In response to the imperfections of investment approaches based on market capitalisation indices, the fund industry has come up with many solutions based on more efficient indices over the last few years. Several strategies have been developed, all sharing the objective of reducing the level of portfolio risk to achieve the best possible control over performance.

Low volatility/minimum variance, risk weighted approaches, equal weighted portfolios, fundamental indexation and so on. Whether they follow an efficient index (MSCI Equal Weighted, FTSE RAFI, FTSE 100 Minimum Variance, S&P 500 Risk Control Indices) or seek to achieve additional return by playing on market anomalies (small/mid indices), so-called "beta efficient" strategies are already used in Europe by most Dutch, Belgian and German pension funds.

This trend is expected to spread. One third of international institutional investors expect to devote over 10% of their portfolio to efficient index investment approaches by 2015.

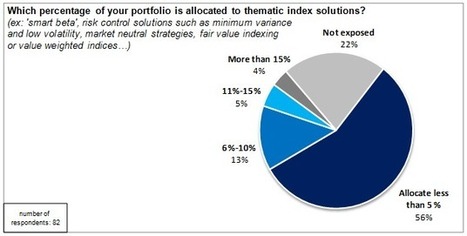

The latest edition of bfinance's Pension Fund Asset Allocation Survey, from which this figure is taken, reveals that market volatility was the biggest source of long-term investors' fears at the beginning of 2012. To control this risk, international institutional investors are reviewing their portfolio diversification targets t in the direction of alternative classes, particularly real estate and infrastructure. At the same time, an increasing number of them (37%) are considering migrating a portion of their traditional passive investments towards thematic index approaches.

Standard asset allocation problems such as mean variance or conditional value at risk can be easily developed and solved using MATLAB® and Financial ...

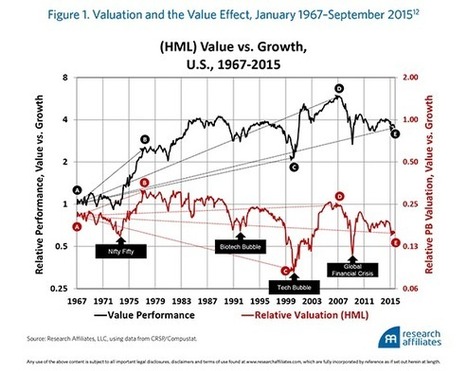

If investors don’t wise up soon that rising valuations are responsible for most of the “alpha” produced by smart beta, the inevitable mean reversion to historical valuation norms threatens to unleash a smart beta crash.

By Bradley Krom While smart beta has become prevalent for equity strategies, its application to fixed income is still more or less in its infancy. Over the next

“Deconstructing 'Smart Beta'ETF.comThe inquiries are coming in faster and harder than ever before. Everyone wants facts and figures about so-called smart-beta funds: How many are there? What's the biggest one?”

“Nest moves to smart beta investment approachCitywire.co.ukAs a result, Nest said it had built on its belief in passive investing to invest more into alternative indexing, or smart beta, to get the best returns at a low cost.”

“ETF TrendsAre Smart Beta ETFs Smart Investments?ForbesThe concept of smart beta funds has intrigued me. Smart beta funds use quantitative rankings to determine what stocks to hold and how to weight them.”

Investment Week Recent market commentary has raised concerns around crowded trades that could adversely affect smart beta strategies, writes Gaurav Mallik, global head of equity strategies at State Street Global Advisors.

Scientific Beta, the smart beta index provider that has come out of academic work done by Edhec Risk Institute, has launched an flexible fee structure.

Find our latest news and press releases here. BlackRock’s iShares business, the world’s largest manager of exchange traded funds (ETFs), projects that smart beta ETF assets will reach $1 trillion globally by 2020 and $2.4 trillion by 2025.

“Investors can target quality international stocks through a new suite of so-called Quality Mix exchange traded funds that mirror strategies employed by Warren (Smart-Beta International ETFs With a Buffett-esque Approach: Investors can target...”

To get content containing either thought or leadership enter:

To get content containing both thought and leadership enter:

To get content containing the expression thought leadership enter:

You can enter several keywords and you can refine them whenever you want. Our suggestion engine uses more signals but entering a few keywords here will rapidly give you great content to curate.

Your new post is loading...

Your new post is loading...