Mobile meets health meets personalization . . .

"The trend among patients to use smartphone applications as healthcare aids continues to grow, according to research published Nov. 8 by the Pew Internet & American Life Project."

Get Started for FREE

Sign up with Facebook Sign up with X

I don't have a Facebook or a X account

|

Scooped by

Linda Holroyd

onto Innovating in an Age of Personalization November 21, 2012 4:55 PM

|

Mobile meets health meets personalization . . .

"The trend among patients to use smartphone applications as healthcare aids continues to grow, according to research published Nov. 8 by the Pew Internet & American Life Project."

Your new post is loading...

Your new post is loading... Your new post is loading...

Your new post is loading...

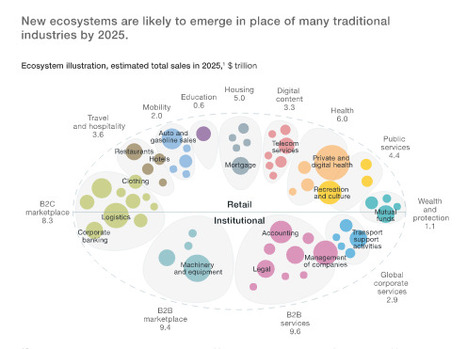

Competing in a world of sectors without bordersBy Venkat Atluri, Miklos Dietz, and Nicolaus Henke Digitization is causing a radical reordering of traditional industry boundaries. What will it take to play offense and defense in tomorrow’s ecosystems? Rakuten Ichiba is Japan’s single largest online retail marketplace. It also provides loyalty points and e-money usable at hundreds of thousands of stores, virtual and real. It issues credit cards to tens of millions of members. It offers financial products and services that range from mortgages to securities brokerage. And the company runs one of Japan’s largest online travel portals—plus an instant-messaging app, Viber, which has some 800 million users worldwide. Retailer? Financial company? Rakuten Ichiba is all that and more—just as Amazon and China’s Tencent are tough to categorize as the former engages in e-commerce, cloud-computing, logistics, and consumer electronics, while the latter provides services ranging from social media to gaming to finance and beyond. Organizations such as these—digital natives that are not defined or constrained by any one industry—may seem like outliers. How applicable to traditional industries is the notion of simultaneously competing in multiple sectors, let alone reimagining sector boundaries? We would be the first to acknowledge that opportunities to attack and to win across sectors vary considerably and that industry definitions have always been fluid: technological developments cause sectors to appear, disappear, and merge. Banking, for example, was born from the merger of money exchange, merchant banking, savings banking, and safety-deposit services, among others. Supermarkets unified previously separate retail subsectors into one big “grocery” category. Changes such as these created new competitors, shifted vast amounts of wealth, and reshaped significant parts of the economy. Before the term was in vogue, one could even say the shifts were “disruptive.” Yet there does appear to be something new happening here. The ongoing digital revolution, which has been reducing frictional, transactional costs for years, has accelerated recently with tremendous increases in electronic data, the ubiquity of mobile interfaces, and the growing power of artificial intelligence. Together, these forces are reshaping customer expectations and creating the potential for virtually every sector with a distribution component to have its borders redrawn or redefined, at a more rapid pace than we have previously experienced. Consider first how customer expectations are shifting. As Steve Jobs famously observed, “A lot of times, people don’t know what they want until you show it to them.” By creating a customer-centric, unified value proposition that extends beyond what end users could previously obtain (or, at least, could obtain almost instantly from one interface), digital pioneers are bridging the openings along the value chain, reducing customers’ costs, providing them with new experiences, and whetting their appetites for more. We’ve all experienced businesses that once seemed disconnected fitting together seamlessly and unleashing surprising synergies: look no farther than the phone in your pocket, your music and video in the cloud, the smart watch on your wrist, and the TV in your living room. Or consider the 89 million customers now accessing Ping An Good Doctor, where on a single platform run by the trusted Ping An insurance company they can connect with doctors not only for online bookings but to receive diagnoses and suggested treatments, often by exchanging pictures and videos. What used to take many weeks and multiple providers can now be done in minutes on one app. Now nondigital natives are starting to think seriously about their cross-sector opportunities and existential threats that may lurk across boundaries. One example: We recently interviewed 300 CEOs worldwide, across 37 sectors, about advanced data analytics. Fully one-third of them had cross-sector dynamics at top of mind. Many worried, for instance, that “companies from other industries have clearer insight into my customers than I do.” We’ve also seen conglomerates that until recently had thought of themselves as little more than holding companies taking the first steps to set up enterprise-wide consumer data lakes, integrate databases, and optimize the products, services, and insights they provide to their customers. Although these companies must of course abide by privacy laws—and even more, meet their users’ expectations of trust—data sets and sources are becoming great unifiers and creating new, cross-sectoral competitive dynamics. Do these dynamics portend a sea change for every company? Of course not. People will still stroll impromptu into neighborhood stores, heavy industry (with the benefit of technological advances, to be sure) will go on extracting and processing the materials essential to our daily lives, and countless other enterprises beyond the digital space will continue to channel the ingenuity of their founders and employees to serve a world of incredibly varied preferences and needs. It’s obvious that digital will not—and cannot—change everything. But it’s just as apparent that its effects on the competitive landscape are already profound and that the stakes are getting higher. As boundaries between industry sectors continue to blur, CEOs—many of whose companies have long commanded large revenue pools within traditional industry lines—will face off against companies and industries they never previously viewed as competitors. This new environment will play out by new rules, require different capabilities, and rely to an extraordinary extent upon data. Defending your position will be mission critical, but so too will be attacking and capturing the opportunities across sectors before others get there first. To put it another way: within a decade, companies will define their business models not by how they play against traditional industry peers but by how effective they are in competing within rapidly emerging “ecosystems,” comprising a variety of businesses from dimensionally different sectors. A world of digital ecosystemsAs the approaching contest plays out, we believe an increasing number of industries will converge under newer, broader, and more dynamic alignments: digital ecosystems. A world of ecosystems will be a highly customer-centric model, where users can enjoy an end-to-end experience for a wide range of products and services through a single access gateway, without leaving the ecosystem. Ecosystems will comprise diverse players who provide digitally accessed, multi-industry solutions. The relationship among these participants will be commercial and contractual, and the contracts (whether written, digital, or both) will formally regulate the payments or other considerations trading hands, the services provided, and the rules governing the provision of and access to ecosystem data. Beyond just defining relationships among ecosystem participants, the digitization of many such arrangements is changing the boundaries of the company by reducing frictional costs associated with activities such as trading, measurement, and maintaining trust. More than 80 years ago, Nobel laureate Ronald Coase argued that companies establish their boundaries on the basis of transaction costs like these: when the cost of transacting for a product or service on the open market exceeds the cost of managing and coordinating the incremental activity needed to create that product or service internally, the company will perform the activity in-house. As digitization reduces transaction costs, it becomes economic for companies to contract out more activities, and a richer set of more specialized ecosystem relationships is facilitated. Rising expectationsThose ecosystem relationships, in turn, are making it possible to better meet rising customer expectations. The mobile Internet, the data-crunching power of advanced analytics, and the maturation of artificial intelligence (AI) have led consumers to expect fully personalized solutions, delivered in milliseconds. Ecosystem orchestrators use data to connect the dots—by, for example, linking all possible producers with all possible customers, and, increasingly, by predicting the needs of customers before they are articulated. The more a company knows about its customers, the better able it is to offer a truly integrated, end-to-end digital experience and the more services in its ecosystem it can connect to those customers, learning ever more in the process. Amazon, among digital natives, and Centrica, the British utility whose Hive offering seeks to become a digital hub for controlling the home from any device, are early examples of how pivotal players can become embedded in the everyday life of customers. For all of the speed with which sector boundaries will shift and even disappear, courting deep customer relationships is not a one-step dance. Becoming part of an individual’s day-to-day experience takes time and, because digitization lowers switching costs and heightens price transparency, sustaining trust takes even longer. Over that time frame, significant surplus may shift to consumers—a phenomenon already underway, as digital players are destroying billions to create millions. It’s also a process that will require deploying newer tools and technologies, such as using bots in multidevice environments and exploiting AI to build machine-to-machine capabilities. Paradoxically, sustaining customer relationships will depend as well on factors that defy analytical formulae: the power of a brand, the tone of one’s message, and the emotions your products and services can inspire. Strategic movesThe growing importance of customer-centricity and the appreciation that consumers will expect a more seamless user experience are reflected in the flurry of recent strategic moves of leading companies across the world. Witness Apple Pay; Tencent’s and Alibaba’s service expansions; Amazon’s decisions to (among other things) launch Amazon Go, acquire Whole Foods, and provide online vehicle searches in Europe; and the wave of announcements from other digital leaders heralding service expansion across emerging ecosystems. Innovative financial players such as CBA (housing and B2B services), mBank (B2C marketplace), and Ping An (for health, housing, and autos) are mobilizing. So are telcos, including Telstra and Telus (each playing in the health ecosystem), and retailers such as Starbucks (with digital content, as well as seamless mobile payments and pre-ordering). Not to be left out are industrial companies such as GE (seeking to make analytics the new “core to the company”) and Ford (which has started to redefine itself as “a mobility company and not just as a car and truck manufacturer”). We’ve also seen ecosystem-minded combinations such as Google’s acquisition of Waze and Microsoft’s purchase of LinkedIn. Many of these initiatives will seem like baby steps when we look back a decade from now, but they reveal the significance placed by corporate strategists on the emergence of a new world. While it might be tempting to conclude as a governing principle that aggressively buying your way into new sectors is the secret spice for ecosystem success, massive combinations can also be recipes for massive value destruction. To keep your bearings in this new world, focus on what matters most—your core value propositions, your distinct competitive advantages, fundamental human and organizational needs, and the data and technologies available to tie them all together. That calls for thinking strategically about what you can provide your customers within a logically connected network of goods and services: critical building blocks of an ecosystem, as we’ve noted above. Value at stakeBased on current trends, observable economic trajectories, and existing regulatory frameworks, we expect that within about a decade 12 large ecosystems will emerge in retail and institutional spaces. Their final shape is far from certain, but we suspect they could take something like the form presented in Exhibit 1. Exhibit 1 Sidebar China by the numbers

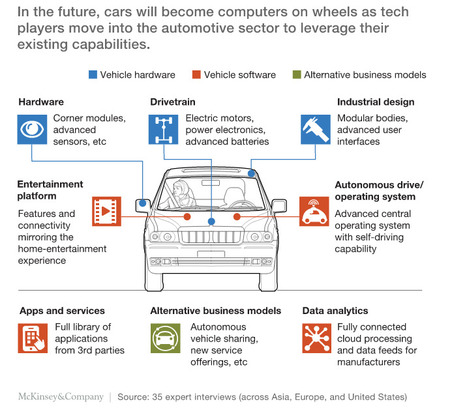

The actual shape and composition of these ecosystems will vary by country and region, both because of the effects of regulations and as a result of more subtle, cultural customs and tastes. We already see in China, for example, how a large base of young, tech-savvy consumers, a wide amalgam of low-efficiency traditional industries, and, not least, a powerful regulator have converged to give rise to leviathans such as Alibaba and Tencent—ideal for the Chinese market but not (at least, not yet) able to capture significant share in other geographies (see sidebar, “China by the numbers”). The value at stake is enormous. The World Bank projects the combined revenue of global businesses will be more than $190 trillion within a decade. If digital distribution (combining B2B and B2C commerce) represents about one-half of the nonproduction portion of the global economy by that time, the revenues that could, theoretically, be redistributed across traditional sectoral borders in 2025 would exceed $60 trillion—about 30 percent of world revenue pools that year. Under standard margin assumptions, this would translate to some $11 trillion in global profits, which, once we subtract approximately $10 trillion for cost of equity, amounts to $1 trillion in total economic profit.1 Snapshots of the futureAgain, it’s uncertain how much of this value will be reapportioned between businesses and consumers, let alone among industries, sectors, and individual companies, or whether and to what extent governments will take steps to weigh in. To a significant degree, many of the steps that companies are taking and contemplating are defensive in nature—fending off newer entrants, by using data and customer relationships to shore up their core. As incumbents and digital natives alike seek to secure their positions while building new ones, ecosystems are sure to evolve in ways that surprise us. Here is a quick look at developments underway in three of them. Consumer marketplacesBy now, purchasing and selling on sites such as Alibaba, Amazon, and eBay is almost instinctive; retail has already been changed forever. But we expect that the very concept of a clearly demarcated retail sector will be radically altered within a decade. Three critical, related factors are at work. First, the frame of reference: what we think of now as one-off purchases will more properly be understood as part of a consumer’s passage through time—the accumulation of purchases made from day to day, month to month, year to year, and ultimately the way those interact over a lifetime. Income and wealth certainly have predictive value for future purchases, but behavior matters even more. Choices to eat more healthily, for example, correlate to a likelihood for higher consumption of physical fitness gear and services, and also to a more attractive profile for health and life insurers, which should result in more affordable coverage. The second major factor, reinforcing the first, is the growing ability of data and analytics to transform disparate pieces of information about a consumer’s immediate desires and behavior into insight about the consumer’s broader needs. That requires a combination of capturing innumerable data points and turning them, within milliseconds, into predictive, actionable opportunities for both sellers and buyers. Advances in big data analytics, processing power, and AI are already making such connections possible. This all generates a highly robust “network factor”—the third major force behind emerging consumer marketplaces. In a world of digital networks, consumer lenders, food and beverage providers, and telecom players will simultaneously coexist, actively partner, and aggressively move to capture share from one another. And while digitization may offer the sizzle, traditional industries still have their share of the steak. These businesses not only provide the core goods and services that end users demand, but often also have developed relationships with other businesses along the value chain and, most important, with the end users themselves. Succeeding in digital marketplaces will require these companies to stretch beyond their core capabilities, to be sure, but if they understand the essentials of what’s happening and take the right steps to secure and expand their relationships, nondigital businesses can still hold high ground when the waves of change arrive. B2B servicesThe administrative burdens of medium, small, and microsize companies are both cumbersome and costly. In addition to managing their own products and services, these businesses (like their larger peers) must navigate a slew of necessary functions including human resources, tax planning, legal services, accounting, finance, and insurance. Today, each of these fields exists as an independent sector, but it’s easy to imagine them converging within a decade on shared, cloud-based platforms that will serve as one-stop shops. With so many service providers available at the ease of a click, all with greater transparency on price, performance, and reputation, competition will ramp up and established players can anticipate more challengers from different directions. At the same time, it’s likely that something approaching a genuine community will develop, with businesses being able to create partnerships and tap far more sophisticated services than they can at present—including cash-planning tools, instant credit lines, and tailored insurance. Already, we can glimpse such innovations starting to flourish in a range of creative solutions. Idea Bank in Poland, for example, offers “idea hubs” and applications such as e-invoicing and online factoring. ING’s commercial platform stretches beyond traditional banking services to include (among other things) a digital loyalty program and crowdfunding. And Lloyds Bank’s Business Toolbox includes legal assistance, online backup, and email hosting. As other businesses join in, we expect the scope and utility of this space to grow dramatically. MobilityFinally, consider personal mobility, which encompasses vehicle purchase and maintenance management, ridesharing, carpooling, traffic management, vehicle connectivity, and much more. The individual pieces of the mobility puzzle are starting to become familiar, but it’s their cumulative impact that truly shows the degree to which industry borders are blurring (Exhibit 2). Exhibit 2 Emerging priorities for the borderless economyThese glimpses of the future are rooted in the here and now, and they are emblematic of shifts underway in most sectors of the economy—including, more likely than not, yours. We hope this article is a useful starting point for identifying potential industry shifts that could be coming your way. Recognition is the first step, and then you need a game plan for a world of sectors without borders. The following four priorities are critical:

No one can precisely peg the future. But when we study the details already available to us and think more expansively about how fundamental human needs and powerful technologies are likely to converge going forward, it is difficult to conclude that tomorrow’s industries and sector borders will look like today’s. Massive, multi-industry ecosystems are on the rise, and enormous amounts of value will be on the move. Companies that have long operated with relative insularity in traditional industries may be most open to cross-boundary attack. Yet with the right strategy and approach, leaders can exploit new openings to go on offense, as well. Now is the time to take stock and to start shaping nascent opportunities.

Linda Holroyd's insight:

The digital experiences people expect and marketers can deliver have changed dramatically, and Jason Spero has had a front-row seat. Now, Google’s VP of Global Performance Solutions is keeping an eye on the consumer behaviors shaping the next generation of experiences. We’re living in the golden age of user experience. Startups are upending entire industries with their focus on simplicity, while traditional companies reinvent themselves on mobile to stay relevant. But it’s not the technology that gets me most excited. Rather it’s the rich experiences that technology is enabling for consumers and the impact it’s having on marketers like you and me. The speed at which brands are introducing compelling new experiences is only accelerating. We’ve not seen anything like it before. For us as marketers, that means consumer expectations are higher than ever. We’re no longer competing with the best experience in our respective categories. We’re now competing with the best experience a consumer has ever had. Every time a company designs a rich, useful, or new experience, it raises the bar for what consumers care about. On the flip side, if an experience is frustrating or annoying, a consumer may not give that company a second chance. Building a great user experience is a challenge, especially as we all grapple with how and when to experiment with new technologies. But rather than think about the technologies first, I find it helps to imagine the experience you’d want as a consumer, apply it to your brand, and build toward that. Here are three things I hear from consumers when it comes to what they expect from brands: “Help me faster” Technology is becoming assistive in ways we couldn’t have imagined a few years ago. We can pay for coffee with a tap. We can deposit a check by snapping a photo. And we can order laundry detergent with a voice command to a digital assistant. But as technology enables faster experiences, consumers are growing impatient. Their willingness to wait is declining and, as a result, consumers are shifting their thinking from, “Who does it best?” to “Who does it best now?” Source: Google Data, Global, n=3,700 aggregated, anonymized Google Analytics data from a sample of mWeb sites opted into sharing benchmark data, Mar. 2016. There’s a price to pay if you don’t consider speed. Fifty-three percent of people will abandon a mobile site if it takes more than three seconds to load.1 Now here’s the reality: We tested 900,000 mobile sites globally and found that the average time it takes to fully load a mobile page is 22 seconds.2 Speed is a developer’s problem, a designer’s problem, and therefore, a marketer’s problem. When marketers prioritize speed it has a ripple effect. Designers must then focus on selecting visual elements, fonts, and a design structure that allow for fast, frictionless mobile experiences. And developers can further optimize, ensuring the best mobile experience possible. “Know me better” Personalized and relevant experiences are key to connecting with consumers, and they have a positive impact on the bottom line. Eighty-nine percent of U.S. marketers reported that personalization on their websites or apps resulted in an increase in revenue.3 Source: eMarketer/Evergage, "2016 Trends in Personalization," conducted by Researchscape. Data was provided to eMarketer by Evergage; June 14, 2016. But personalization is a strategy, not a feature. We have an opportunity to be smarter with data, using important signals about customers—such as browsing behavior or CRM data—to shape their experiences. For example, when Maybelline was preparing to launch new products for contouring—a type of makeup application that is becoming more mainstream—it used Google Insights to craft how-to videos, which are personalized by intent and demographic. As a result, Maybelline’s videos racked up 9M views. Likewise, 63% of people expect brands to use their purchase history to provide them with personalized experiences.4 In other words, if you know I just purchased a pair of shoes, then offer me socks or a matching belt to go with them. “Wow me everywhere”Brands need to consider how all of their experiences—across media, channels, and devices—fit together. Source: Google/Greenberg, U.S., “Rising Expectations in Consumer Experiences,” n=1,501 consumers aged 18–54, Mar. 2017. Sixty-two percent of people expect brands to deliver a consistent experience every time they interact with a brand. But only 42% believe brands actually do provide a consistent experience. Walgreens provides a good example of seamless, consistent experiences in action. The brand’s team recognized that mobile could help it remove barriers between online and offline. Its mobile app connects consumers with a doctor or pharmacist online, and consumers can then pick up prescriptions in-store. Likewise, beauty advisors are armed with tablets, so they can quickly pull up past purchases online and make recommendations for offline purchases. The approach is paying off. Customers who interact with Walgreens in-store and on mobile are six times more valuable than someone who only visits the brand’s physical stores. Bringing it all togetherAs consumer behaviors shift, it will be important to rethink the investments we make in the user experience. Removing friction and bridging the gaps between channels—all while treating each customer as a unique individual—will be key. Ultimately, creating great digital customer experiences is not solely a product challenge or a marketing challenge. It’s a business opportunity. And those who invest in creating memorable experiences will win users’ hearts, minds, and ultimately, dollars. Jason SperoVP of Global Performance Solutions at Google

Linda Holroyd's insight:

Help me faster. Know me better. Wow me everywhere. . . No pressure!

The life-sciences industry is embracing digital to unlock innovation. We spoke to ten digital leaders at global pharmaceutical companies to understand how they focus their efforts. The conviction that competitive differentiation will require effective digital initiatives has led many life-sciences companies to create a new leadership role, chief digital officer (CDO), to guide their digital initiatives. To understand how these leaders see the digital future and how they are managing for success, we spoke to CDOs and their equivalents at ten pharma companies. These conversations suggest three imperatives for digital efforts: focus on the team applying the tools, not on the tools themselves; make bold, disruptive bets; and optimize the portfolio of initiatives to achieve company priorities, while taking finite resources into account. Focus on teams and capabilities, not toolsLike most tools, digital technology becomes commoditized, so gains from early adoption tend to fade as technology becomes cheaper and more accessible. Thus, technology itself is unlikely to be a sustainable differentiator. “It is easy for businesses to jump to technology, to be enamored with the shiny objects and not focus on the problem [they are] trying to solve,” says Amy Landucci, global head of digital medicines at Novartis. Sustainable differentiation requires a focus on generating cutting-edge insights into the business and its possibilities. To that end, companies must build teams of people capable of generating such insights. The team, not the tool, is the vital element in digital success across industries.1 The team must have a suite of digital capabilities, including expertise in data science and multichannel management, experience deriving insights from real-world evidence, and a system of digital tools to complement traditional pharmaceuticals. Generating differentiating insights requires a cross-functional team that’s able to work across markets. Stay current on your favorite topicsSUBSCRIBE A team member needs to have “drive, good understanding of customer journeys and ability to identify the relevant innovative digital solutions leading to better healthcare outcomes. He/she needs to inspire the rest of the organization,” according to Betul Susamis Unaran, global head of digital at Ferring Pharmaceuticals. Other digital leaders say they seek individuals who want a job that is not purely technical, who can understand pain points and ways that digital technology can resolve them, and who can work with diverse members of the wider enterprise. These abilities are crucial, since “getting digital embedded in the business is just as difficult as figuring out where to focus,” says Francis Kendall, digital-strategy leader at Roche. The evolution of digital in the strategy of manufacturers creates this need for cross-functional teams. The next few years will likely see manufacturers’ focus shift from technology to design in order to ensure adoption of digital and analytics solutions inside and outside the enterprise. Several factors will fuel this shift. First, powerful digital and analytics platforms that enable faster and easier application development are emerging. For example, while deep learning analytics used to be the secret gardens of a few technology companies, open-source platforms like Alphabet’s TensorFlow can enable anyone (with solid mathematical skills) to develop innovative analytics. The impact of the analytical tools will depend on their reach, which will in turn depend on the creation of interfaces that enable lay users to leverage the analytics in their day-to-day work. Creating intuitive interfaces so executives, physicians, or patients can use—and help improve—the tools will be mostly a design and marketing challenge. Second, just as tech companies such as Apple and Fitbit have made user-centric design a significant source of digital value, life-sciences companies will embed design thinking into their approaches to the market. Many are realizing that differentiating through digital will require translating deep customer insights into solution designs that help patients and providers simplify their journeys or improve their outcomes. Would you like to learn more about our Pharmaceuticals & Medical Products Practice?Visit our Commercial page Finally, life-sciences companies are increasingly recognizing the need to overhaul their current approach to application development. Only a handful of the 160,000 healthcare applications available on iOS, for example, are used at scale. Similarly, pharmaceutical manufacturers are starting to realize that creating applications focused solely on their products will limit their impact. Most patients are polymedicated and require interoperable solutions. How many apps will a single patient use? The adoption challenge is huge and will require sophisticated teams that put digital and analytics at the heart of the business. Attracting such talent remains challenging, as multiple tech companies are venturing into life sciences. Companies in some industries admit paying digital executives more than the CEO, albeit on terms strongly linked to performance. The organizational structures within which teams operate will depend on their mandate. Philip Ma, vice president of digital health technology and data sciences at Biogen, says that a key question is whether the company’s strategy is “to enable the existing business or to create new businesses.” Most CDOs with whom we spoke are charged with enabling the development of digital solutions within the core of the business, so they have organized their teams to integrate closely with, and have influence on, business functions. But the rarer strategy of using digital to create novel business lines and revenue streams calls for designing the organization to be as unencumbered as possible by the current enterprise. Kristian Hart-Hansen, CEO of the LEO Innovation Lab, says that he wants to be like a “speed boat going out into open waters.” Otsuka Digital Health, a start-up created to commercialize a digital behavior-health platform, is similarly freestanding.2 Make bold, disruptive betsChange in today’s digital world is proceeding rapidly. The belief that digital change happens incrementally is dangerous and has contributed to the demise of many companies, including some with a rich technological history—such as Kodak, a technology leader that failed to keep pace with the rapid digitization of photography. A portfolio of digital initiatives should include bold, disruptive bets. Malika Mir, CDO at Ipsen, says that a key part of her role is “to make sure that the business understands digital is a game changer, that it will revolutionize how we do business.” Other industries offer valuable lessons for pharma. In some industries, digital has moderately realigned supply and demand in the market by exposing new supply (Airbnb) or by addressing unmet demand (streaming services that unbundle single songs from albums). In other industries, market dynamics have shifted radically, with companies reimagining products and services (as, for example, Amazon and Dropbox transformed storage products into a service) or hyperscaling platforms that blur traditional industry definitions and span multiple market segments (Apple, Google, and Tencent).3In banking, among other industries, traditional barriers to entry, such as regulatory control, have not prevented extreme market shifts—signaling risks for companies that ignore the need to make bold moves. While many pharma companies are launching game-changing initiatives to transform their core business, another option is to create a separate, self-sustaining entity for these efforts. LEO Pharma created Innovation Lab as an independent unit with multiyear funding to focus on nonpharmacologic digital solutions for patients with skin diseases. As CEO Hart-Hansen suggests, LEO Innovation Lab is shifting “from a pills company to a solutions company,” creating digital platforms and applications not necessarily tied to drugs. Initiatives fall into two key categories. A disruptive initiative inherently transforms a product or a customer experience (or the monetization of either). Conversely, an optimizing digital initiative improves the efficiency of a business or product more incrementally. The distinction is important. Disruptive initiatives require substantial change and create tension in the enterprise. Success metrics are rarely fiscal, especially in the early stages. These initiatives require multiyear investments and extensive capability building, and they have a higher risk of failure than optimizing initiatives. Optimizing initiatives often have a measurable return on investment. These “safer” initiatives are important, but too much attention to them can prove dangerous, as they can create a false sense of security. They consume the digital team’s time and effort but rarely mitigate the external risk of disruption to the enterprise. Optimize the portfolioFrom the many digital initiatives available to them, CDOs must choose those that will best serve the company’s priorities within its finite resources. Making the right choice requires setting the digital strategy, aligning initiatives with strategic goals, creating metrics for and prioritizing initiatives, and developing an operating model. Setting the digital strategy requires identifying how digital technology can help redefine the business (that is, the use cases). This step ensures focus on addressing the needs of the enterprise, with less focus on the technology itself. “Technology is here to facilitate a business,” says Marcello Damiani, chief digital officer of Moderna Therapeutics. “If you don’t understand your business, you can’t apply your technology.” Then the CDO needs to inventory initiatives and align them with the use cases. Except for a new or small company that is “planting its initiatives in a green field,” most companies have existing initiatives that have arisen organically within the enterprise. A closer look at these initiatives often finds opportunities to combine some by use case. Philip Ma of Biogen, for instance, has reorganized multiple small analytics and data-science initiatives to take advantage of their interdependencies in helping the company get better at forecasting. Next, the CDO needs to define metrics for success, as a basis for prioritizing initiatives. The right metrics depend on the type and scope of the initiative. CDOs agree that a financial-output metric such as return on investment is not necessarily well suited to disruptive initiatives in their early stages (or ever, in many cases). In the early stages, measures appropriate to a specific use case, such as increased customer adoption or shorter recruitment time, are generally more appropriate. Most also use a second metric, such as degree of alignment or likelihood of implementation, to reflect the desire and ability to execute an initiative—underscoring the importance of change management in deploying digital. Combining these metrics with resource requirements is an effective way to prioritize initiatives. Some CDOs discover that their portfolio focuses too heavily on technology like apps or analytics. Others see that they lack the capability4or team for effective execution. Finally, the CDO must develop an operating model. A common impediment to successful deployment of digital initiatives is the company’s traditional way of working. Established pharmaceutical companies typically make decisions meticulously, and often slowly. As a result, the CDOs we interviewed recognize the need to develop new operating models that enable rapid building, testing, and learning—an agile or lean-start-up model, for example. The goal is to swiftly deepen understanding of the customer or use case and learn from failed experiments. For instance, one company recently developed a new pricing and contracting tool for medical-device representatives. Instead of modifying the core analytical engine embedded in a complex legacy system, it deployed a new cloud-based solution, initially using simple outputs from the legacy system. Believing that the tool was directionally correct, the company piloted and refined it with field representatives. It gradually developed a full solution to embed in the enterprise system, but it benefited from the impact of the initial solution in the meantime. How pharma can win in a digital worldRead the article The status quo is often deeply rooted in large pharma companies, and this can hamper the effort to create a build-test-learn operating model. For example, team members often have difficulty accepting the failures that inevitably happen when testing and iterating a nascent initiative. Some CDOs tackle such issues by asking senior management to realign employees’ performance metrics. Others recruit individuals from technology firms and start-ups, where the build-test-learn approach is part of the company culture. “It’s OK to fail,” says Michael Russo, executive director of digital strategy and innovation of Acorda Therapeutics, “but fail quickly and learn from the mistakes.” Role modeling by leaders—for example, when an executive describes his or her own failures and the lessons learned—can also help shift the culture. A crucial part of the new operating model is an approach to knowledge management. Malika Mir of Ipsen, for example, has established processes to record all initiatives in a central database in order to track them and share knowledge from successful and failed initiatives across the global organization. This has the added benefit of providing a means of tracking initiatives. Deployment of resources is equally important. In the early stages of an initiative, when the potential for failure is high, use of resources needs to be limited without extinguishing innovation. “If tests show the project is good and we see a business case, then we go to beta phase and scale up,” says Hart-Hansen of LEO Innovation Lab. One CDO speaks of putting “guardrails” around the resources devoted to initiatives, while empowering leaders to allocate the resources as they see fit. CDOs can play a key role in guiding life-sciences companies through the disruption of digital technology and reaping its rewards. Successful CDOs build teams that can generate insights from digital tools and have the courage to make bold, disruptive bets. These leaders also create a portfolio of initiatives that match company priorities and make the organizational changes needed to execute those initiatives successfully. In an end state where digital is fully embedded in the business, the successful digital leader may be faced with the dilemma of his or her position becoming redundant. At its best, the CDO is thus an agent of transformation, and the epitome of selfless leadership. About the author(s)Amy Hung is a senior expert in McKinsey’s New Jersey office, Olivier Leclerc is a senior partner in the Southern California office, and Travis Murdoch is a consultant in the Silicon Valley office.

Linda Holroyd's insight:

The role of the CDO in Pharma - what a concept!

acquista-depalgo-online's curator insight,

March 25, 2024 1:31 PM

Gibson's curator insight,

June 20, 2024 12:07 PM

https://chaojiyaowu.com/

https://perderepesoefedrina.com/

The case for digital reinvention

Linda Holroyd's insight:

What's the bottom-line impact for adopting a digital strategy?

Slow economic growth is the mantra of political campaigns and economic angst. Growth in economic output per hour (“labor productivity”) achieved an annual pace of 3 percent for a full half-century between 1920 and 1970. Since 1970 that rate has slowed to about 1.5 percent, and in the last six years productivity growth has slowed further to a lamentable 0.5 percent annual rate. My book The Rise and Fall of American Growth attributes this enormous contrast between rapid growth in 1920-70 and slow growth after 1970 to the basic nature of inventions. Growth in the middle of the 20th century was propelled by the invention in the late 19th century of electricity, the internal combustion engine, the telephone, chemicals and plastics, and the diffusion to every urban household of clear running water and waste removal. America made a transition from 50 percent of the working population on farms to a largely urban nation, and the drudgery of household work – carrying water in and out, doing laundry on a scrub board – made a transition to modern bathrooms and kitchens by the 1950s. The digital revolution associated with computers has since 1960 dominated the sphere of innovation, as office work transitioned from the typewriter and old-fashioned calculator to the new world of personal computers, spreadsheet and word processing software, the internet, and search engines. But the impact of this revolution in boosting productivity growth lasted only one decade (1995-2005), a much shorter impetus than occurred earlier in the century when productivity growth achieved its 3 percent annual pace for five decades from 1920 to 1970. Why? The computer revolution altered office work but did not extend into everyday life as had the earlier inventions that brought us electricity, motor vehicles, and the modern kitchen and bathroom. Smart phones were introduced by Blackberry in 2003 and by Apple in 2007, but their uses are primarily to boost consumer enjoyment through social networks and game-playing, not a part of the market economy that creates jobs and pays wages. Why has productivity growth been so mediocre, a 0.5 percent annual pace since 2010? In my view this has occurred because most of the benefits of the digital revolution were over by 2005. Everywhere you look, from corporate offices to check-in desks at doctor, dentist, and veterinarian offices, the equipment on the desks is the same as in 2005, as is most of the software. This slackening of the pace of economic growth due to the minor impact of new innovations has both a pessimistic and an optimistic aspect. Slow productivity growth dampens the ability of business firms to provide wage increases to their workers. But slow productivity growth also means that steadily growing output continues to provide new jobs, 15.5 million of which have been created in the U.S. since early 2010. But how can so many jobs be created in a world of technological hype of robots taking over the economy? Aren’t robots about to decimate jobs, throwing half the population out of work as has been predicted to occur over the next decade by the two Oxford economists in 2013, Carl Frey and Michael Osborne? Robots are nothing new; the first industrial robot was introduced by General Motors in 1961, and by the mid-1990s robots had a major role in automobile factories, welding together body parts and freeing human workers from the noxious fumes of the auto paint shop. But robots have made little impact outside of manufacturing. Even Amazon’s high-tech warehouses use robots just to move shelves to human workers, who hand-select the items to be shipped as well as the packing material, and pack the shipments by hand. But outside of manufacturing and wholesale warehouses, robots are hard to find. I play a game called “find the robot.” In my daily strolls in and out of supermarkets, restaurants, doctor and dentist offices, my nearby hospital, offices in my own university, and the vast amount of employment involving elementary and secondary teachers, personal trainers, and old age caretakers, I have yet to find a robot. In my journeys, the closest thing I have found to the introduction of a robot in the service sector is that in a local casual dining restaurant, there are kiosks on the tables to allow patrons to pay their bills without human intervention. But offsetting that is the fact that my local supermarket recently removed its self-checkout electronic kiosks to be replaced by human express checkout agents, apparently due to excessive fraud as customers slid expensive items by the dumb credulity of the self-checkout kiosks. The Frey and Osborne pessimism about jobs is total fiction. They predict over the next decade that 55 percent of airline pilot jobs will be eliminated. Sorry, but government regulations require two pilots in a commercial aircraft, and a switch to one pilot per aircraft is nowhere in sight. They predict that 92 percent of retail checkout clerk jobs will be eliminated, but there is no robot-like replacement of retail clerks in sight beyond the 30-year-old invention of bar-code scanning. Surely multiple-function robots will be developed, but it will be a long and gradual process before robots outside of manufacturing and wholesaling become a significant factor in replacing human jobs in the service, transportation or construction sectors. And it is in those sectors that the slowness of productivity growth is dragging down the economy’s overall performance. My book concludes that the rapid economic growth of the mid-20th century cannot be repeated. Those “Great Inventions” were too important and too pervasive to happen again anytime soon. But let us not forget, the corollary of slow productivity growth is the rapid creation of jobs, as we have witnessed in the last six years and will enjoy for the foreseeable future. Robert J. Gordon is professor in social sciences at Northwestern University and the author of The Rise and Fall of American Growth, one of six books on the shortlist for the 2016 Financial Times and McKinsey Business Book of the Year Award, to be announced Nov. 22.

Linda Holroyd's insight:

The 3%+ economic growth between 1920 and 1970 was sparked by inventions and innovations that transitioned us from urban living to modern bathrooms and kitchens by the 1950. Most of the benefits of the digital revolution started in 1960 were over by 2005, and we have witnessed slower productivity growth of 1.5 and even .5 percent since 1970. However, this does not discount the rapid creation of jobs we've witnessed in the last six years and will enjoy for the foreseeable future.

by Reenita Das , CONTRIBUTOR Opinions expressed by Forbes Contributors are their ownSource: Frost & Sullivan Here are the top five ways that Frost & Sullivan’s transformational health program analysts predict diabetes management will change in the future. Mandatory Screening Current global statistics on diabetes diagnosis are grim–1 in 2 diabetics remains undiagnosed. A primary challenge to overcome this issue lies in the gold standard for diagnosis–fasting and random blood glucose levels. However, this is set to change with the arrival of non-invasive methods to predict diabetes risks. The Scout DS system by Miraculins is one such device. Using visible light to assess skin diabetes biomarkers (like the Advanced Glycation End-Products) on the forearm, the system throws out a diabetes score in 90 seconds. If the score is high, the patient is referred to a specialist for additional tests and consultation. The non-invasive, quick, no-fasting, no-bloodwork system means you could be getting screened for diabetes during your next annual physical checkup at your general physician’s office. Nutrigenomic Profiling Every individual is different when it comes to metabolic rates, exercise capabilities, tendencies to put on weight or stay lean, inclination to eating sweets, predisposition to diabetes and so on, courtesy of DNA. But now, we have the ability to sequence our DNA and have access to what is known as the individual nutrigenomic profile. The modern science of nutrigenomics combines nutrition and genetics, enables individuals to know how food constituents interact with their genes at molecular levels, and contributes to the disease. This knowledge can help diabetes prevention, or assist diabetics in better managing their disease. Don’t be surprised to see a diabetic person armed with a food scanner (like TellSpec or DietSensor) assessing his restaurant dish and dessert against his nutrigenomic profile Non-Invasive Monitoring The “holy grail” of diabetes monitoring is non-invasive glucose monitoring that can end pricking fingers for testing several times a day. There are several approaches being developed; broadly, these could be categorized based on where monitoring occurs–eyes (tear drop), fingertip, earlobe and saliva. Apart from big names like Google and Novartis involved in making such monitoring products a reality, there are also smaller players like Medella Health, LighTouch Medical and Quick LLC. Approaches include contact lenses, passing light (visible, infrared or other) through the skin to detect glucose and even salivary assessments. So the next time you are talking to a diabetic person and their contact lens turns a bright color (an indicator for hypoglycemia), get them a chocolate pronto. They will thank you! Background Therapy Of course, a potential “cure” for diabetes is replacing pancreatic β cells with stem cell-derived, lab-grown cells. But the current focus of the industry is the artificial pancreas–although we have Medtronic’s MiniMed 670G as the first of this category, we are likely to see many more advances in this area. Competitors like BigFoot Biomedical, Dexcom and Animas Corporation are also developing similar systems. What these essentially mean is freedom from daily monitoring glucose levels, guesstimating appropriate insulin dosages and injecting them. Another advance that will change the field is being developed by Sensulin and other major pharma companies like Eli Lilly–glucose-responsive, once-a-day insulin that could potentially replace basal and prandial insulin. While this insulin still would be taken once a day through the same insulin pens or other delivery devices, the release of insulin in the body would be controlled by blood glucose levels alone, controlling these levels far better than regular insulin delivery. Overall, diabetics would now be able to live worry-free–either injecting insulin only once a day, or simply letting the artificial pancreas system take over completely, improving the overall quality of life. Your diabetic friend might just stop carrying her glucometer, test strips, lancets, insulin pen and chocolates (or maybe not chocolates). Analytics And Artificial Intelligence A future diabetic person will have their genomic information incorporated in to their diabetes management regimen. Big Data analytics will play a very important role in informing the patient (not the caregiver!) what they should eat, how much they should exercise and how to manage the disease–in real time. An artificially intelligent interface will “communicate” with the user. For example, the a distant-future system might tell the patient (based on her past history, genetic predisposition and today’s diet and activity levels): “If you have that particular dessert now, it will cause your glucose levels to shoot up, necessitating immediately performing activities like jogging to burn approximately 150 calories or an insulin injection of 0.5 units. Please select your choice–jogging or automatic insulin delivery” (numbers are hypothetical). Does this mean now is the best time for diabetics? We are definitely along the way to finding a cure for this disease, but until then, advances in technology will surely make the life of a diabetic person much easier. Are you a diabetes patient advocate or an entrepreneur? We would love to hear your opinions on what you think will be the future of diabetes care. This article was written with contributions from Siddharth Shah, Research Analyst and Venkat Rajan, Global Director, both from the Visionary Health program of Frost & Sullivan’s Transformation Health practice.

Linda Holroyd's insight:

How science and healthcare will make it easier for those who suffer from diabetes

Published on November 9, 2016

Linda Holroyd's insight:

Interesting perspective on why the election predictions of the majority were wrong

Every now and then, it’s a fun and healthy challenge to think distantly. Sure, we already expect self-driving cars, wearable hardware, a connected home, and augmented reality. But where does the foreseeable future take us next? I’m talking more Black Mirror than investor thesis. What new problems will we be struggling with? What will kill us? What will connect us? While solutions change, some questions will always remain. If only to stimulate discussion among friends, here are a few ideas on my mind these days:

Allow me to explain, as well as share some implications for each: (1) Social media will become passive.The concept of actively “posting” or “sharing” will be frowned upon and entirely replaced by a passive stream of your life’s experiences, whereabouts, and media consumption. Imagine a 24 hour channel of you that is authentic, aways live (or automatically programmed), and always accessible to your friends (or if you’re born in the age of transparency (post year 2000), accessible to anyone). Any effort to actively post something will be seen as “manual editing” and will be perceived negatively unless it is an artistic statement. Quality will be community and algorithmically-determined, surfacing the highlights of your experience in a way that is automatic and thus deemed more authentic. Implications?

Personally, I’m more bullish about augmented reality than virtual reality. The augmented layer opens up a ton of exciting (and horrifying) ways for brands, friends, governments, and artists to get in your line of sight based on where you are and when you’re there. Quite quickly, I see it getting out of hand. While the physical world has practical limitations that keep billboards at bay, the augmented world won’t. To get a feel for how bad this could be, check out this video. Implications?

A few years ago I shared my excitement for the “interface layer: where design commoditizes tech,” and how superior interfaces will aggregate multiple services underneath. In the future, we will want fewer interfaces in our lives — and these interfaces will integrate all sorts of utilities into a simple flow. Examples?

The biggest implication of the emerging interface layer is ruthless competition to be the default. The utility-based providers underneath these interfaces will be pressed on margins and will compete to be the default provider in the interfaces we use on a daily basis. To survive, the providers will focus more on optimizing the cost-efficiency of their services rather than spending money building their brand and relationships with customers. (4) Autonomous vehicles in cities will become a public utility.When (not if) all transportation within a city’s limits becomes automated and increasingly regulated, cities will rethink infrastructure and public transportation. Some cities already see Uber as a solution to “last mile” transportation quandaries. Perhaps planning and scheduling software for public transportation becomes more important than the commoditized technology in the vehicles themselves. Perhaps transportation will join the ranks of water and electricity? Implications?

The “tragedy of the commons” is the unfortunate human tendency to take advantage of shared-resources out of self-interest, thus depleting the benefits everyone could enjoy through collective action. Back in the day, farmers would take their livestock and selfishly deplete the town commons before returning to their own lands (which they would sustain thoughtfully). If everyone just agreed to graze the commons sparingly, it would last and benefit everyone. But self-interests obstruct the common good. People who abuse insurance spike prices for the rest of us. People who cheat taxes cause the rest of us to pay more. Through increased transparency, networks, and artificial intelligence, technology will enable us to collectively regulate and align our interests. Implications?

Forecasts for the future are not an investment thesis. The future won’t happen until the present is ready for it. One of the things I’ve learned from the partners at Benchmark is just how important it is to invest with a tremendous insight into the present. But for a seed investor, product leader, or entrepreneur, forecasts for the future add a new lens to pattern recognition. Aside from what I look for in a founder, team, and product, I try to determine whether the future is a headwind or a tailwind for a company. Is the team attempting to defy a likely outcome or make it happen in a better way? If nothing more, considering the future exercises our imagination and sparks conversation and debate with people you can learn from. Bring it.

Linda Holroyd's insight:

5 Forecasts: Social media, augmented reality, UIs, autonomous vehicles a 'tragedy of commons'

When I read the other day that the Honest Company, founded in 2011, was likely to be acquired by a large, established consumer packaged goods (CPG) company for nearly $2 billion, I initially was surprised. As a fan of the brand and its creator, Jessica Alba, my wife was not. After all, she pointed out, Alba started the company based on what she herself had experienced as a new mother: the need for a trusted supplier of safe, eco-friendly products for babies.

Linda Holroyd's insight:

It's about service and excellence. It's about brand. WTG Honest Company!

McKinsey Transforming operations management for a digital world October 2016, By Albert Bollard, Alex Singla, Rohit Sood, and Jasper van Ouwerkerk

When combined, digital innovation and operations-management discipline boost organizations’ performance higher, faster, and to greater scale than has previously been possible.In every industry, customers’ digital expectations are rising, both directly for digital products and services and indirectly for the speed, accuracy, productivity, and convenience that digital makes possible. But the promise of digital raises new questions for the role of operations management—questions that are particularly important given the significant time, resources, and leadership attention that organizations have already devoted to improving how they manage their operations.At the extremes, it can sound as if digitization is such a break from prior experience that little of this history will help. Some executives have asked us point blank: “If so much of what we do today is going to be automated—if straight-through processing takes over our operations, for example—what will be left to manage?” The answer, we believe, is “quite a lot." More digital, more human Digital capabilities are indeed quite new. But even as organizations balance lower investment in traditional operations against greater investment in digital, the need for operations management will hardly disappear. In fact, we believe the need will be more profound than ever, but for a type of operations management that offers not only stability—which 20th-century management culture provided in spades—but also the agility and responsiveness that digital demands. The reasons we believe this are simple. First, at least for the next few years, to fully exploit digital capabilities most organizations will continue to depend on people. Early data suggest that human skills are actually becoming more critical in the digital world, not less. As tasks are automated, they tend to become commoditized; a “cutting edge” technology such as smartphone submission of insurance claims quickly becomes almost ubiquitous. In many contexts, therefore, competitive advantage is likely to depend even more on human capacity: on providing thoughtful advice to an investor saving for retirement or calm guidance to an insurance customer after an accident. That leads us to our second reason for focusing on this type of operations management: building people’s capabilities. Once limited to repetitive tasks, machines are increasingly capable of complex activities, such as allocating work or even developing algorithms for mathematical modeling. As technologies such as machine learning provide ever more personalization, the role of the human will change, requiring new skills. A claims adjuster may start by using software to supplement her judgments, then help add new features to the software, and eventually may find ways to make that software more predictive and easier to use. Acquiring new talents such as these is hard enough at the individual level. Multiplied across an organization it becomes exponentially more difficult, requiring constant cycles of experimentation, testing, and learning anew—a commitment that only the most resilient operations-management systems can support.Seizing the digital momentAnd if digital needs operations management, we believe it’s equally true that operations management needs digital. Digital advances are already making the management of operations more effective. Continually updated dashboards let leaders adjust people’s workloads instantly, while automated data analysis frees managers to spend more time with their teams. The biggest breakthroughs, however, come from the biggest commitment: to embrace digital innovation and operations-management discipline at the same time. That’s how a few early leaders are becoming better performers faster than they ever thought possible. At a large North American property-and-casualty insurer, for example, a revamped digital channel has reduced call-center demand by 30 percent in less than a year, while improved management of the call-center teams has reduced workloads an additional 25 percent. Achieving these outcomes requires organizations to tackle four major shifts. Digital and analog, reinforcing each other Digitization can be dangerous if it eliminates opportunities for productive human (or “analog”) intervention. The goal instead should be to find out where digital and analog can each contribute most.That was the challenge for a B2B data-services provider, whose customized reports were an essential part of its white-glove business model. Rather than simply abandon digitization, however, the company enlisted both customers and frontline employees to determine which reports could be turned into automated products that customers could generate at will.Working quickly via agile “sprints,” developers tested products with the front line, which was charged with teaching customers how to use the automated versions and gathering feedback on how they worked. The ongoing dialogue among customers, frontline employees, and the developer team now means the company can quickly develop and test almost any automated report, and successfully roll it out in record time. Driving digital, enterprise-wide Developing new digital products is only the beginning, as a global bank found when it launched an online portal. Most customers kept to their branch-banking habits—even for simple transactions and purchases that the portal could handle much more quickly and cheaply. Building the portal wasn’t enough, nor was training branch associates to show customers how to use it. The whole bank needed to reorient its activities to showcase and sustain digital. That meant modifying roles for everyone from tellers to investment advisers, with new communications to anticipate people’s concerns during the transition and explain how customer service was evolving. New feedback mechanisms now ensure that developers hear when customers tell branch staff that the app doesn’t read their checks properly.Within the first few months, use of the new portal increased 70 percent, while reductions in costly manual processing means bringing new customers on board is now 60 percent faster. And throughout the changes, employee engagement has actually improved. Realigning from the customer back The next shift redesigns internal roles so that they support the way customers work with the organization. That was the lesson a major European asset manager learned as it set out on a digital redesign of its complex, manual processes for accepting payments and for payouts on maturity. The entire organization consisted of small silos based on individual steps in each process, such as document review or payment processing—with no real correlation to what customers wanted to accomplish. The resulting mismatch wasted time and effort for customers, associates, and managers alike. The company saw that to digitize successfully, it would have to rethink its structure so that customers could easily move through each phase of fulfilling a basic need: for instance, “I’ve retired and want my annuity to start paying out.” The critical change was to assign a single person to redesign each “customer journey,” with responsibility not only for overseeing its digital elements but also for working hand in glove with operations managers to ensure the entire journey worked seamlessly. The resulting reconfiguration of the organization and operations-management systems reduced handoffs by more than 90 percent and cycle times by more than half, effectively doubling total capacity. Making better leaders through digital The final shift is the furthest reaching: digital’s speed requires leaders and managers to develop much stronger day-to-day skills in working with their teams. Too often, even substantial behavior changes don’t last. That’s when digital actually becomes part of the solution.About two years after a top-to-bottom transformation, cracks began to show at a large North American property-and-casualty insurer. Competitors began to catch up as associate performance slipped. Managers and leaders reported high levels of stress and turnover. Speed and scale: Unlocking digital value in customer journeys A detailed assessment found that the new practices leaders had adopted—the cycle of daily huddles, problem-solving sessions, and check-ins to confirm processes were working—were losing their punch. Leaders were paying too little attention to the quality of these interactions, which were becoming ritualized. Their people responded by investing less as well. Digital provided a way for leaders to recommit. An online portal now provides a central view of the leadership activities of managers at all levels. Master calendars let leaders prioritize their on-the-ground work with their teams over other interruptions. Redefined targets for each management tier are now measured on a daily basis. The resulting transparency has already increased engagement among managers, while raising retention rates for frontline associates. Organizations investing in human and digital capabilities can start by asking themselves several critical questions:

Capturing the digital opportunity will require even greater operations-management discipline. But digital also makes this discipline easier to sustain. Adding the two together creates a powerful combination.

About the author(s)

Linda Holroyd's insight:

Combine digital innovation and operations management

Recently, while vacationing in Tuscany, we hired a driver and we went wine tasting. Our first stop was the most famous winemaker Antinori Family. Gorgeous, newly designed winery, but from the moment we walked in, the vibe was unwelcoming. The receptionist did not greet us, the wine pourers in the tasting room had total attitude and were not interested in either engaging with us nor describing the wines we were tasting. Besides that, each small tasting was expensive! Disappointed, we departed with no wine in hand and hurried on to visit a few other good wineries in the picturesque area. Our most memorable stop by far was at the Tenuta Tociano winery in San Gimignano. To our pleasant surprise, the owner Pierluigi greeted us at the gate with an umbrella while wearing an apron and boots (it was raining heavily). He introduced himself, made sure he knew our names, where we were from and then proceeded to escort us to a small table which was loaded with empty wine glasses and cheese/salami plate for the tasting. ( I later found out that he makes sure he greets or speaks with everyone that visits his winery.) Pierluigi gave us the background on his wine and all the awards they won from Wine Spectator. More importantly, however, he was also charming enough to tell us all that awards don't matter because wine preference is a matter of taste and he did not want us to feel compelled in any way to prefer one wine more than the other due to its "high" ratings. He then introduced his nephew, who spent the next few minutes entertaining and educating us with some tasting techniques. He had us all swishing the wine around and practically gargling on it. Interesting enough, everyone in the room was laughing and smiling and feeling awkward together. On the table, they had a paper placemat and a pen to identify which wines you preferred and cleverly, on the back of the placemat, a handy order form to purchase the wines we had just tasted, as well as a spot to put your contact info to join their exclusive online community and hear about their stateside wine tasting events. As a veteran marketer and sales person, I totally appreciated the marketing and true salesmanship of this small winery. These were my takeaways that apply to any business, whether you are a 700-year-old winery, or any company doing business today. 1- Greetings Matter (first impressions)! You can have the slickest website or coolest office ever, but you must find a way to also make people feel welcome, whether it's in your place of business or your website. Do not be indifferent! 2- Be Generous. Educate and give people information that pertains your industry for free. Much like the winemakers' nephew who spent time teaching us how to properly taste wine from awkwardly sticking your nose in the glass to swirling in our mouths, he taught us about the differences in Chianti grapes and educated us on the difference between a Chianti, Reserva or a super Tuscan. What is your place of business doing to educate or give information or content for free? this builds loyalty immediately. They were extremely generous in their pouring, which built instant loyalty and yes a wine buzz. 3-Create a Community: Figure out a way to make your prospect be a part of your community. During our visit, we were encouraged to sign up and be part of a Tuscan wine lovers community with wine articles, videos and discounted wine with free shipping to the US. There are thousands of wineries in the Chianti region but this winery figured out a way to get us to be an advocate, a member and potentially a long time shopper. One of my favorite go-to resources for great tips on building and nurturing a successful community to grow your business (www.jeffbullas.com) . People interactions matter. Honestly, I bought Chianti wine on our trip based on how sellers engaged with me during the wine tasting (yeah this proves I am not a wine connoisseur.) It's similar to any business, the product itself must be good, but the sales interactions and the customer service portion of the business are vitally important. It isn't sufficient to have just slick packaging or a gorgeous website, your people interactions and how your company makes prospects and customers feel matter more that you realize. Scott McKain's book Collapse of Distinction: has some great practical advice and some entertaining examples of how much customer service matters. We now live in an attention-based economy. When we are lucky enough to have our customers/prospects attention that's when need to be authentic and engaged. So pour that glass of chianti and ask yourself what am I doing to make my customers feel appreciated and feel satisfied that they are getting good value from your products and services.

Linda Holroyd's insight:

Greetings Matter, Be Generous, Build Community

New insights for new growth: What it takes to understand your customers today

Linda Holroyd's insight:

Tangible suggestions on how to better and more deeply listen to and connect with customers

FountainBlue’s September 2 VIP roundtable was on the topic of Embracing the Age of Personalization. Please join us in thanking our gracious hosts at Hitachi. The executives in attendance at this month’s roundtable represented a wide range of industries, roles, functions and company sizes. Therefore, their perspectives on who the customer is, what the customers’ needs are, and how best to address them varied widely. Below is a compilation of their collective thoughts regarding serving the needs of the customer.

Here are some predictions from our group of execs:

Resources:

Linda Holroyd's insight:

What would *you* do differently if customers were your true north?

|

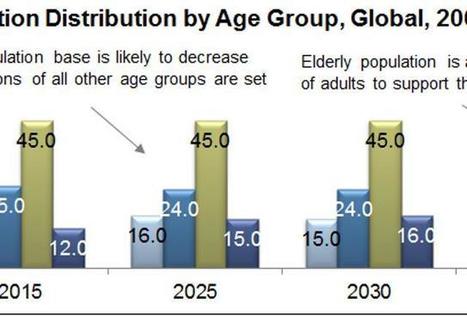

Is Healthcare becoming a Data-driven Science led by Clinicians? The current model of sick care is undeniably unsustainable due to a number of compelling reasons. The aging population burden tops the list. The United Nations’ World Population Aging Report paints a grim picture for the future (see Figure 1) – from 2025 and beyond, the proportion of the elderly population (aged 60 and above) is set to rise, while the share of the working adult population to support this elderly population is expected to remain constant, and even to drop after 2030.

Disconnect Between Healthcare Spending and Patient Outcomes At the same time, the world will continue to grapple with a significant disconnect between health spending and actual patient outcomes. Consider the parameter of life expectancy (see Figure 2, sourced from Our World in Data). As expected, the U.S. is an outlier, but even in other developed nations such as Switzerland and Norway, where health expenditure is higher than the other countries it still does not result in a proportionate increase in life expectancy – some nations actually spend less and yet achieve similar life expectancies. Figure 2: Life Expectancy vs. Health Expenditure, 1970-2013 Clearly, the present healthcare situation is economically unsustainable. But more importantly, this situation is set to get worse with an increasing aging population that demands more care services and hence higher healthcare expenditure. The importance of wellness and prevention becomes even more critical in this current situation. Less than 50 percent of Medicine is Evidence Based and Lacks Accuracy and Continuity Defining the Nexus of Disease Prevention and Treatment with Health Analytics In a heightened era of population health analytics and continuous and interoperable digital health information, the practice of medicine is becoming more and more of an art form and less of a scientific process. A doctor’s education, clinical experience and intellectual instinct may never be entirely replaced by machine learning or AI software. But, recent health information technological and life sciences advances are making it more and more possible to overcome several current challenges. Physiological function sensors are becoming commoditized, and along with wireless communication technologies, the Internet of medical things approach to care is poised to take hold in the delivery of healthcare in the U.S. Figure 3: Medical Practice transformation, Select Providers, who have historically been at the epicenter of all things medicinal, are being asked to engage with an ever growing onslaught of sophisticated and highly functional digital assets. Today’s physicians are being presented with unprecedented real-time access to medical databases in a cloud environment that hold, literally, the entire history of clinical care, symptomatology, 3D images of tumors, diagnosis and prognosis for every conceivable rash or physical malady known. What modern medicine is to do with this information is not yet clear. Presently, a redefining of the processes and practices of medicine are being explored with amazing innovations driven by an over-arching quest for improved quality outcomes. Frost & Sullivan Make no mistake — the paradigm of the traditional doctor patient relationship is shifting from one of 100% reliability on the physician to drive practically every aspect of care to one of virtual and digital collaboration along the continuum of health analytics across the entirety of the care ecosystem. Additionally, millennials prefer to see doctors virtually rather than face to face which will accelerate this trend. This Darwinian step of medical practice evolution has led to the discovery of a unique opportunity to shift even further the paradigm of medicine to one of understanding the underlying precursors to all forms of disease by statistically performing a multi-variate regression analysis for every dependent variable in our environment. The results of which, when arrayed in rank order by coefficient of correlation (r²) reveals in conjunction with genomic data which specific chronic and degenerative disease threats pose the greatest health dangers for each particular individual. Similarly they also show what the precursors to these diseases will be, where and how to monitor them, and how to prevent the onset of these very same debilitating diagnoses. Figure 4: Maturity levels for automation in healthcare