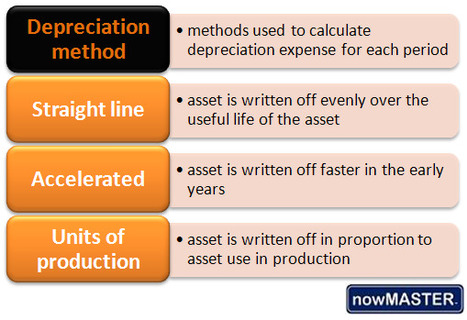

Depreciation in accounting is a process that proportionately expenses the cost of a fixed asset over the asset's useful economic life. In time, fixed assets will eventually lose all their economic value due to a combination of aging, wear and tear, deterioration and/or obsolescence. Depreciation expense ensures that this decline in the value of the fixed assets is matched in the accounting system against the income generated over the same period of the fixed asset’s useful life. Depreciation then is the necessary fulfilment of the matching principle in accounting. While depreciation expense is a bookkeeping entry that does not involve any cash outlay, it is, under certain conditions, an allowable and legitimate tax deduction as a cost of doing business.

Your new post is loading...

Your new post is loading...