Your new post is loading...

Your new post is loading...

|

Scooped by

Beeyond

Today, 8:40 AM

|

“There is a 1% population that’s not covered today in very rural areas,” Desroches stated. “And I think satellite is a great solution for that... but within urban and suburban areas, the infrastructure that is in place is better. It is the cost per bit to deliver that is cheaper.”. From the perspective of a tier-one telecom operator managing a $176 billion connectivity business that provides nationwide premium fiber and 5G service across America, this position makes total sense.

But the moment you set foot outside the telecom world, the broader financial market paints a radically different picture. Wall Street analysts are issuing downgrades over the satellite threat, and SpaceX is currently on its roadshow for a historic June 12 IPO targeting a $1.75 trillion valuation. It is a number built almost entirely on the premise of disrupting the global telecommunications market; in fact, SpaceX models Starlink’s total addressable market at $1.3 trillion, which is the exact size of total global telecom revenues.

|

|

Scooped by

Beeyond

June 6, 10:25 AM

|

The postman. I remember him from when I was a kid. He was an elderly man who brought letters to the door. We got excited when the doorbell rang because it meant news, a connection, or an update. Technology killed that job. Faster, cheaper ways to send messages replaced him. It wasn’t because the job was bad; it was because the economics of communication changed.

We’re seeing the exact same thing happen in telecom customer care right now. People like to say “AI will assist the human,” implying a nice, happy future where machines and people work together. That’s a lie. AI is not helping reps but replacing them. This is driven by three simple things: customers demand zero friction, speed matters more than small talk, and the cost of human labor is way too high.

The Telco call customer care layer is not evolving, but ending. Now, the human part doesn’t stop at zero. As the front lines go fully automated, a tiny group of about 5% of humans will remain. This is a high-stakes, specialized workforce. Their job is harder and more intense than anything we’ve seen before.

|

|

Scooped by

Beeyond

June 3, 7:02 AM

|

Techco is dead.The definition was always consulting fluff.

McKinsey defined Techco as an evolution into “platform-oriented innovators akin to today’s top tech players.” The financial mechanics prove this is a category error. Telcos and tech companies share nothing but the letter “T”. The inherent financial structure leaves no room for debate: telecom runs on 1% R&D; tech runs on 15% or more. We do not write proprietary operating systems or build global developer ecosystems. We manage heavy, long-lived physical infrastructure, power, and heating loads, using standardized vendor hardware.

Attempting to secure a software valuation by changing corporate vocabulary does not alter the depreciation cycle of a cell tower or the CapEx of a fiber trench. Techco is simply the newest headstone in the telecom graveyard, buried alongside WAP portals, Telco 2.0, DSP, and the Smartpipe.

|

|

Scooped by

Beeyond

May 30, 11:04 AM

|

The telecom world is split right down the middle over a major spending decision. This is even more polarizing than whether Pizza should have pineapple or if cats are better pets than dogs. The Telco fans are divided!

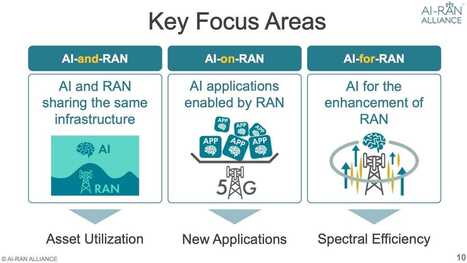

Telcos are trying to figure out whether tomorrow’s radio networks actually need GPUs, or if they can just keep using dedicated ASICs or even the CPU hardware they already have. The decision may seem small, but it has massive consequences across the value chain, vendors, the ecosystem, Capex, and monetization.

To understand where people stand, I ran a poll on LinkedIn asking if we actually need GPUs in the RAN to build a future-proof RAN network, or if the standard ASIC/CPU approach is enough. The results showed a clear dividing line. Around 60% said standard ASICs and CPUs are good enough, while 40% feels GPUs are mandatory.

|

|

Scooped by

Beeyond

May 27, 3:14 AM

|

There is a unicorn startup out of Latin America called NotCo. Their killer product is NotMilk. It is exactly what it sounds like: milk that tastes, pours, and froths exactly like milk. But it takes the cow completely out of the equation.

Yes! They removed the friction of the animal, the environmental tax, and the legacy supply chain, yet delivered the exact sensory outcome you want in your morning latte.

The telecom industry has the exact same problem.

After 150 years of legacy operations, the “telco” part of the equation produces nothing but friction. To be brutally honest, the word itself is tainted. It is universally associated with dropped calls, incomprehensible billing, utility, hidden fees, and hours wasted on hold.

But the reality is that today’s operators ( Telco) provide exponentially more value than basic connectivity alone. They are the invisible backbone of the modern digital economy. To survive, the industry needs to remove its own cow from the equation.

|

|

Scooped by

Beeyond

May 26, 7:26 AM

|

Look at the machine the telecom industry built.

It is, without exaggeration, the most complex and astonishing technological achievement in human history. Right now, it seamlessly connects 6 billion human beings and 21 billion machines. It works everywhere, anytime, and almost for free.

Engineers designed this infrastructure to operate with 99.999% reliability. Every five years, they completely rebuild it from the ground up just to make it run 10x faster. It keeps the global digital economy breathing across continents, oceans, and concrete.

It is an absolute miracle of physics.

And the reward?

Nobody loves the telco. In fact, the public barely tolerates them. When you look at the cold, hard data, the telecom sector sits at the absolute bottom of global brand loyalty. It ranks below airlines and banks, and is functionally tied to the local tax authority in the hearts of its own consumers.

|

|

Scooped by

Beeyond

May 22, 3:55 AM

|

The financial markets are currently parsing the implications of SpaceX’s proposed $1.75tn IPO valuation. While much of the initial retail focus has centered on the company’s interplanetary ambitions, institutional investors are scrutinizing a far more grounded thesis detailed in the May 2026 S-1 filing. The prospectus outlines a strategic pivot from a launch-and-logistics provider to a vertically integrated global telecommunications and compute utility.

At 94 times its projected 2025 consolidated revenue of $18.67bn, SpaceX’s valuation represents a significant departure from traditional aerospace and telecommunications multiples. The justification rests on the company’s definition of a staggering $28.5tn Total Addressable Market. By partitioning this TAM into space logistics ($370bn), global connectivity ($1.6tn), and AI infrastructure ($26.5tn), the prospectus argues that the historical separation between the physical transport of data and the compute layer is converging, and the company intends to capture the margins of both.

|

|

Scooped by

Beeyond

May 20, 9:18 AM

|

This week at the J.P. Morgan Global Technology, Media and Communications Conference, executive leadership from the major U.S. wireless carriers and AST SpaceMobile presented their outlooks on the direct-to-device satellite market. The public consensus among the telecom CEOs framed orbital connectivity as a strictly complementary technology rather than a disruptive threat.

Verizon CEO Dan Schulman stated that for the foreseeable future, satellite will remain a complementary service to the carriers. He noted that terrestrial capacity is 100 to 1,000 times more efficient than satellite in urban and suburban areas. T-Mobile CEO Srinivasan Gopalan doubled down on this view, noting that satellite traffic currently accounts for just 0.0002% of T-Mobile’s total network usage. Gopalan also dismissed the potential threat of a D2D provider launching an MVNO to compete directly with carriers, arguing that it would not add incremental total addressable market. AT&T CEO John Stankey similarly described satellite as a natural extension of the network, acknowledging it currently handles a small percentage of total network traffic.

|

|

Scooped by

Beeyond

May 18, 10:15 AM

|

All ESP32 (and some ESP8266) devices can make use of at least one type of mesh network to communicate, peer-to-peer, without the need for a centralized “router.” Others can be used to interface with existing smart homes, communicate over long distances, or take advantage of low-latency data transfer in useful projects that are fun to make.

|

|

Scooped by

Beeyond

May 17, 11:17 AM

|

If I were a Tier-1 Telco executive today, I would be deeply concerned about the long-term revenue damage Starlink will inflict. And yes, it will inflict damage, because you don’t plan for tens of thousands of satellites in orbit just to rescue a few stranded hikers on Mount Everest. That is the truth, whether the industry admits it out loud or not.

But trying to block Musk, or believing he will passively accept his fate as a submissive 3GPP radio vendor, is an absolute delusion. Forming a defensive cartel to isolate SpaceX does two highly dangerous things for legacy carriers. First, it moves the attention from the Real Problem, which is Earthbound CapEx and Flat Revenue, and secondly, It Wakes a Dragon and Triggers Asymmetric Retaliation.

|

|

Scooped by

Beeyond

May 15, 10:11 AM

|

On May 14, 2026, the three largest U.S. carriers announced a joint venture to pool spectrum for a unified direct-to-device (D2D) satellite platform. While the public narrative centers on rural coverage, this is a defensive restructuring of telecom power.

Satellite connectivity is scaling aggressively. SpaceX’s V3 satellites and Starship launches will soon drive a 10x capacity increase, while recent regulatory shifts have elevated Starlink from a vendor to a sovereign spectrum holder. Concurrently, Amazon’s acquisition of Globalstar gives the hyperscaler direct access to Apple’s D2D consumer market. Far beyond eliminating dead zones, this JV marks a high-stakes power struggle between legacy Tier-1 operators and vertically integrated space titans for the control of next-generation communications.

|

|

Scooped by

Beeyond

May 14, 9:37 AM

|

A Tier One telco threw me an “acid test” question today. The question was much sharper: “With around 10,000 satellites in orbit today, how many fixed broadband households can Starlink actually support? 20 million, 30 million, 100 million?” That question is important because it is not about coverage but about damage. Fixed and cable players do not lose sleep because Starlink can draw a coverage map over the planet; they lose sleep if Starlink can take paying broadband households at scale without destroying its own quality.

|

|

Scooped by

Beeyond

May 10, 5:34 AM

|

For over a decade, the telecommunications industry has been running away from its own identity. We were told that being a “pipe” was a death sentence, leading many Telcos to pursue other ventures rather than remain Telcos, while neglecting the engineering masterpiece beneath their feet. But as Kim Krogh Andersen (Product and technology from Telstra) recently highlighted at TM Forum, the tides are shifting. His message was a refreshing wake-up call for the industry: The network is not a commodity to be hidden; it is the product itself.

Switching our mindset from “providing access” to “selling a programmable product” is the most significant architectural and cultural pivot of this generation. It’s an admission that our 99.999 % reliability is not just a utility but a high-performance engine that, if properly exposed, can power the next era of the Inference Economy. Based on Andersen’s insights and the emerging shift toward AI-native architectures, I have identified 10 concrete aspects that define what it truly means to treat your network as a product.

|

|

|

Scooped by

Beeyond

June 8, 5:21 AM

|

Unplanned downtime costs manufacturers $50B annually. Root causes, prevention strategies, and CMMS-powered approaches to eliminate reactive maintenance.

|

|

Scooped by

Beeyond

June 5, 9:21 AM

|

When I worked at Google, the cultural difference was clear. Engineers there were treated like stars. This wasn’t just a figure of speech; they earned the same respect and pay as top athletes like Messi or Michael Jordan. They got million-dollar contracts because leadership knew that nothing would happen without their talent. The business team at Google understood their job was to support the engineers’ work. They knew the product was the engineering, and they treated the engineers with real respect.

Contrast that with the average telecom operator or vendor today. If you walk into a typical telco office, you will find the engineers in the backseat, hidden away in back rooms, tasked with the mundane, high-pressure duty of keeping the network alive. They are the ones sweating over the five-nines, ensuring the infrastructure stays up through every crisis, while the people at the front of the room- the business folks, the strategic advisors, the ones who talk big and sell the “digital transformation” vision- take the glory. It is a massive absurdity.

|

|

Scooped by

Beeyond

June 1, 11:34 AM

|

Yes, Laser is the ultimate communications medium. Physics dictates that transmitting photons through a vacuum offers near-infinite bandwidth with zero latency constraints. But deploying naked lasers on Earth has historically been an exercise in frustration. Atmospheric turbulence, fog, rain, and physical interference forced the industry to wrap light in glass cables or default to the reliable, albeit slower, medium of radio frequencies.

For decades, Free Space Optics, or FSO, was dismissed as a fragile science experiment, and, to some extent, the case was officially closed.

Laser communications are back, driven by an explosion of technology developments and critical infrastructure needs that were once far from mainstream. Today, lasers are taking over every single layer of the network topology simultaneously, building a seamless architecture from space down to the terrestrial core. In orbit, optical inter-satellite links are creating massive mesh networks in a vacuum to route data globally.

|

|

Scooped by

Beeyond

May 28, 5:44 AM

|

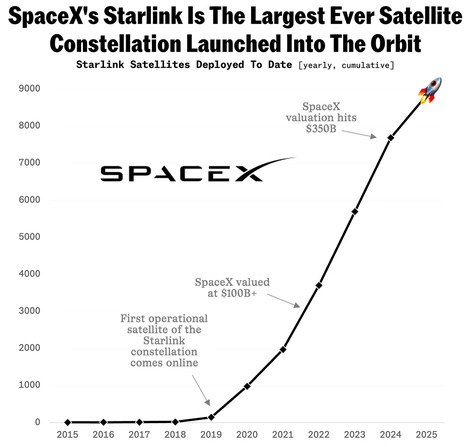

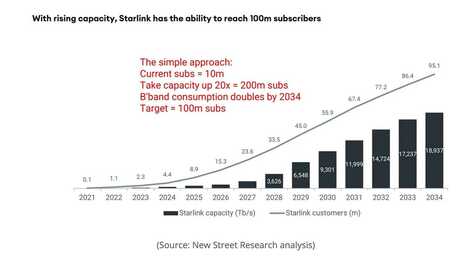

While the telecom sector spent years comfortably looking down on satellite internet as a niche utility for remote cabins, the cold mathematics of orbital infrastructure have been quietly laying the groundwork for an absolute takeover. A recent comprehensive forecast by the analyst firm New Street Research projected that Starlink will scale from its current base of roughly 10.3 million users to a massive 100 million subscribers by 2034. That means capturing nearly 10% of the global fixed broadband market and translating that density into roughly $49 billion to $55 billion in annual top-line revenue.

|

|

Scooped by

Beeyond

May 26, 10:05 AM

|

Today, video streaming consumes around 70% of network traffic. Naturally, we spent years building infrastructure optimized for humans watching screens, chasing peak download speeds, and fighting buffering.

That architecture is about to change dramatically.

The 2026 Cisco report reveals a rapid structural shift in how networks are used. AI inference token consumption is growing 10x year over year, and by 2035, inference alone will account for 25% of total network traffic. But this time, the real issue is not volume but the shape of the data.

Agentic AI operates autonomously at software speed. An agent executing a task generates up to 450% more traffic than a human would. More importantly, it requires sustained state and upstream capacity, not downstream bursts. Autonomous agents don’t care about gigabit downlink speeds. Their survival relies entirely on Time To First Token (TTFT) and an unbroken connection to the model.

If you are still engineering exclusively for downstream consumer video, you are building for the past. Here is the technical reality of the new inference network.

|

|

Scooped by

Beeyond

May 24, 5:53 AM

|

The SpaceX S-1 filing is their public declaration that the traditional telecommunications business model has entered a terminal phase. By valuing its connectivity segment opportunity against a $1.6 trillion Total Addressable Market, SpaceX is not signaling a partnership with telcos but their replacement, to the fullest extent that physics allows. This transition may not be completed in 12 or 24 months, but the 10-year ambition is clear.

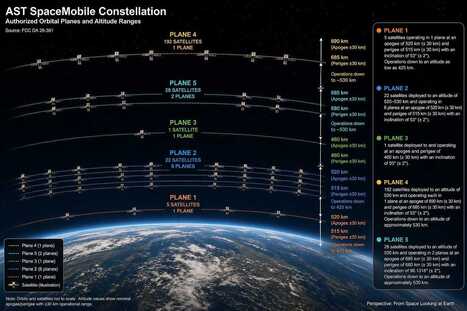

Faced with this orbital expansion, the industry is frantically seeking a counterweight, and market sentiment has converged on AST SpaceMobile as the only viable alternative. It is time to examine what AST SpaceMobile brings to the table in terms of its corporate strategy, technological architecture, and partnership framework, and to assess whether it offers telcos a path to maintaining their relevance.

|

|

Scooped by

Beeyond

May 21, 9:20 AM

|

To appreciate the significance of this development, it is helpful to look back at the previous defining era of telecommunications. In the early 2010s, as smartphones became ubiquitous and app economies exploded, the metric of value for both carriers and consumers shifted dramatically. This was the era of the gigabyte. Subscriptions, usage caps, and pricing tiers were all defined by data consumption. Telcos established the price per gigabyte as their primary billing KPI, monetizing the massive demand for mobile internet, video streaming, and app-based services. For a decade, the “GB per month” was the yardstick of digital life.

|

|

Scooped by

Beeyond

May 19, 10:19 AM

|

Look at the image above. On the left is your current human subscriber. For the last two decades, you have sold them GBs per month, fought over marginal ARPU increases, and watched every single app try to commoditize your network. That race to the bottom didn’t end up really well.

On the right is your brand-new customer.

Figure just ran a live drill in which a human intern competed against its Figure 03 humanoid, “Bob,” to see who could sort and categorize more packages. The result? The human lost the moment they had to step away to go to the bathroom. F.03 just kept working.

|

|

Scooped by

Beeyond

May 18, 10:12 AM

|

As I have consistently discussed, the sudden explosion of thousands of autonomous, AI-powered voice applications has pushed Twilio’s orchestration platform into the center stage of the Inference Economy.

Honestly, it feels almost stupid that a historically high-latency, expensive, frequently untested, and spam-ridden legacy voice channel like Twilio VOIP is fundamentally beating the global telecom operators who have literally owned and operated this infrastructure for 150 years.

Unfortunately, this is just a damning reflection of how little the telecom establishment understands about AI economics. How many times can a single industry lose its core service to outsiders?"

|

|

Scooped by

Beeyond

May 17, 11:09 AM

|

The military is moving from communications as a support function to communications as an operating layer. In the older model, networks connected headquarters, bases, command rooms, ships, vehicles, and troops. In the new model, networks connect drones, sensors, logistics systems, cyber platforms, autonomous vehicles, cloud environments, AI models, identity systems, command software, and industrial supply chains. The network is no longer outside the mission; it is now inside the mission.

|

|

Scooped by

Beeyond

May 15, 5:03 AM

|

La 125e édition du concours Lépine vient de s'achever, récompensant des inventions toujours plus ingénieuses. Nous avons réalisé une sélection des plus originales d'entre elles. Que diriez-vous de vendre (on peut aussi le donner) votre accès Internet inutilisé ? Le système DotDot permet de partager ses Gigas à travers un petit boîtier coloré intelligent qui crée « un réseau WiFi dans les 100 m autour de soi ». « C’est un partage de connexion anonyme sous stéroïdes », résumait Christophe Bureau, le fondateur, auprès d’actu Grenoble en mai 2025, après avoir remporté une médaille d’or.

|

|

Scooped by

Beeyond

May 11, 2:12 PM

|

For a decade, “Becoming a Utility” was the ultimate slur in the telecom boardroom. If you wanted to offend a Telco C-suite, you just needed to say: “You are nothing more than a Utility”.

But in 2026, the irony is really sad as Telcos should be begging for that utility status. While global operators grind out a stagnant 4% revenue growth, power utilities have positioned themselves as the AI revolution’s feedstock, surging at 8% their revenues in 2025 or double the pace of the so-called “TechCos.”

The industry remains stuck in an echo chamber of Haters dismissing leadership as incompetent, Vendors selling silver-bullet products to fix structural rot, and Denialists claiming tech agility on 2% revenue growth. To find the exit, we must stop the noise and address the five-dimensional trap: Regulatory, Technological, Market, Consumer, and Cultural, that keeps 300 intelligent Telco´s management teams producing identical mediocre results.

|