Your new post is loading...

|

Scooped by

Institut sur la gouvernance (IGOPP)

August 16, 2021 9:08 AM

|

There is no standard measure of environmental, social and governance (ESG) performance—and the system is largely being used as greenwash.

|

|

Scooped by

Institut sur la gouvernance (IGOPP)

August 13, 2021 11:00 AM

|

When upstart activist hedge fund Engine No. 1 secured three seats on the board of ExxonMobil in June, it was a high-profile repudiation of the way the country’s largest oil company has long conducted business: with a laser focus on returns and a blind eye to its impact on the world at large. The fund vowed to push ExxonMobil to develop a plan to address climate change and reduce its carbon footprint. Exxon’s responsibility as a business would no longer be only to its shareholders, the boardroom showdown signaled, but also to the public and the planet. [...] Activist investors have come a long way: from corporate raiders to climate heroes. Historically, activist funds have focused on short-term returns. They hold their shares for one, two, or, in “extreme cases,” three years, according to a January 2020 paper by Mark DesJardine, an assistant professor of strategy and sustainability at Penn State, and Rodolphe Durand, founder of the Society and Organizations Research Center at the business school HEC Paris. The average investment horizon of an activist hedge fund, DesJardine says, is about 13 months.

|

|

Scooped by

Institut sur la gouvernance (IGOPP)

August 10, 2021 10:32 AM

|

[...] At a recent roundtable hosted by Willis Towers Watson, board members expressed concerns about climate issues and risks, specifically physical, liability and transition risks. Because risks and their relative importance vary considerably by company and industry, organization leaders and board members are sorting through which risks are most appropriate for their companies to address. Board members also see both managing risk and driving performance as key to creating value for all stakeholders, including regulators, shareholders, employees and consumers. How well the company addresses these issues also is considered a way to attract and retain employees, customers and investors (which, ultimately, equals more capital). [...] Climate risks typically are viewed in three broad categories: - Physical risks: These risks arise from weather-related events and slow-onset climatic changes that can affect a company’s assets, people, infrastructure and supply chains.

- Liability risks: These include product liability claims brought by states, cities and activists, as well as claims against businesses for failing to adapt to a transition to a low-carbon economy or failing to heed professional advice on physical risks’ impacts on supply chains, infrastructure and processes.

- Transition risks: These arise from regulatory and policy requirements (e.g., mandatory carbon pricing policies that increase a company’s cost of capital).

Shareholder activism is on the rise. Once a tool used primarily to direct and shape the composition of a company’s executive board, it is increasingly utilized by equity shareholders seeking to influence mergers & acquisitions and corporate governance issues. In recent years, new strategies have emerged that have increased the scope and power of activist methods, aided by social media and encouraged by a rise in successful dissident actions. We asked Teresa Tomchak of Farris LLP to walk us through the latest developments and trends in shareholder activism and what it means for Canada’s corporate sector.

BlackRock Launches Biggest ETF Ever – and It’s Green,” trumpeted Yahoo Finance. “BlackRock secures largest-ever ETF launch as green investing wave builds,” heralded the Financial Times. By the time the world’s largest investment house unveiled its U.S. Carbon Transition Readiness ETF (LCTU) in early April, investors had poured a cool US$1.25 billion into it. That didn’t just make it the largest launch of any ESG-aligned (environmental, social, governance) ETF to date, it was the “biggest launch in the ETF industry’s three-decades history,” as Bloomberg noted. Another $500 million was invested in its sister fund, BlackRock World ex U.S. Carbon Transition Readiness ETF (LCTD). It was quite a PR comeback, considering BlackRock had been getting skewered in the press after its former head of sustainable investing, Tariq Fancy, penned a handful of damning op-eds calling most sustainable investing “PR spin” and a “deadline distraction” from climate change. Nevertheless, the new BlackRock U.S. Carbon Transition Readiness ETF arrived to much praise. Its stated approach: investing in large- and mid-cap companies that “BlackRock believes are better positioned to benefit from the transition to a low-carbon economy.” Of course, believing a company is well positioned to benefit from the transition is one thing; seeing them actually lead the transition is another.

There was a time not long ago when a company was evaluated on an after-tax basis, and it would benchmark its effective tax rate (ETR) against those of its peer group or industry. Corporate tax was a line item that needed to be managed, and management regularly sought opportunities to achieve a more favorable ETR. Investors and shareholders in companies often received little in-depth information about a company’s tax policies. This often created an environment where companies adopted strategies focused on cross-border financing arrangements, transfers of IP to low-tax jurisdictions, and transfer pricing as opportunities to create enterprise and shareholder value through tax base erosion. While many of these strategies followed the letter of the law, they often leveraged tax law mismatches between countries or moved income producing assets to low tax jurisdictions. [...] Institutional Investors are taking a leading role advancing responsible tax policy – at both the organisation and the investee/portfolio company levels. Norges Bank believes that responsible corporate tax plays an important role in societies and has made this one of its investment principles. Nicolai Tangen, CEO, told the Norwegian Parliament that it had recently divested from companies with weak or no reporting related to tax and transparency.

American International Group Inc. plans to use an IPO to sell part of its life and retirement business, while Blackstone Group Inc. agreed to buy a sizeable stake, according to a person familiar with the matter.

Boards are central to companies addressing ESG issues and should look to enhanced diversity and expertise to fulfill this role in a positive way, according to SEC member Allison Herren Lee

A CEO change is always an exciting moment for all parties involved. Boards invest immense time and resources to find the next CEO for the firm. Stakeholders, inside and outside of the firm, are on their toes, as they try to anticipate where the new leader will take the organization. And last but not least, the new leader is in the spotlight, eager to make a visible difference, and under high pressure that any changes will have to be towards a more successful direction.

Credit Suisse’s top management is under pressure to come up with an overhaul plan for the scandal-hit Swiss bank that could include a potential merger with rival UBS, three people familiar with its thinking told Reuters.

Shareholder proposals that would require companies to disclose more activities are gaining traction.

Activist investors have some menacing tools of the trade. First comes the phone call, letting a boss know they have a new arrival on the share register. Then there is the slide deck, enumerating all the failings for which the boss is supposedly responsible. Sometimes the body language when predator and prey meet for the first time can be the most unsettling.

The coming years are seen by many as an opportunity to rebuild the economy with ESG reporting at the forefront. So, registrants, gone are the days when ESG efforts were merely a public relations tactic and you could get away with promising without delivering.

|

|

|

Scooped by

Institut sur la gouvernance (IGOPP)

August 16, 2021 9:04 AM

|

More than US$16 trillion worldwide is currently sitting in government bonds yielding negative real returns. Meanwhile, the world needs at least US$35 trillion of sustainable investment to avoid the 1.5 degree increase in global temperatures that the UN Intergovernmental Panel on Climate Change warns is now imminent.

|

|

Scooped by

Institut sur la gouvernance (IGOPP)

August 11, 2021 11:20 AM

|

This study provides new evidence on the impact of activist hedge funds in influencing target companies’ operational performances, especially distinguishing four different types of activism demands: 1) changing corporate governance, 2) restructuring balance sheet, 3) implementing growth strategies, and 4) cutting cost and divesting non-core assets. While a general improvement in operating performances is observed across activist-targeted public companies, I find that the group four hedge funds tend to have greater positive impacts as measured by operating metrics such as return on assets (ROA) and gross profit margin (GPM). The research addresses understudied areas of shareholder activism and identifies the subtle differences among different types of activist hedge funds. This analysis aims to provide passive investors a better forecast of the impact of the identified activist investor type.

|

|

Scooped by

Institut sur la gouvernance (IGOPP)

August 6, 2021 11:18 AM

|

Recent literature finds that firms led by female CEOs are more likely to be targeted by activist shareholders, and that female CEOs are more likely to cooperate with activist shareholders’ requests. [...] Our results suggest that investors rely on gender stereotypes when evaluating the responses of male and female executives to shareholder activism, and that these evaluations affect their investment judgments. Our results also suggest a potential alternative explanation for the finding that female CEOs are more likely to cooperate with activist shareholders than male CEOs. Rather than inherent differences in the management style of male and female CEOs, responses may be driven, at least in part, by managers anticipating that they will be penalized by investors for deviating from gender-stereotypical behavior.

Activist Insight issued The Activist Investing Half-Year Review 2021 in collaboration with Olshan’s Shareholder Activism Practice Group. The review highlights major news and trends shaping shareholder activism during the first six months of 2021, ESG issues, federal regulations that could impact shareholder activism, and statistics on activist campaigns during the 2021 proxy season. The review also features an in-depth interview with Andrew Freedman, Co-Head of Olshan’s Shareholder Practice, for the Q&A feature. Andy spoke on the following: rebounding and growth of activism during the pandemic, ESG activism, M&A opposition, and the SEC and how it relates to shareholder activism.

Over the last 12 months, there have been important developments in Australia in relation to climate change risks. Australian regulators have set a clear expectation that entities and their officers must not only disclose material climate risks but also take proactive measures to mitigate those risks to avoid liability. There has also been a marked increase in shareholder and broader community activism on climate change, and this has been a major ‘pressure point’ for entities to commit to emissions reductions targets and other mitigating action. [...] Regulatory and court developments in the last 12 months have fundamentally changed the climate risk and liability position in Australia for all entities and their officers. There is now a clear expectation from APRA and ASIC that entities must not only assess and disclose the material climate risks which impact on their operations but also take proactive steps to mitigate and manage those risks. Continued shareholder and community-based climate activism also places pressure on entities to commit to emissions reductions targets. The recent recognition of a duty owed by the Australian Government to avoid the risk of personal injury to Australian children from climate change in determining whether to approve new development proposals also breaks new legal ground and may lead to the recognition of a similar duty owed by both public and private sector entities in the conduct of business operations in future years.

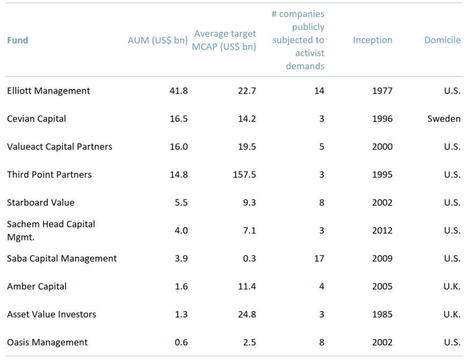

Activist funds are making a comeback after a retrenchment in 2020 due to Covid-19. Smaller companies are particularly vulnerable. The resurgence in activist strategies and the growth in new players in this space is driven by two factors – sustainability/ESG and a frustration with passive investment strategies. In companies above $500m MCAP activist campaigns often raise legitimate concerns, but they tend to destroy Total Shareholder Return (TSR) for 12 months. 50% of CEOs subject to an activist campaign end up moving roles, according to data presented by Boston Consulting Group (BSG). The number of new players in the activist space is likely to account for greater than 30% of all campaigns. [...] Key points: - Activist funds purchase shares of companies in order to effect a significant change in the company while advancing their investor agenda – e.g. targeting environmental and social issues.

- Some consider the role of activists as all smoke and mirrors – Trian Partners took a US$ 2.5bn stock position in General Electric (NYSE: $GE) in 2015 and any significant outcome of its campaign is yet to be seen.

- While the pandemic temporarily reduced the number of activist campaigns during 2020 – two global trends suggest a rebound – frustration with certain aspects of passive investments (funds that track an index and not an individual stock and carry out nil verification or due diligence) and ESG / sustainability, itself driven in large part by both climate and social change data.

A group of activist investors seeking to wrest control of Martin Shkreli’s pharmaceutical company failed miserably this week — with the “Pharma Bro” voting his shares from prison.

Vivendi is going to spin off Universal Music Group on the Euronext Amsterdam exchange this fall. The New York Stock Exchange would help UMG tap into the U.S. market.

Credit Suisse Group AG is considering centralising the management of its bankers to the world's wealthy, reversing a regional structure put in place six years ago, as the scandal-plagued Swiss bank looks for ways to tighten controls and improve operations, three sources familiar with the matter said.

How can the board of the future keep pace? To help boards stay agile and relevant, board education practices should adapt to reflect the rapidly evolving external developments and strategy, risks and talent oversight needs.

Japan’s trade ministry on Friday denied its officials directed an adviser to contact Toshiba Corp shareholders as part of a plan to pressure them to support management in a key vote on board membership.

Despite more than 80 per cent of Thomson Reuters shareholders voting against the B.C. Government and Service Employees’ Union’s (BCGEU) human rights proposal, the result felt like a victory to Emma Pullman, the union’s capital markets advisor.

|