JPMorgan's Chief Investment Office was given an edict to try to reduce risk-weighted assets, as part of a firm-wide initiative in the face of regulatory changes...

|

Scooped by

Ellie Kesselman Wells

onto Anomalies March 2, 2013 7:03 PM

|

JPMorgan's Chief Investment Office was given an edict to try to reduce risk-weighted assets, as part of a firm-wide initiative in the face of regulatory changes...

Your new post is loading...

Your new post is loading... Your new post is loading...

Your new post is loading...

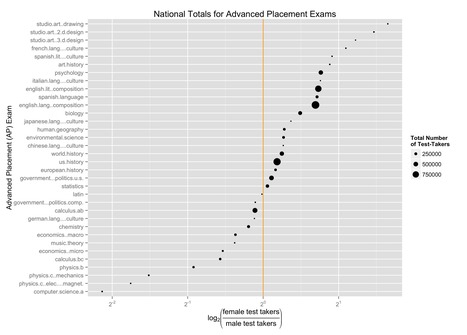

Barbara Ericson does an annual analysis of AP CS exam results. Her 2013 analysis attracted significant media attention.

Ellie Kesselman Wells's insight:

Some articles did a poor job with the statistics, so Kevin Karplus did a model-based analysis of Barbara's data. He was able to identify in which states the under-representation was truly significant. Best press coverage: NYTimes Bits blog, going beyond just the shocks in the 2013 results, e.g. the situation in computer science has worsened over time. In Wyoming, for instance, no high school student of ANY race or gender took the test, while 35 students took the test there in 2001.

Worst press coverage: Huffington Post used Barbara's results as an indication of how unimportant Computer Science is! "True, she was trying to point out there were too few computer science-focused girls compared to bio and math, but seriously, if that's our biggest problem..."

JPMorgan's Chief Investment Office was given an edict to try to reduce risk-weighted assets, as part of a firm-wide initiative in the face of regulatory changes...

Ellie Kesselman Wells's insight:

The default of Kodak in January 2012 was a credit event that would certainly have influenced JP Morgan's CIO's decisions leading up to the "London Whale" in May 2012. Eastman Kodak was part of many credit default swap indices. Kodak's filing for bankruptcy on January 19th led to a variety of idiosyncratic risk exposures in JPM's synthetic credit portfolio.

How fast is high-frequency stock trading? In the time it takes to read this sentence, tens of thousands of high-speed, computer-automated transactions can occur. Winning traders edge out rivals by intervals measured in nanoseconds. Fans of the practice say that high-frequency traders add crucial liquidity to the stock market. Critics dispute that claim and highlight, instead, lurking perils for the global financial system. Via Complexity Digest

Ellie Kesselman Wells's insight:

Yes! It IS time for some greater introspection about this, before there are even worse problems. Right now, there is very little understanding of risks to most people, including the voting public. European regulators seem to have a more realistic view and be willing to act upon it than in the U.S.A.

Ill-gotten gains are artificially bounded by zero, as there is no data on losses experienced by cybercriminals. Thus the shape and skew (mean and stdev too!) of frequency distributions are incorrect. Also: "Cybercrime surveys... exhibit a pattern of enormous, unverified outliers dominating the data... 90% of the estimate [was] from the answers of 1 or 2 individuals." The significant harm experienced by users rather than the small gain achieved by hackers is the true measure of the cost of cybercrime.

|

Much fanfare accompanied the Sept. 25, 2010, launch of the Air Force’s Space Based Space Surveillance satellite.

Ellie Kesselman Wells's insight:

It immediately went offline (though fixed, finally, in August 2012). The malfunction was due to a high-energy, ionizing radiation cloud, identified in 1958 by James Van Allen, when Sputnik I's instruments were also affected. He believed the cause to be anomalous radiation, which led to his discovery of the Van Allen radiation belts. The innermost belt dips closest to Earth above an area 300 km east of Brazil, at 200 km altitude, because the Earth's magnetic field is weakest there. On 8 Mar 2012, the Earth's upper atmosphere experienced the disruptive effects of solar flares. 2013 is the apex of that 11-year solar cycle, Once it has past, we'll only have the more predictable though not well-understood effects of the South Atlantic Anomaly to contend with.

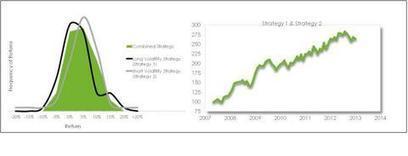

Most hedge funds claim to produce positive absolute returns. The reality is sobering: most strategies still largely depend on stock market performance and those not incorporating equities haven't kept their promises either.

Ellie Kesselman Wells's insight:

Natural motivation for a brief discussion of skew and kurtosis

How social media responses differ to expected and unexpected events (earthquakes).

Ellie Kesselman Wells's insight:

Compare social media responses to earthquakes, Hurricane Irene and the Yahoo! Music Awards; differences are obvious, and make sense intuitively.

|

The default of Kodak in January 2012 was a credit event that would certainly have influenced JP Morgan's CIO's decisions leading up to the "London Whale" in May 2012. Eastman Kodak was part of many credit default swap indices. Kodak's filing for bankruptcy on January 19th led to a variety of idiosyncratic risk exposures in JPM's synthetic credit portfolio.