Investment EuropeFocus on smart beta: investors apply smart beta approach to bondsInvestment EuropeThis is where smart beta solutions come in.

Your new post is loading...

Your new post is loading... Your new post is loading...

Your new post is loading...

Investment EuropeFocus on smart beta: investors apply smart beta approach to bondsInvestment EuropeThis is where smart beta solutions come in.

No comment yet.

Sign up to comment

Beating the market sounds great, but may not always be a great outcome (Smart beta offers fresh alternatives for the brave http://t.co/Jq6GAKb3 #equity #pensions John Belgrove #AonHewitt...)...

Active managers are feeling the pressure as money flows from active managed funds into strategy indices, as so-called “smart beta” gains traction.According to one exchange-traded fund provider, who wished not to be named: “Quantitative index...

PowerShares has brought us something very new, and I think the fund is going to be a big hit.

The low volatility anomaly is getting some serious press these days. Historically that has not always been a good sign for future performance.

Newscape Capital Group's Richard Bonnor-Moris says that he likes smart beta products as they do exactly what you expect and are beneficial ...youtube.com...

A growing understanding of the composition of hedge fund returns is letting investors capture the return streams of hedge funds through systematic exposure to persistent risk premia (returns above the expected risk-free rate of return).

This provides investors with diversification away from equity market risk in a low-cost, liquid and transparent manner, but without the downsides of investing in a hedge fund.

The ETF firm is adding emerging markets and developed ex-U.S. ETFs to its roster.

Five years ago, who would have predicted that the rich world would reprise the Great Depression?

The strategy is gaining influential adherents, mainly among institutions, but hasn't caught on with individuals. Will this strategy work in the future? Could an individual investor apply it? I think the answer is, tentatively, yes to both questions. To understand why risk-parity works, we have to revisit a common fundamental misconception of portfolio construction.

The typical investor thinks of assets as being like indivisible elements, with distinct characteristics. In contrast, the risk-parity approach begins with the observation that asset classes can be described in much the same way atoms can be described as combinations of electrons, protons, and neutrons. The fundamental particles in the risk-parity view of the world are inflation and economic growth. This isn't a modern insight, but one that's been around academia for decades. The risk-parity application is relatively new, however.

It was all so simple: diversify and sit back. But the investment strategy pursued by so many – now underfunded – pension fund managers hoping for a steady stream of returns has not worked.

Historically low interest rates, an appearance of diversification when funds actually held different flavours of equity – be it public, private, foreign or supposedly hedged – as well as poor active management have all contributed to the strategy’s failure. The indiscriminate selling of the financial crisis exposed the flaws of diversification.

Seeking performance while at the same time increasingly needing to control risk makes smart beta thematic index approaches such as low volatility, minimum variance and risk-weighted strategies increasingly appealing to institutional investors allocating back into commodities

The interest in smart beta investment strategies is strong and growing - and evidence suggests smart beta tools are able to offer superior returns, says David Blitz, head of quantitative research at Robeco.

|

Smart beta concept to combat investment cost challengeInvestorDailyAccess to exposures and markets that are not available off the self from a passive manager is anticipated to have a huge impact on the industry over the next 10 years.

Appetite rises for alternative indicesFinancial TimesAn increasing number of investors are moving away from traditional market capitalisation-based indices to alternative strategies, known as smart beta, in search of better returns and lower costs...

Investors need to ensure they shift their asset allocation as regimes change.

PowerShares marries two of the hottest trends in the ETF market into one single wrapper.

Mean-variance investing is all about diversification. Diversification considers assets holistically and exploits the interaction of assets with each other, rather than viewing assets in isolation. Holding a diversified portfolio allows investors to increase expected returns while reducing risks. In practice, mean-variance portfolios that constrain the mean, volatility, and correlation inputs to reduce sampling error have performed much better than unconstrained portfolios. These special cases include equal-weighted, minimum variance, and risk parity portfolios.

Since the first market capitalisation-weighted ("cap-weighted") equity index was introduced by Standard & Poor's in 1923, cap-weighted indexing has become the dominant form of index investing. Today, cap-weighted indices account for the vast majority of assets in index-linked investment products such as ETFs and index funds, as well as trading volumes in exchange-traded and over-the-counter ("OTC") index futures, options and other derivatives.

In recent years, there has been a proliferation of alternatively weighted indices, such as fundamentally weighted indices, equal-weighted indices, and low-volatility indices. Correspondingly, there have been increased debates about the role of alternatively weighted indices (or "alternative beta") in investment portfolios.

Passive investing is enjoying an unprecedented period of popularity as growing numbers of institutional and retail investors discover that exchange traded funds and other index-based products are vital tools for building robust portfolios.

Money manager looks to add six new funds to its suite of smart-beta funds.

For the past 25 years, the asset allocation pie chart has been the most prominent and widely used tool in financial planning. Type in your age, some basic income and risk tolerance information and out comes a recommended formula for how much money you should have in stocks, bonds and cash.

In response to the imperfections of investment approaches based on market capitalisation indices, the fund industry has come up with many solutions based on more efficient indices over the last few years. Several strategies have been developed, all sharing the objective of reducing the level of portfolio risk to achieve the best possible control over performance.

Low volatility/minimum variance, risk weighted approaches, equal weighted portfolios, fundamental indexation and so on. Whether they follow an efficient index (MSCI Equal Weighted, FTSE RAFI, FTSE 100 Minimum Variance, S&P 500 Risk Control Indices) or seek to achieve additional return by playing on market anomalies (small/mid indices), so-called "beta efficient" strategies are already used in Europe by most Dutch, Belgian and German pension funds.

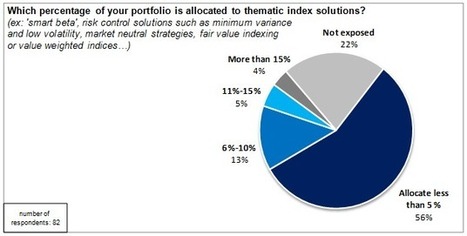

This trend is expected to spread. One third of international institutional investors expect to devote over 10% of their portfolio to efficient index investment approaches by 2015. The latest edition of bfinance's Pension Fund Asset Allocation Survey, from which this figure is taken, reveals that market volatility was the biggest source of long-term investors' fears at the beginning of 2012. To control this risk, international institutional investors are reviewing their portfolio diversification targets t in the direction of alternative classes, particularly real estate and infrastructure. At the same time, an increasing number of them (37%) are considering migrating a portion of their traditional passive investments towards thematic index approaches.

Towers Watson’s institutional investment clients have allocated over £10bn to Smart Beta solutions in the past five years. During this time, the company has partnered with many different asset managers to develop 20 Smart Beta solutions in areas where there were good investment ideas but no desirable investment products, on a net of fees basis.

Craig Baker, global head of investment research at Towers Watson, said: “We are entirely focused on providing our clients the best net-of-fees investment propositions, regardless of whether they are large or small or investing actively or passively. Smart Beta solutions have particularly wide applications for most of our clients which is why we have worked with many different top asset managers to develop these new solutions. Having the ideas and the relationships in the industry, means we have been able to design much better net-of-fees products for our clients.”

|