Your new post is loading...

Your new post is loading...

|

Scooped by

Beeyond

June 23, 9:44 AM

|

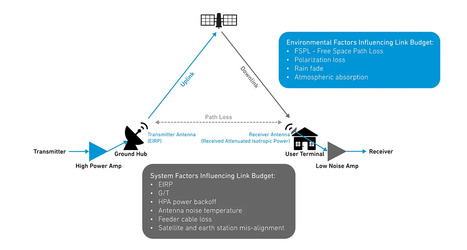

When a consumer installs a satellite dish on a roof, they establish a pristine, uncompromised line of sight to the sky using an active phased-array antenna with massive gain (30+ dBi). That architecture scales. Direct-to-Device does not. When you remove the dedicated roof dish and attempt to close that same 500 km link with an unmodified smartphone, you are forced to rely on an isotropic, omnidirectional antenna yielding roughly 0 dBi of gain and operating at a fraction of a watt of transmit power.

Despite the massive satellite apertures currently being deployed to brute-force the uplink, the laws of physics remain unforgiving. Orbital D2D cannot provide meaningful concurrent sector capacity, cannot provide low latency, and, due to a microscopic penetration margin, absolutely cannot provide indoor coverage.

Orbital D2D is more like an insurance policy. It is a brilliant, necessary solution for the 0.0001% of edge cases like the stranded hiker, the mid-ocean SOS, and extreme remote telemetry. But for Telcos tasked with delivering gigabits of data to dense urban and suburban populations, where 80% of data is consumed indoors, orbital D2D is practically useless as a core capacity layer.

|

|

Scooped by

Beeyond

June 21, 5:53 PM

|

At Reliance's Annual General Meeting, Jio shared a detailed proposal with India’s space regulator, IN-SPACe, outlining a massive orbital infrastructure project. The plan details the deployment of a proprietary Low Earth Orbit satellite constellation comprising approximately 1,650 satellites. Positioned at an operational altitude of approximately 650 kilometers, the network is designed to target two distinct service models: high-throughput rural fixed broadband and Direct-to-Device connectivity, which allows standard, off-the-shelf smartphones to connect directly to satellites without specialized satellite dishes or hardware modifications.

|

|

Scooped by

Beeyond

June 18, 8:41 AM

|

In 1932, American industrialist Eben Byers died after his jaw physically collapsed from drinking “Radithor”, an over-the-counter energy drink infused with raw radium. In the early 20th century, society was so mesmerized by the superficial “glow” of radiation that brands blindly put thorium and radium into cosmetics, toothpaste, and water. It wasn’t until 1938, when the lethal, cellular-level destruction of radiation became undeniable, that governments stepped in, stripped radioactive elements from consumer shelves, and locked nuclear energy behind strict regulatory walls.

Today, we are repeating that exact historical error.

|

|

Scooped by

Beeyond

June 14, 7:09 AM

|

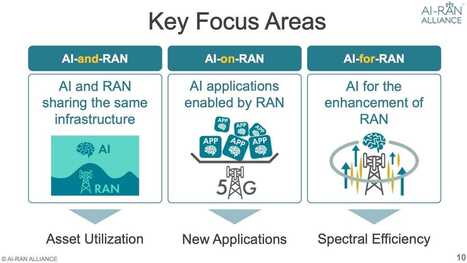

AI-RAN (artificial intelligence—radio access network) is a technology that enables the full integration of AI into the radio access network to realize transformative gains in operational performance, deliver new AI-based services, and unlock monetization opportunities. It enhances connectivity across mobile networks by leveraging AI to improve spectral efficiency, dynamic traffic handling, and real-time responsiveness.

|

|

Scooped by

Beeyond

June 8, 9:37 AM

|

Over the last eight months, NVIDIA has been aggressively pushing its AI-RAN strategy into the telecom ecosystem. We saw the high-profile operator announcements with T-Mobile, the deep Layer 1 baseband partnership with Nokia, and their massive strategic investment in custom silicon designer Marvell.

But all of that momentum had a strict physical boundary where NVIDIA stayed inside the baseband cabinet at the bottom of the tower. Their servers were targeting the Centralized Unit and the Distributed Unit part of Radio systems. The actual Radio Unit, the box clamped to the antenna at the top of the mast, was considered completely off-limits for general-purpose compute or dedicated chipsets.

The reason? The RU handles highly deterministic, real-time Layer 1 tasks in a harsh, passively cooled environment. The industry assumption was that a power-hungry GPU could never survive the strict energy, cost, and thermal constraints of the antenna. That space belonged exclusively to the highly efficient, custom ASICs built by Ericsson, Nokia, and Huawei.

|

|

Scooped by

Beeyond

May 30, 11:04 AM

|

The telecom world is split right down the middle over a major spending decision. This is even more polarizing than whether Pizza should have pineapple or if cats are better pets than dogs. The Telco fans are divided!

Telcos are trying to figure out whether tomorrow’s radio networks actually need GPUs, or if they can just keep using dedicated ASICs or even the CPU hardware they already have. The decision may seem small, but it has massive consequences across the value chain, vendors, the ecosystem, Capex, and monetization.

To understand where people stand, I ran a poll on LinkedIn asking if we actually need GPUs in the RAN to build a future-proof RAN network, or if the standard ASIC/CPU approach is enough. The results showed a clear dividing line. Around 60% said standard ASICs and CPUs are good enough, while 40% feels GPUs are mandatory.

|

|

Scooped by

Beeyond

May 28, 5:44 AM

|

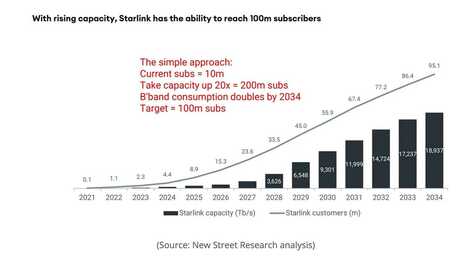

While the telecom sector spent years comfortably looking down on satellite internet as a niche utility for remote cabins, the cold mathematics of orbital infrastructure have been quietly laying the groundwork for an absolute takeover. A recent comprehensive forecast by the analyst firm New Street Research projected that Starlink will scale from its current base of roughly 10.3 million users to a massive 100 million subscribers by 2034. That means capturing nearly 10% of the global fixed broadband market and translating that density into roughly $49 billion to $55 billion in annual top-line revenue.

|

|

Scooped by

Beeyond

May 24, 5:53 AM

|

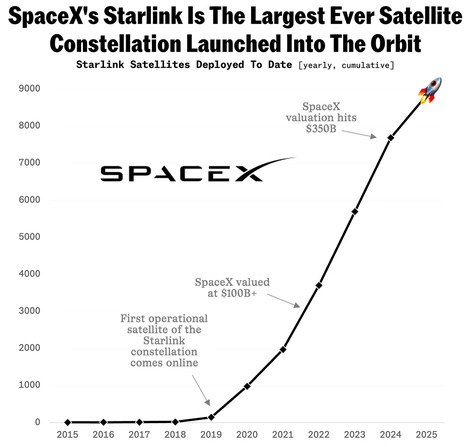

The SpaceX S-1 filing is their public declaration that the traditional telecommunications business model has entered a terminal phase. By valuing its connectivity segment opportunity against a $1.6 trillion Total Addressable Market, SpaceX is not signaling a partnership with telcos but their replacement, to the fullest extent that physics allows. This transition may not be completed in 12 or 24 months, but the 10-year ambition is clear.

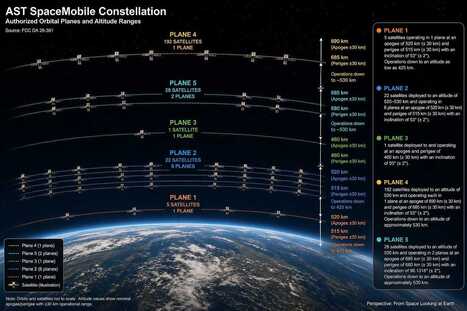

Faced with this orbital expansion, the industry is frantically seeking a counterweight, and market sentiment has converged on AST SpaceMobile as the only viable alternative. It is time to examine what AST SpaceMobile brings to the table in terms of its corporate strategy, technological architecture, and partnership framework, and to assess whether it offers telcos a path to maintaining their relevance.

|

|

Scooped by

Beeyond

May 22, 3:55 AM

|

The financial markets are currently parsing the implications of SpaceX’s proposed $1.75tn IPO valuation. While much of the initial retail focus has centered on the company’s interplanetary ambitions, institutional investors are scrutinizing a far more grounded thesis detailed in the May 2026 S-1 filing. The prospectus outlines a strategic pivot from a launch-and-logistics provider to a vertically integrated global telecommunications and compute utility.

At 94 times its projected 2025 consolidated revenue of $18.67bn, SpaceX’s valuation represents a significant departure from traditional aerospace and telecommunications multiples. The justification rests on the company’s definition of a staggering $28.5tn Total Addressable Market. By partitioning this TAM into space logistics ($370bn), global connectivity ($1.6tn), and AI infrastructure ($26.5tn), the prospectus argues that the historical separation between the physical transport of data and the compute layer is converging, and the company intends to capture the margins of both.

|

|

Scooped by

Beeyond

May 20, 9:18 AM

|

This week at the J.P. Morgan Global Technology, Media and Communications Conference, executive leadership from the major U.S. wireless carriers and AST SpaceMobile presented their outlooks on the direct-to-device satellite market. The public consensus among the telecom CEOs framed orbital connectivity as a strictly complementary technology rather than a disruptive threat.

Verizon CEO Dan Schulman stated that for the foreseeable future, satellite will remain a complementary service to the carriers. He noted that terrestrial capacity is 100 to 1,000 times more efficient than satellite in urban and suburban areas. T-Mobile CEO Srinivasan Gopalan doubled down on this view, noting that satellite traffic currently accounts for just 0.0002% of T-Mobile’s total network usage. Gopalan also dismissed the potential threat of a D2D provider launching an MVNO to compete directly with carriers, arguing that it would not add incremental total addressable market. AT&T CEO John Stankey similarly described satellite as a natural extension of the network, acknowledging it currently handles a small percentage of total network traffic.

|

|

Scooped by

Beeyond

May 18, 10:12 AM

|

As I have consistently discussed, the sudden explosion of thousands of autonomous, AI-powered voice applications has pushed Twilio’s orchestration platform into the center stage of the Inference Economy.

Honestly, it feels almost stupid that a historically high-latency, expensive, frequently untested, and spam-ridden legacy voice channel like Twilio VOIP is fundamentally beating the global telecom operators who have literally owned and operated this infrastructure for 150 years.

Unfortunately, this is just a damning reflection of how little the telecom establishment understands about AI economics. How many times can a single industry lose its core service to outsiders?"

|

|

Scooped by

Beeyond

May 17, 11:09 AM

|

The military is moving from communications as a support function to communications as an operating layer. In the older model, networks connected headquarters, bases, command rooms, ships, vehicles, and troops. In the new model, networks connect drones, sensors, logistics systems, cyber platforms, autonomous vehicles, cloud environments, AI models, identity systems, command software, and industrial supply chains. The network is no longer outside the mission; it is now inside the mission.

|

|

Scooped by

Beeyond

May 14, 9:37 AM

|

A Tier One telco threw me an “acid test” question today. The question was much sharper: “With around 10,000 satellites in orbit today, how many fixed broadband households can Starlink actually support? 20 million, 30 million, 100 million?” That question is important because it is not about coverage but about damage. Fixed and cable players do not lose sleep because Starlink can draw a coverage map over the planet; they lose sleep if Starlink can take paying broadband households at scale without destroying its own quality.

|

|

|

Scooped by

Beeyond

June 22, 9:50 AM

|

Telecom autonomy has struggled to evolve under traditional machine learning models because these older systems operate as uninterpretable black boxes. Machine learning excels at deterministic tasks and pattern recognition across massive datasets. However, network engineers managing critical infrastructure require clear explanations before executing system changes.

This lack of explainability stalled the progression of autonomous networks. Handing over control of complex actions without understanding the underlying math creates an extremely risky trust gap for Telcos. To resolve this, Nokia and Google Cloud designed the Gemini-powered agents using a “glass box” architecture.

Instead of executing an unverified command, the action reasoner agent functions as an advisory layer. It processes the network data and presents a confidence-based recommendation to the human operator. Because these specialized agents can explain their conclusions and reasoning, they elicit greater trust from users. Human engineers retain control and final approval over critical control points before logging and executing fixes. By combining autonomous data analysis with human observability, the platform establishes the required safety to deploy machine-speed operations.

|

|

Scooped by

Beeyond

June 19, 9:39 AM

|

Global mobile network data traffic grew by 22% between the first quarter of 2025 and the first quarter of 2026. That is a steady number, but it shows growth is slowing. Compare that to 2019, when the explosion of mobile video caused traffic to spike by 80% year-on-year. The data shows that the predicted AI data tsunami on the access network is absent.

|

|

Scooped by

Beeyond

June 18, 3:39 AM

|

By anchoring machine identities directly at the network or hardware level, operators can definitively authenticate automated assets and enforce strict security boundaries. Recent initiatives by operators like SK Telecom and StarHub demonstrate this emerging use case, moving beyond high-level AI experimentation to build concrete frameworks that assign verifiable identities to autonomous systems, enabling audit, monitoring, and secure machine-to-machine operations.

|

|

Scooped by

Beeyond

June 13, 9:10 AM

|

Sure, 6G will deliver necessary operational improvements. It will utilize new 7GHz spectrum, improve radio performance, and lower the cost per bit for operators still recovering from the 5G capex hangover. However, consumers and enterprises do not pay a premium for faster pipes. Connectivity is now a hyper-commoditized utility.

If Telcos want to capture value in this new economy, they must stop defining their core business as “connectivity.” Telecom is a distribution business.

Networks serve as the last-mile delivery system for the global economy. In the past, the industry distributed voice, SMS, and 8K video. Today, the asset being distributed is intelligence. Hyperscalers are building massive, centralized AI data centers, but that compute power requires a physical delivery mechanism to reach users.

To get in the path of the money, telecom operators must pivot to distributing AI agents and semantic compute to the edge.

|

|

Scooped by

Beeyond

June 1, 11:34 AM

|

Yes, Laser is the ultimate communications medium. Physics dictates that transmitting photons through a vacuum offers near-infinite bandwidth with zero latency constraints. But deploying naked lasers on Earth has historically been an exercise in frustration. Atmospheric turbulence, fog, rain, and physical interference forced the industry to wrap light in glass cables or default to the reliable, albeit slower, medium of radio frequencies.

For decades, Free Space Optics, or FSO, was dismissed as a fragile science experiment, and, to some extent, the case was officially closed.

Laser communications are back, driven by an explosion of technology developments and critical infrastructure needs that were once far from mainstream. Today, lasers are taking over every single layer of the network topology simultaneously, building a seamless architecture from space down to the terrestrial core. In orbit, optical inter-satellite links are creating massive mesh networks in a vacuum to route data globally.

|

|

Scooped by

Beeyond

May 29, 6:44 AM

|

Why is a company in its earliest revenue stages worth more than the giant that built the ground network?

Because the market believes space communications will be just as big as terrestrial ones. Investors are looking at future cash flows, betting that AST will carry a massive chunk of global mobile traffic, and do it with a SaaS-style model that completely bypasses the heavy, low-margin hardware trap telcos force on terrestrial vendors today.

|

|

Scooped by

Beeyond

May 27, 3:14 AM

|

There is a unicorn startup out of Latin America called NotCo. Their killer product is NotMilk. It is exactly what it sounds like: milk that tastes, pours, and froths exactly like milk. But it takes the cow completely out of the equation.

Yes! They removed the friction of the animal, the environmental tax, and the legacy supply chain, yet delivered the exact sensory outcome you want in your morning latte.

The telecom industry has the exact same problem.

After 150 years of legacy operations, the “telco” part of the equation produces nothing but friction. To be brutally honest, the word itself is tainted. It is universally associated with dropped calls, incomprehensible billing, utility, hidden fees, and hours wasted on hold.

But the reality is that today’s operators ( Telco) provide exponentially more value than basic connectivity alone. They are the invisible backbone of the modern digital economy. To survive, the industry needs to remove its own cow from the equation.

|

|

Scooped by

Beeyond

May 24, 5:51 AM

|

As a follow-up to our ongoing tracking of the telecommunication market, the structural contraction we’ve been mapping is visibly accelerating. The BT Group recently announced plans to eliminate up to 40% of its workforce by 2030, representing approximately 27,500 jobs. This follows a broader pattern across the global sector: Verizon recently executed a $2 billion restructuring program involving 15,000 corporate roles, while T-Mobile filed to reduce its corporate management layer in Bellevue, Washington. Across the entire ecosystem, operators and their supply chains are systematically reducing headcount.

The telecommunications labor market is locked into a structural contraction that will continue at least through this decade, and the reasons have nothing to do with AI or any technological shift.

|

|

Scooped by

Beeyond

May 21, 9:20 AM

|

To appreciate the significance of this development, it is helpful to look back at the previous defining era of telecommunications. In the early 2010s, as smartphones became ubiquitous and app economies exploded, the metric of value for both carriers and consumers shifted dramatically. This was the era of the gigabyte. Subscriptions, usage caps, and pricing tiers were all defined by data consumption. Telcos established the price per gigabyte as their primary billing KPI, monetizing the massive demand for mobile internet, video streaming, and app-based services. For a decade, the “GB per month” was the yardstick of digital life.

|

|

Scooped by

Beeyond

May 19, 10:19 AM

|

Look at the image above. On the left is your current human subscriber. For the last two decades, you have sold them GBs per month, fought over marginal ARPU increases, and watched every single app try to commoditize your network. That race to the bottom didn’t end up really well.

On the right is your brand-new customer.

Figure just ran a live drill in which a human intern competed against its Figure 03 humanoid, “Bob,” to see who could sort and categorize more packages. The result? The human lost the moment they had to step away to go to the bathroom. F.03 just kept working.

|

|

Scooped by

Beeyond

May 17, 11:17 AM

|

If I were a Tier-1 Telco executive today, I would be deeply concerned about the long-term revenue damage Starlink will inflict. And yes, it will inflict damage, because you don’t plan for tens of thousands of satellites in orbit just to rescue a few stranded hikers on Mount Everest. That is the truth, whether the industry admits it out loud or not.

But trying to block Musk, or believing he will passively accept his fate as a submissive 3GPP radio vendor, is an absolute delusion. Forming a defensive cartel to isolate SpaceX does two highly dangerous things for legacy carriers. First, it moves the attention from the Real Problem, which is Earthbound CapEx and Flat Revenue, and secondly, It Wakes a Dragon and Triggers Asymmetric Retaliation.

|

|

Scooped by

Beeyond

May 15, 10:11 AM

|

On May 14, 2026, the three largest U.S. carriers announced a joint venture to pool spectrum for a unified direct-to-device (D2D) satellite platform. While the public narrative centers on rural coverage, this is a defensive restructuring of telecom power.

Satellite connectivity is scaling aggressively. SpaceX’s V3 satellites and Starship launches will soon drive a 10x capacity increase, while recent regulatory shifts have elevated Starlink from a vendor to a sovereign spectrum holder. Concurrently, Amazon’s acquisition of Globalstar gives the hyperscaler direct access to Apple’s D2D consumer market. Far beyond eliminating dead zones, this JV marks a high-stakes power struggle between legacy Tier-1 operators and vertically integrated space titans for the control of next-generation communications.

|