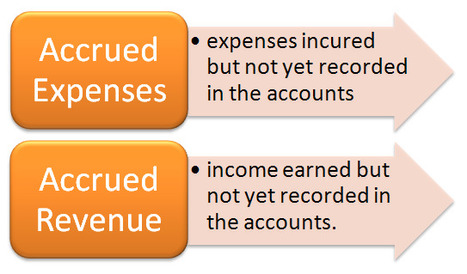

Accruals in accounting are special journal entries that are made by accountants and bookkeepers at the end of each accounting period and prior to the preparation and distribution of the financial statements. Accruals are the practical application of the matching period where income and expenses must be recorded in the accounting period where they are respectively earned and incurred. Accrual entries involve bringing to account revenue that has been earned but not yet invoiced and expenses that has been incurred but not yet billed.

Your new post is loading...

Your new post is loading...