as Fidelity and T. Rowe Price, have already marked down their investments in multiple unicorns, and it’s increasingly common for start-up IPOs to raise less capital than their pre-IPO valuations. Given the still-lofty level of those valuations, this no longer attracts the extreme stigma that it did in 2000. Regardless of how the profits divide up, the company is still independent and now listed.

Tech companies also are staying private for, on average, three times longer.4 A much greater share of companies wait until they are making accounting profits before coming to market. From 2001 to 2008, fewer than 10 percent of tech IPOs were launched after the company had reached profitability: since 2010, almost 50 percent had reached at least the break-even point. The number of companies coming to market has remained relatively flat since the 1990s technology bubble. But the average capitalization at IPO time has more than doubled in the past five years, reflecting the fact that the companies making public offerings are larger and more mature.

What happens post-IPO? Over the past three years, 61 tech companies have gone public with a market cap of more than $1 billion. The median company in this group is now trading just 3 percent above its listing price. The valuations of a number of former unicorns are lower still, including well-known companies like Twitter in the United States and Alibaba in China.

History paints a challenging picture for many of these recently listed companies. Between 1997 and 2000, there were 898 IPOs of technology companies in the United States, valued collectively at around $171 billion. The attrition among this group was brutal. By 2005, only 303 of them remained public. By 2010, that number had declined to 128. In the decade from 2000 to 2010, the survivors among these millennials had an average share-price return of –3.7 percent a year. In the subsequent five years, they returned only –0.8 percent per annum—despite soaring equity markets.

The geographic dimension

The current crop of pre-IPO companies is far more diverse than in 2000. It will be particularly interesting to see which of the two largest geographic groups—the US and the Chinese unicorns—weathers the shakeout best. Consider just Internet companies. The total market value of listed Internet companies today is around $1.5 trillion. Of this, US companies represent nearly two-thirds, and Chinese companies—mostly listed in the United States—almost all of the remainder. The rest of the world put together amounts to less than 5 percent.

The differences between the unicorns in these regions are revealing. Of the more than 100 unicorns operating in the United States and China, only 14 have overlapping investors, and just two—the electronics company Xiaomi and the transportation-network company Didi Chuxing (formerly Didi Kuaidi)—account for two-thirds of the combined valuation of all of them. Three-quarters of the Chinese unicorns are primarily in the online space, compared with less than half of the US unicorns, and these serve separate user bases as a result of regulatory separation of the two countries’ Internet markets.

It is not obvious which group holds the advantage. The local market to which Chinese Internet companies have access is substantial, with well over twice as many users as in the United States; the e-commerce market is significantly larger and growing almost three times as fast. Moreover, the three Chinese Internet giants, Baidu, Alibaba, and Tencent, have invested in many of the Chinese unicorns, giving them easier access to a platform of hundreds of millions of users on which to operate.

The Chinese unicorns also have a much higher proportion of “intermediary” companies—start-ups that act primarily as channels or resellers of other companies’ services and take a cut of earnings. Around a third of the Chinese unicorns have business models of this kind, compared with only one in eight of their US counterparts. Finally, the US start-ups tend to adapt faster to a global audience. Although there are several established Chinese technology companies that have successfully made the leap to the global stage, such as Huawei, Lenovo, and ZTE, very few of the companies founded in the past five years have reached that point.

For all the differences between the tech start-up markets of today and those of 2000, both periods are marked by excitement at the potential for new technologies and businesses to stimulate meaningful economic change. To the extent that valuations are excessive, the private markets would appear to be more vulnerable. But perspective is important. The market capitalization of the US and Chinese equity markets declined by $2.5 trillion in January alone. Any correction to the roughly half a trillion dollars in combined value of all the unicorns as of their last funding round is likely to seem milder than the correction of the last technology bubble.

About the author(s)

David Cogman is a principal in McKinsey’s Hong Kong office, where Alan Lau is a director.

|

|

Scooped by

Linda Holroyd

May 24, 2016 6:39 PM

|

Historically, sales and marketing have not always been harmonious bedfellows, but the opportunities afforded by big data and the complexities of connecting with customers in more granular ways require integrated and collaborative models that bring marketing and sales together.

On average, a B2B customer will regularly use six different interaction channels throughout the purchase process, and two-thirds come away frustrated by inconsistent experiences. The notion of a customer decision journey (CDJ) around which marketing and sales collaborate has become embedded in many leading sales organizations, but the journey differs by customer segment, with needs and expectations varying at each stage. Insightful customer research and advanced analytics mean these segments can be defined ever more precisely by marketing, but that work is wasted unless sales reaches the right people with the right offer. Nor is the onus all on marketing. Both functions generate enormous volumes of valuable data on customer segments and preferences, but at outperforming companies, the front line reports back to help marketing refine its value propositions.

As data becomes more readily available and easier to crunch, companies can move from broad-based predictive modeling to a much more personalized approach. Information from past interactions with a customer or from existing sources can be used to instantaneously customize the buyer’s experience. Remembering customer preferences is just the beginning; true personalization is the next wave in a customer’s journey and helps drive loyalty.

Pay attention to presales

For B2B sales, “personalization” is about delivering tailored solutions. To do that, sales organizations need a very clear understanding of customer needs. This requires technical experts to be involved with customers at a very early stage in the buying journey. These presales specialists are so important that one account manager at a global technology company said, “Every sales leader would say they couldn’t run the business without a specialist. The competitive dynamic is such that if you don’t bring your A-game to the deal, you’re not going to win.”

In addition to getting experts working on deals, the presales function can play a vital role in qualifying leads. Social media, digital marketing, advanced analytics, and the more pervasive use of inside sales have exponentially increased the number of deals a company can pursue. But too many potential deals can have a negative effect on the organization by diffusing focus and taxing resources. It is far more efficient and effective to qualify leads using data and analytic tools, so that only the most attractive ones then move into the pipeline.

Despite its importance, presales is often understaffed and overlooked. A high-performing sales organization should have about two-thirds of its presales team undertaking technical presales activities (crafting solutions to customers’ problems) and the rest involved with commercial presales activities (managing deal qualification, pricing, and bid). For maximum productivity, the function should account for 40 to 50 percent of the overall commercial headcount. B2B companies with strong presales capabilities consistently achieve win rates in excess of 40 percent in new business, which is 10 to 15 points higher than we usually observe.

Although this technical sales support is most associated with B2B sales, it can apply to B2C, too. Apple’s product geniuses may be the best-known examples, but some car dealers send the product expert, not the salesperson, out on the customer’s test drive to answer questions.

With its focus on how digital technologies, data, and analytics are changing the face of selling, it’s natural that Sales Growth concludes with some thoughts on where the future may lie for sales organizations. The pervasive automation of back-office processes and the complete outsourcing of the sales function, enabled in part by precisely this technology shift, are redrawing the lines of sales management.

Machine learning and intelligent automation are already transforming a wide range of industries and functions. By 2020, customers will manage 85 percent of their relationship with an enterprise without interacting with a human, and 40 percent of sales activities could be automated using technology that already exists.4

“Cognitive agents” such as IPsoft’s Amelia, already understand, interact, and—crucially—learn in order to solve customers’ problems in industries from financial services to telecommunications. They can parse natural language and independently determine which questions to ask in order to diagnose what the customer really needs and act accordingly. It’s a small step from helping customers tackle basic processes to selling, and Amelia can already solve basic customer problems, for example, moving a customer to a more comprehensive phone tariff.

These new technologies and trends do not spell the end of salesmanship. They will fulfill much of the presales work, but many sales will still need people to close them. Making sure that the right salesperson is in place is becoming easier, too, thanks to analytics. Matching the seller with the lead and equipping the salesperson with the maximum amount of useful information to close the deal will characterize the new sales environment.

AI can be deployed beyond just responding to queries. Today, even with modern CRM systems, only a quarter of leads are actually contacted. A bot can contact 100 percent of them and do so in a relatively engaging, human-like manner that should not put off any potential customers.5 Companies that have pioneered the use of AI in sales rave about the impact, which includes an increase in leads and appointments of more than 50 percent, cost reductions of 40 to 60 percent, and call-time reductions of 60 to 70 percent. Customers love it too—these companies have seen an increase in customer satisfaction as customers get what they want faster.

Sales teams will need to be comfortable with algorithms and able to work with data scientists and marketing-tech experts to design solutions. Sales leaders, meanwhile, will need clear escalation and exception protocols to manage the trickiest or most valuable situations. As the machines get smarter, the biggest differentiator of success will be the human touch. Senior executives will need to ask the right questions, vigorously approach the exceptions that the machines highlight, and shine in the areas that AI will always struggle with: ambiguity and emotional engagement.

With more sales organizations turning to technology vendors to solve problems, is it only a matter of time before the whole sales function is outsourced? Outsourcing the part of your business that involves selling to customers sounds risky at first, but for pioneering companies, the fact that the salesperson doesn’t work directly for the company no longer matters, nor is it important that s/he may be selling products from several different companies in the same category over the course of a week. What matters for the manufacturer is that someone is out there pounding the pavement, the phone, and the digital platforms, getting the product into the hands of customers more cheaply and effectively than the company can do itself.