(This article was first published on Xi'an's Og » R, and kindly contributed to R-bloggers)

I received the following email about Introducing Monte Carlo Methods with R a few days ago:

Hallo Dr.

Get Started for FREE

Sign up with Facebook Sign up with X

I don't have a Facebook or a X account

Your new post is loading...

Your new post is loading... Your new post is loading...

Your new post is loading...

(This article was first published on Xi'an's Og » R, and kindly contributed to R-bloggers)

No comment yet.

Sign up to comment

Nice article out of Morningstar’s ETFInvestor where they are now tracking six new quant models of ETFs. Many of these use the 12-month SMA and various combinations of value and momentum.

(This article was first published on The Average Investor's Blog » R, and kindly contributed to R-bloggers)

Good evening everybody, I’ve been paying attention to portfolio modelling for the past few months.

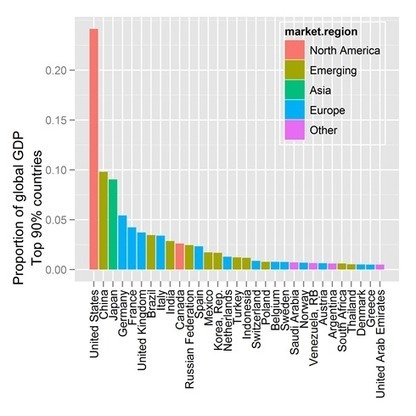

(This article was first published on Decision Science News » R, and kindly contributed to R-bloggers) LEARN HOW TO IMPORT WORLD BANK DATA AND INVEST IN THE WHOLE WORLD Click to enlarge The market cap of the countries comprising 90% of the...

(This article was first published on R snippets, and kindly contributed to R-bloggers)

Standard sample function works differently when it gets single element integer vector as opposed to longer vectors.

(This article was first published on Simply Statistics, and kindly contributed to R-bloggers)

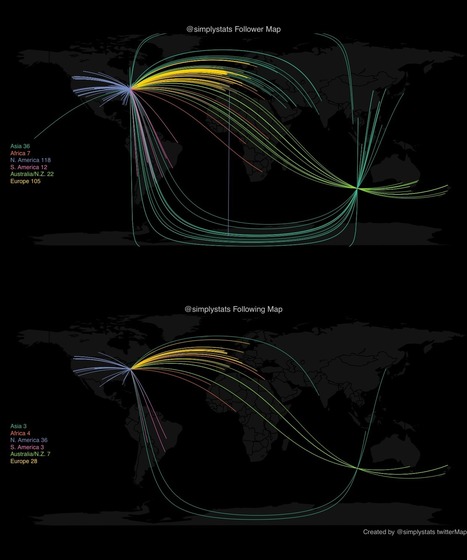

I wrote a little function to make a personalized map of who follows you or who you follow on Twitter.

(This article was first published on Portfolio Probe » R language, and kindly contributed to R-bloggers)

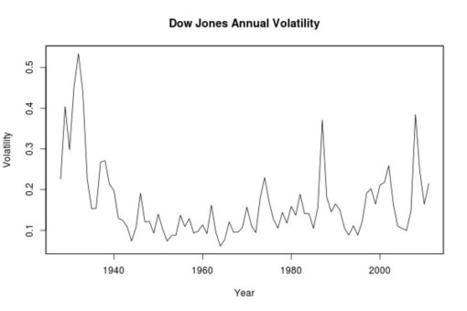

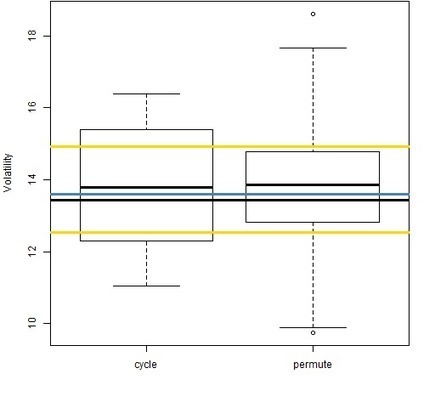

Do non-trading days explain the mystery of volatility estimation?

(This article was first published on [R]appster, and kindly contributed to R-bloggers) On my road to eventually running all of my programs off an USB device I’ve gotten a little bit closer yesterday thanks to input from Duncan Murdoch and...

(This article was first published on Apply R, and kindly contributed to R-bloggers)

I have just realized that UseR! 2011 presentation slides are now available from the conference web site.Unfortunately, no big surprise this year.

Many statistical algorithms are taught and implemented in terms of linear algebra. Statistical packages often borrow heavily from optimized linear algebra libraries such as LINPACK, LAPACK, or BLAS. When implementing these algorithms in systems such as Octave or MATLAB, it is up to you to translate the data from the use case terms (factors, categories, numerical variables) into matrices.

In R, much of the heavy lifting is done for you through the formula interface. Formulas resemble y ~ x1 + x2 + …, and are defined in relation to a data.frame. There are a few features that make this very powerful:

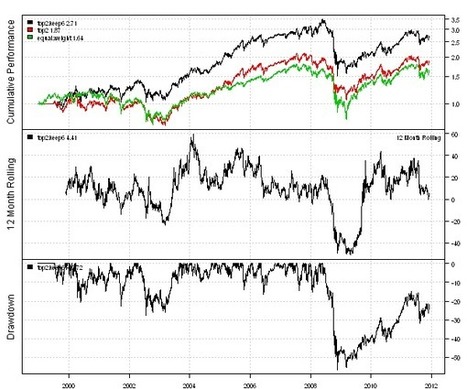

(This article was first published on Systematic Investor » R, and kindly contributed to R-bloggers) I want to illustrate Backtesting with Short positions using an interesting strategy introduced by Woodshedder in the Simple, Long-Term...

(This article was first published on Portfolio Probe » R language, and kindly contributed to R-bloggers)

How does the effect of our expected returns change over time?

|

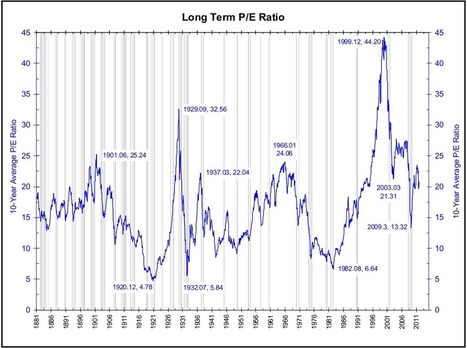

Long term look at Composite Earnings and P/E, using 10 year average: > click for ginormous version All charts courtesy of Bianco Research...

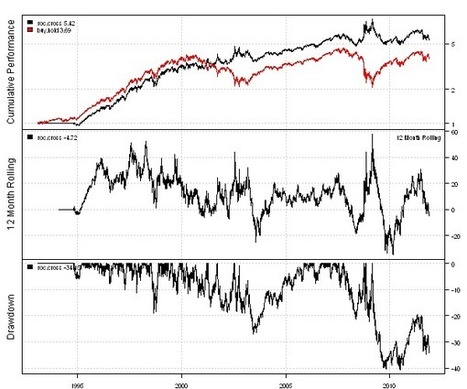

Over the years, I have become friendly with Mebane Faber, co-founder and the Chief Investment Officer of Cambria Investment Management. He manages an ETF called the Cambria Global Tactical ETF (GTAA). Back in 2007, Meb authored an excellent paper titled “A Quantitative Approach to Tactical Asset Allocation.” It was published in the Journal of Wealth Management, Spring 2007. That analysis tested and reviewed simple timing models, using a 10-month moving average on various asset classes as a signal to enter and exit asset holdings. Compared with traditional “Buy & Hold” investing, the performance improvements across all asset classes were quite significant. The methodology has the advantage of being objective, unemotional and mechanical (fee free to insert “first wife” joke here).

(This article was first published on The Dancing Economist, and kindly contributed to R-bloggers) Hello, folks its time to cover some important econometrics tests you can do in R.The Akaike information criterion is a measure of the...

Hi everyone, I was looking at a book to find some algorithm to detect clusters within financial data. I managed to find a decent algorithm for that matter, but I then wanted to test it on some real data.

(This article was first published on Quantum Forest » rblogs, and kindly contributed to R-bloggers) I expect there will be many reviews and wish lists for R this year, with many of them focusing on either running speed or dealing with large...

(This article was first published on Statistical Modeling, Causal Inference, and Social Science » R, and kindly contributed to R-bloggers) Seth Rogers writes: I [Rogers] am a member of an online community of statisticians where I burn a...

(This article was first published on Statisfaction » R, and kindly contributed to R-bloggers)

Baptiste Coulmont explains on his blog how to use the R package maptools.

(This article was first published on Consistently Infrequent » R, and kindly contributed to R-bloggers) Introduction Romain Francois presented an Rcpp solution on his blog to an old r-wiki optimisation challenge which I had also presented R...

I want to discuss the implementation of Rotational Trading Strategies using the backtesting library in the Systematic Investor Toolbox.The Rotational Trading strategy switches investment allocations throughout the time, betting on few top ranked...

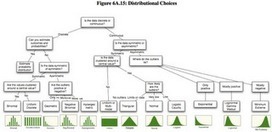

A good starting point to learn more about distribution fitting with R is Vito Ricci's tutorial on CRAN. I also find the vignettes of the actuar and fitdistrplus package a good read. I haven't looked into the recently published Handbook of fitting statistical distributions with R, by Z. Karian and E.J. Dudewicz, but it might be worthwhile in certain cases, see Xi'An's review. A more comprehensive overview of the various R packages is given by the CRAN Task View: Probability Distributions, maintained by Christophe Dutang.

(This article was first published on Research tips » R, and kindly contributed to R-bloggers)

This is a gem of a book. It will become the book I give PhD students when they are learning how to write good R code.

|