(This article was first published on CYBAEA Data and Analysis, and kindly contributed to R-bloggers) Amazon UK | US We continue working our way through the examples, case studies, and exercises of what is affectionately known here as “the...

Your new post is loading...

Your new post is loading... Your new post is loading...

Your new post is loading...

(This article was first published on CYBAEA Data and Analysis, and kindly contributed to R-bloggers) Amazon UK | US We continue working our way through the examples, case studies, and exercises of what is affectionately known here as “the...

No comment yet.

Sign up to comment

One of the persistent themes on Wall Street is that investing strategies go in and out of favor on a regular basis. Oftentimes this has to do with the performance of the strategies, sometimes based on the structure of markets and always having to...

(This article was first published on Eran Raviv » R, and kindly contributed to R-bloggers)

Spurious Regression problem dates back to Yule (1926): “Why Do We Sometimes Get Nonsense Correlations between Time-series?

We posted yesterday that the S&P500 was set up for a pullback after carving out an outside day (higher high and lower low than previous day) at strong resistance and looked for follow through selling today. Didn’t happen.

(This article was first published on Systematic Investor » R, and kindly contributed to R-bloggers)

In the last post, Multiple Factor Model – Building Risk Model, I have shown how to build a multiple factor risk model.

December 2011 Case-Shiller Home Price Indices showed that 2011 ended at new index lows.

The National Composite Index fell by 3.8% during Q4; year over year changes were down 4.0%.

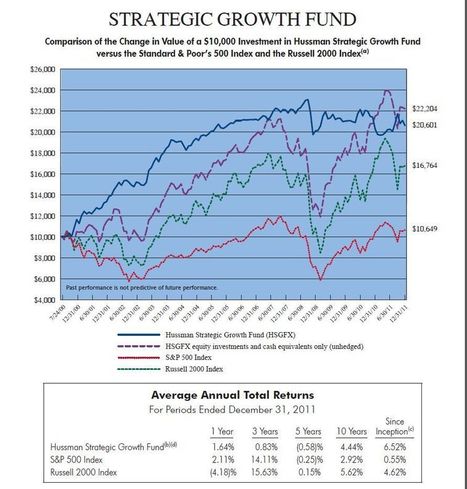

This is a really interesting semi-annual report from Hussman. In it he shows the returns of his main fund, both hedged and unhedged.

Are frontier markets the next emerging markets? And if so, should global equity investors include them in their portfolios? From a risk parity perspective, investors could benefit from a frontier markets allocation well in excess of the market weight of the asset class. A risk parity portfolio tends to outperform a market cap-weighted portfolio during periods of positive equity returns while delivering comparable returns during crisis periods. Even if portfolio managers could not follow a risk parity asset allocation strategy due to benchmark tracking considerations, overweighting frontier markets could help them outperform their benchmarks during upside periods without increasing downside risks significantly.

The Norwegian Government Pension Fund Global was recently ranked the largest fund on the planet. It is also highly rated for its professional, low-cost, transparent, and socially responsible approach to asset management. Investment professionals increasingly refer to Norway as a model for managing financial assets. We present and evaluate the strategies followed by the Fund, review long-term performance, and describe how it responded to the financial crisis. We conclude with some lessons that investors can draw from Norway’s approach to asset management, contrasting the Norway Model with the Yale Model.

(This article was first published on Systematic Investor » R, and kindly contributed to R-bloggers)

This is the third post in the series about Multiple Factor Models.

This is the second post in the series about Multiple Factor Models.

(This article was first published on R, Ruby, and Finance, and kindly contributed to R-bloggers) LaTeX is a typesetting system that can easily be used to create reports and scientific articles, and has excellent formatting options for...

(This article was first published on Systematic Investor » R, and kindly contributed to R-bloggers)

The Multiple Factor Model can be used to decompose returns and calculate risk.

|

In this post I want to summarize all the material I covered in the Multiple Factor Models series. The Multiple Factor Model can be used to decompose returns and calculate risk.

GNU R (ou simplement R) est un langage puissant de programmation utilisé pour le traitement de données et l’analyse statistique. R est un logiciel libre distribué selon les termes de la licence GNU GPL.

With this post I want to share some very interesting research insight from the world of correlation. Correlation metrics get a lot of attention during severe bear markets.

(This article was first published on Portfolio Probe » R language, and kindly contributed to R-bloggers)

2011 was a good vintage for minimum variance, at least among stocks in the S&P 500.

(This article was first published on Portfolio Probe » R language, and kindly contributed to R-bloggers)

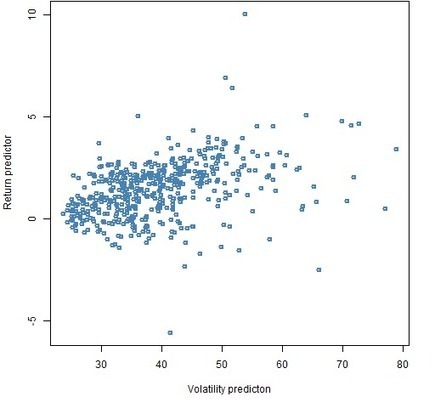

A look at the distortion from predicted to realized.

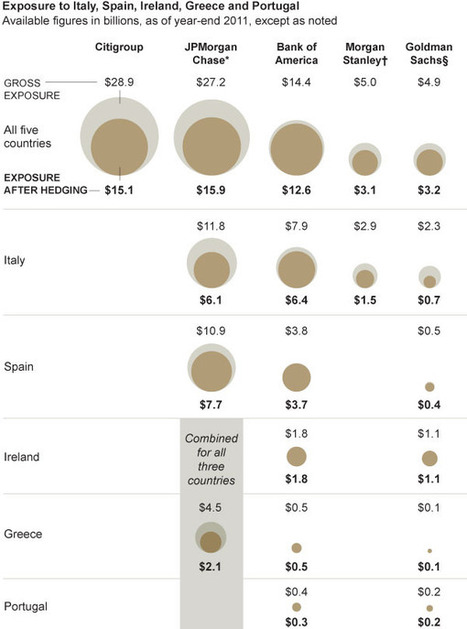

A Primer on the Euro Breakup

John Mauldin February 27, 2012 ~~~ It’s one thing to say that peripheral eurozone countries are better off leaving the euro, but how, exactly?

(This article was first published on Cartesian Faith » R, and kindly contributed to R-bloggers)

This is the second part in a three part series on teaching R to MFE students at CUNY Baruch.

This study investigates a number of anomaly variables in capital markets research around the world, including asset growth, book-to-market, investment-to-assets, momentum, net stock issues, size, and total accruals. We use zero-cost trading strategies, the Fama-French factor model, and the newly developed alternative investment-based three-factor model (Chen, Novy-Marx, and Zhang 2010) to show that these anomalies produce significant abnormal returns across countries. We show that abnormal returns vary dramatically among countries and between developed and emerging economies. We provide strong evidence to support the limits of arbitrage theory in international equity markets by documenting a positive correlation between idiosyncratic risk and abnormal returns for all of the anomalies. We also show that idiosyncratic risk has less impact on abnormal return for developed countries than emerging countries. Our results support the mispricing explanation of the existence of various anomalies around the world.

(This article was first published on Adventures in Statistical Computing, and kindly contributed to R-bloggers)

I have been looking into time series analysis with R. I'm still ramping up the learning curve as I am very accustomed to SAS/ETS.

Stochastic Volatility Models and the Pricing of VIX Options is written by Joanna Goard, Mathew Mazur and published in Mathematical Finance.

Option selling has always been a fascination for me, and long time readers may recall a lot of the posts I used to do on the subject years ago.

My reads to start the week off: • Freddie Mac Bets Against American Homeowners (ProPublica) • Money From MF Global Feared Gone (WSJ) • 9.8 Million Shadow Inventory Says Housing Market is a Long Way From the Bottom (Naked Capitalism) • Flurry of...

|