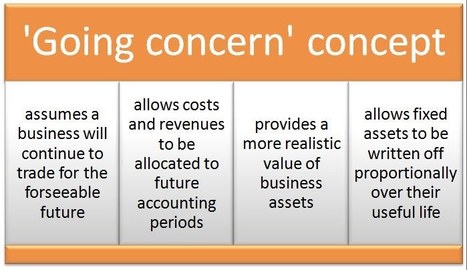

The 'going concern' concept in accounting is an assumption that the business will continue to exist for the foreseeable future. Accountants adopt the 'going concern' concept so they can prepare realistic financial reports. Without the 'going concern' concept, accountants would have to write off all assets in the current period including long term assets that still have an economic benefit for future periods.

Your new post is loading...

Your new post is loading...