Your new post is loading...

|

Scooped by

Institut sur la gouvernance (IGOPP)

August 28, 2020 11:42 AM

|

Norway’s $1.2 trillion wealth fund will publish all voting intentions ahead of shareholder meetings from 2021, which is at least one year earlier than previously indicated. The world’s biggest sovereign investor says it wants to be more transparent in how it exercises its ownership, in a bid to promote good corporate governance and similar goals, including environmental standards. The fund has already started explaining its reasoning when it votes against company boards. “Our intention is to provide more information to the market and to be fully transparent about how we use our voting rights,” Norges Bank Investment Management, said in a report on Friday, as part of a review of its work on responsible investment over the past 20 years. The fund also said it was “concerned that a lack of information makes the market for voting advice not fully efficient.” Norway’s wealth fund, which was built from the proceeds of the country’s oil and gas production and now owns about 1.5% of stocks worldwide, invests according to a broad set of ethical principles. These include a ban on some weapons, tobacco and most coal investments, in addition to rules on human rights and greenhouse gas emissions. [...] The fund has been cleared to venture into renewable energy infrastructure under these mandates, but has yet to make its first investment. The effort will be led by outgoing Chief Executive Officer Yngve Slyngstad, who is set to move to London after Nicolai Tangen succeeds him next week. “Over time, we expect our renewable investments to diversify the fund and generate higher returns than the assets we sell to finance their purchase,” the fund said.

|

|

Scooped by

Institut sur la gouvernance (IGOPP)

August 26, 2020 11:20 AM

|

We examine the governance role of delegated portfolio managers. In our model, investors decide how to allocate their wealth between passive funds, active funds, and private savings, and asset management fees are endogenously determined. Funds' ownership stakes and asset management fees determine their incentives to engage in governance. Whether passive fund growth improves aggregate governance depends on whether it crowds out private savings or active funds. In the former case, it improves governance even if accompanied by lower passive fund fees, whereas in the latter case, it improves governance only if it does not increase fund investors' returns too much. Regulations that decrease funds' costs of engaging in governance may decrease total welfare. Moreover, even when such regulations are welfare improving and increase firm valuations, they can be opposed by both fund investors and fund managers.

|

|

Scooped by

Institut sur la gouvernance (IGOPP)

August 13, 2020 10:54 AM

|

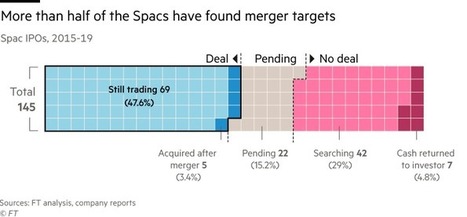

[...] From hedge fund billionaire Bill Ackman to sports executive Billy Beane of Moneyball fame, some of the most high-profile investors have sought to raise cash in blank cheque companies, believing they have the special eye to find under-appreciated businesses which they can bring to the public markets. By using Spacs, they can skip over the expensive and time-consuming IPO process. [...] The boom in Spacs is taking place at a time when trillions of dollars sitting in private equity and venture capital funds and many promising companies feel less pressure to go through the costly and time-consuming process of listing on the stock market in order to raise new money. For retail investors, Spacs present a chance to buy into fast-growing companies that might otherwise remain private. Yet a Financial Times analysis of the US blank cheque companies that were organised between 2015 and 2019 shows that these cash shell structures remain a dicey bet for ordinary investors. The majority lie below $10 per share, the standard price where Spacs first sell their shares to the public. Such disappointments have beset even veteran investors such as private equity firm TPG, which has three Spacs, none of which trade higher than $10.20. The poor investment record of many Spacs is a reminder that when Wall Street pushes a new product, clever financiers invariably find a way to shift the most risk on to ordinary investors - even if a new generation of Spac founders believes they will avoid the problems of the past. “Overall, investing in a Spac is like flipping a coin, where only half of them are shown to be value creating,” says Milos Vulanovic, a finance professor at EDHEC Business School who has studied the structure for years.

|

|

Scooped by

Institut sur la gouvernance (IGOPP)

August 4, 2020 10:38 AM

|

[...] The tale is a cautionary one, given the high fashion for reverse listings these days. In the US, special purpose acquisition companies, or Spacs, last year accounted for a quarter of all IPOs. [...] Spac fans said it is a natural time for the sector to boom: many private companies are struggling following the coronavirus pandemic, and the lockdowns that accompanied it, and are seeking easy access to finance. Stock markets are booming, giving Spacs a straightforward route to market. But there is nervousness among investors towards more complicated corporate IPOs. Spacs, backed by big-name sponsors, provide investors with the comfort of a trusted intermediary. There are structural advantages too. In volatile times like these, it is attractive if a company can fix a price and execute a deal quickly, and avoid the delays and hassle inherent in filing an IPO prospectus and being scrutinised by regulators, before being able to list. Investment banks’ IPO fees, particularly hefty in the US, can also be mitigated. The downsides are obvious. In some jurisdictions at least, the level of information that investors get of a company that reverse-lists is scant, though US Spacs stress that the disclosures in their merger prospectuses are just as fulsome as a mainstream IPO would demand. Another negative is the dilution effect for company owners and investors, effected via complex warrant structures attached to the vehicles’ listed equity. And there is an inherent conflict of interest in the value of payback for sponsors being tied to the price paid for a merger. Deals also tend to be magnets for a “Spac mafia” of arbitrage hedge funds which buy up the warrants to exploit short-term pricing anomalies.

Active equity mutual funds are well known to have underperformed passive benchmarks net of fees. Even so, the active management industry continues to manage tens of trillions of dollars. The puzzling coexistence of a large underperforming active management industry and an accessible passive management industry raises an important question: why are investors willing to tolerate this underperformance? One popular hypothesis is that active funds outperform in market downturns, when investors value performance the most. The COVID-19 crisis is particularly suitable for testing this hypothesis, for two reasons. First, investors surely want to hedge against such an unprecedented output contraction and unemployment surge. Second, large price dislocations during this crisis provide opportunities for active managers to perform well. For example, the S&P 500 experienced its steepest descent in living memory, losing 34% of its value in the five weeks between February 19 and March 23 before bouncing back by over 30% in the following five weeks through the end of April.

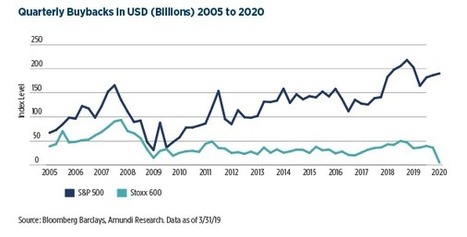

[...] The robust recycling of the capital within the US economy can lead to innovation and growth that avoids the “trapped capital” syndrome of Europe and Japan. A higher level of profitability has enabled US companies to dedicate more capital to share repurchases (or buybacks). A key advantage of share repurchases is that they enable the recycling of capital throughout the economy, so capital may end up in the most innovative hands and not trapped inside of less efficient, more mature companies. We believe buybacks optimize capital allocation for companies unable to invest at a higher rate of return than their cost of capital, particularly when agency costs exist between corporate management and investors. While perhaps controversial to some, we disagree with those who argue that buybacks are shortsighted and lead to less innovation and investment, suppress job growth and exacerbate income equality. While the aftermath of the pandemic and subsequent recession will certainly lower activity, we expect share repurchase programs in the US will rise to their previous levels when conditions normalize. We agree companies should not assume irresponsible amounts of leverage to buy back stock. However, in reality, the aggregate amount of buybacks represents a small percentage of total capital returned to investors. Given the likely challenges associated with assuming additional leverage and corporate models that may shift to more commoditized, lower return businesses in the aftermath of the pandemic, we expect that the recycling of high-return capital to innovation and secular growth will simply sustain itself. While we acknowledge that companies with large buyback programs have tended to invest less in innovation, our findings suggest the US economy has done an efficient job of recycling the proceeds from share repurchases through venture capital and private equity firms. [...] Share repurchases have steadily increased in the US over the last 20 years and the gap in buybacks between the US and Europe has widened in the last 10 years, both in nominal and relative terms. In Europe, barely 20% of Stoxx 600 corporations have executed share buybacks versus more than 80% of its S&P 500 peers.

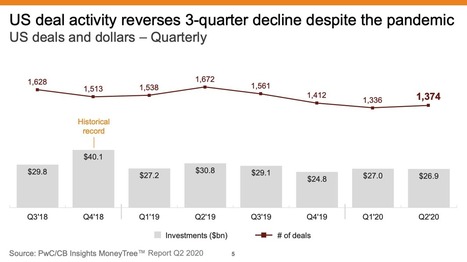

In Q2’20, US-based startups continued to pick up deals and dollars during the Covid-19 crisis. Venture capitalists didn’t let the global pandemic stunt dealmaking in the second quarter of the year. Though funding took a hit in Q2’20 both globally and in the US, deal activity recovered compared to Q1’20. However, the extent of Covid-19’s impact remained visible when compared to 2019 levels. Deal activity in Asia rises 20% in Q2’20, compared to 9% in Europe and 3% in North America. Download the CB Insights and PwC MoneyTree Report to see all the data. We take a look at how the coronavirus pandemic has shaped venture capital financings in Q2’20.

1. VC deals to US-based startups in Q2’20 saw a quarterly increase but were down compared to last year [...]

2. The number of quarterly mega-rounds ($100M+) in the US hit a new record in Q2’20 [...]

3. Unicorn births declined for the fourth consecutive quarter

The number of new unicorns in the US steadily declined over the past year. [...]

4. In the US, IPO exits jumped while M&A activity fell amid the pandemic. [...]

5. Globally, deals recovered compared to Q1’20 while funding dropped [...]

6. Digital health dominated deal activity in the US

Digital health and medical devices saw an increase in deals in Q2’20, as companies scrambled to develop solutions for the pandemic.

The pandemic has had an emphatic impact on rewards for shareholders. A report this reveals that dividend payments in the UK were cut in the second quarter by a “dizzying” 57.2%, or £22bn. The statistics, compiled by Link Asset Services, show that 176 companies opted to hold on to cash during the lockdown by cancelling dividend payments. A further 30 reduced their dividends. In all, they amounted to three-quarters due to pay in Q2. Link says dividends paid in Q2 this year are the lowest since 2010 and “the decline itself is by far the biggest ever recorded”. Only the scale of the figures should come as a surprise. As lockdown took effect, many sectors saw business grind to a halt forcing them to seek state aid as well as take drastic measures. Many took government loans, making dividend payments—even if cash was available—a significant reputational and financial risk. [...] Resetting dividends is viewed as a healthy development by many market observers concerned that some big-name companies have paid out at record levels while also managing significant debt. In more stable times a dividend cut may have been viewed by the market as a red flag; in the current environment many regard it as good sense. Another consideration for boards mulling dividend payments is: are they legal?

Warren Buffett finally found his next crisis-era deal. His Berkshire Hathaway Inc., which has stayed relatively quiet during the tumult of the coronavirus pandemic, broke its silence at the end of a holiday weekend with its biggest acquisition in more than four years. The agreement for Dominion Energy Inc.’s natural gas pipeline and storage assets signaled to the market that Buffett is willing to pounce despite his cautious tone in May about the pandemic, according to David Kass, a professor of finance at the University of Maryland’s Robert H. Smith School of Business. “He’s willing to make investments now, of a fairly sizable amount,” Kass said. “It’s very positive that he’s sending a signal for the right deal at the right price, $10 billion or more, ‘We’re ready to go, we’re ready to invest.’” [...] His inability to make a major acquisition recently has drawn scrutiny from his critics, who argued that Buffett lost his ability to pull off the game-changing transactions that helped vault Berkshire into the ranks of the most valuable U.S. public companies. Now, the deal to buy substantially all of Dominion Energy’s natural gas transmission and storage assets for $4 billion, along with the assumption of $5.7 billion in debt, shows that Buffett is willing to put his money to work, Kass said. [...] Buffett has considered its energy business one of the “lead dogs” of Berkshire’s non-insurance operations alongside its railroad. Berkshire’s purchase expands its hold in the sector, adding more infrastructure to handle natural gas to its already sprawling energy operations across states such as Nevada and Iowa. Berkshire also struck the deal at a low point in the market. Natural gas futures in the U.S. dropped last month to their lowest point in 25 years and have recovered just slightly since then. “This looks like confirmation that commodities like energy are undervalued,” Bill Smead, chief investment officer at Smead Capital Management, which owns Berkshire shares, said in an emailed comment. “At the bottom, assets move from weak hands to strong hands.”

Private equity fund managers are planning for a summer like no other. Flush with more cash than ever before – a $2-trillion war chest – fund managers around the world are aggressively pitching deals to businesses battered by the economic fallout from the novel coronavirus. Canadian players are in the heart of the action, with everyone from multibillion-dollar pension plans and global fund managers to smaller PE funds that buy family-owned companies looking past COVID-19, and trying to find ways to invest in an economy that is bouncing back. There is only one problem: Few are willing to sell – at least so far. Business owners and boards who might have been willing to negotiate just a few months ago are now refusing to engage with potential buyers, based on well-founded fears they would be selling at virus-induced discounts. Propped up by government wage and credit support, many are opting instead to wait for an expected recovery and a return to heady, pre-pandemic price tags. It’s creating a delicious dynamic in corporate Canada and around the globe. Sophisticated private equity investors are itching to put capital to work at what they perceive as bargain-basement prices, while equally savvy sellers are holding out for better offers. [...] Bruce Flatt, chief executive at Brookfield Asset Management Inc., gave an optimistic assessment of the situation at a recent conference. [...] Mr. Flatt, who oversees US$60-billion of what’s known as “dry powder” – uncommitted capital from clients of Toronto-based Brookfield – told a virtual meeting of the Canadian Venture Capital and Private Equity Association (CVCA) that the crisis will leave many businesses in need of new capital or under pressure to sell divisions. As a virtual audience of 600 nodded their heads approvingly, he said, “There are going to be a lot of opportunities for private equity over the next six to 12 months.”

Typically, when a company offers stock to the public, it emphasizes the positive. Fundamentally, the pitch is this: Buy us and prosper. Maybe even get rich. But Hertz Global Holdings put out a prospectus this week that projected a different outcome: Gamble on us and be prepared to end up with something worthless. Hertz, you see, is bankrupt. But it said it hoped to sell $500 million in shares, maybe even $1 billion, anyway. For sheer audacity, what Hertz was trying just takes my breath away. It caught the eye of the Securities and Exchange Commission, too. On Wednesday, Jay Clayton, the agency’s chairman, said on CNBC, “We have let the company know that we have comments on their disclosure,” and added, “In most cases, when you let a company know that the S.E.C. has comments on their disclosure, they do not go forward until those comments are resolved.” [...] Trading in the company’s shares stopped briefly at 11:44 a.m. and in a new filing, Hertz said it had suspended its new stock offering, while it discussed matters with the S.E.C. The S.E.C. declined to expand on Mr. Clayton’s statement, and Hertz did not respond to repeated requests for comment. What is unusual in the Hertz stock venture is that the company is still in the early stages of what are formally known as Chapter 11 bankruptcy proceedings. Companies in bankruptcy do not, as a rule, sell stock, precisely because creditors have a higher claim on assets than shareholders do. By the time the creditors have been paid a fraction of what they are owed, there may be nothing left for shareholders.

Despite recent challenges, venture capital firms are still seeking out investment opportunities across the country. Since our last analysis of most active VCs in January 2020, we've seen shake-ups across 10 states. Our graphic maps out the most active VC investor in every US state. Although startups based in California, New York, and Massachusetts have traditionally accounted for the majority of VC tech investment in the US, VCs are spurring other hotbeds of innovation across the country. The Covid-19 pandemic put a dent in VC deal activity during Q1’20, while investors cut fewer but larger checks, with funding up 14% quarter-over-quarter. Using CB Insights data, we analyzed the most active venture capital firms investing in tech startups in every US state.

Private equity (PE) firms are often said to use their industry expertise and operational know-how to identify attractive investments, to develop value creation plans for those investments, and to generate attractive investors returns by implementing their value creation plans. Although many studies refer to such value creation plans, there is no systematic evidence on what these plans typically look like or whether they help improve company operations or investor returns. In a recent paper, we open up the black box of value creation in private equity with the help of confidential information on value creation plans and their execution. We find that plans are tailored to each portfolio company’s needs and circumstances and have become more hands-on. Successful execution varies systematically across funds and is a key driver of investor returns. Company operations and profitability improve in ways consistent with successful execution, even beyond PE funds’ exit.

|

|

|

Scooped by

Institut sur la gouvernance (IGOPP)

August 26, 2020 11:26 AM

|

The U.S. Securities and Exchange Commission is easing restrictions that prevent most people from investing in hedge funds and hot startups. olders of professional certifications -- like Series 7 licenses that authorize individuals to sell securities -- will be eligible to invest in riskier assets under rule changes the regulator announced Wednesday. The revamp is focused on allowing those with financial expertise to put their money in private investments that don’t trade on public exchanges even if they fail to meet existing net worth and income restrictions. The SEC said in a statement that the changes are meant to make it easier for firms to raise capital and “more effectively identify institutional and individual investors that have the knowledge and expertise to participate” in those offerings. “Today’s amendments are the product of years of effort by the Commission and its staff to consider and analyze approaches to revising the accredited investor definition,” SEC Chairman Jay Clayton said in a statement. “For the first time, individuals will be permitted to participate in our private capital markets not only based on their income or net worth, but also based on established, clear measures of financial sophistication.” The changes, which were first proposed in December, adjust the SEC’s “accredited investor” standard. The policy has generally kept investors out of hedge funds, fast-growing technology companies that haven’t gone public and private equity funds unless they have a net worth of $1 million or higher and annual salaries of at least $200,000. The SEC’s two Democratic commissioners voted against the revamp, arguing that by failing to update the net worth and compensation requirements for inflation, the regulator missed an opportunity to protect many unsophisticated investors from putting their money in potentially dangerous assets. Commissioners Allison Lee and Caroline Crenshaw, in a joint statement, said the 38-year-old thresholds hardly mean the same thing in today’s dollars.

|

|

Scooped by

Institut sur la gouvernance (IGOPP)

August 24, 2020 9:37 AM

|

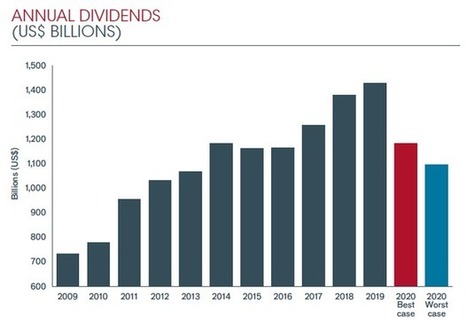

The coronavirus crisis will see the world’s biggest firms slash dividend payouts between 17%-23% this year or what could be as much $400 billion, a new report has shown, although sectors such as tech are fighting the trend. Global dividend payments plunged $108 billion to $382 billion in the second quarter of the year, fund manager Janus Henderson has calculated, equating to a 22% year-on-year drop which will be the worst since at least 2009. All regions saw lower payouts except North America, where Canadian payments proved to be resilient. Worldwide, 27% of firms cut their dividends, while worst affected Europe saw more than half do so and two thirds of those cancel them outright. “2020 will see the worst outcome for global dividends since the global financial crisis,” Janus Henderson said in a report published on Monday. “We now expect headline global dividends to fall 17% in a best-case scenario, paying $1.18 trillion... Our worst-case scenario could see payouts drop 23% to $1.10 trillion.” [...] “Dividend trends are reflecting the trends in society and the stock market at the moment,” said Janus Henderson’s head of global equity income, Ben Lofthouse. [...] The most obvious is the path of the coronavirus, but there is also what U.S. firms do later this year and whether Europe’s banks get the green light early next year to restart their payments. “The big question for the U.S. is what will happen in the fourth quarter. If many companies make significant cuts to their dividends, payouts will be fixed at a lower level until towards the end of 2021.”

|

|

Scooped by

Institut sur la gouvernance (IGOPP)

August 12, 2020 11:44 AM

|

Down rounds—equity financing rounds where the company’s valuation is lower than at least one of its previous rounds of financing—have been rare in the sellers’ market of the past few years, where high valuations fueled by an abundance of capital is the norm. However, as the impact of COVID-19 and other black swan events permeates global economies, an increasing number of companies will grapple with fundraising in an environment of increased investor caution around valuations and deployment of capital, particularly for pre-profit companies in harder-hit sectors. In this installment of the MoFo PE Briefing Room, we discuss a few tips for investors when navigating a down round, both as an existing investor and as a new investor coming into the company.

1. Understand your rights. What are they, and how can you use them?

2. As a new investor, use your negotiation leverage over both the company and the existing investors.

3. Use the down round as an opportunity to renegotiate for better terms.

Days before, Slyngstad had announced his decision to resign as chief executive of the oil fund — the largest sovereign wealth fund in the world — after an impressive 12 years, during which the fund had topped $1 trillion in assets and sparked headlines for announcing its intention to divest from shares in the very asset from which it derives its wealth: oil. [...] Tangen is a celebrated stock picker. But the oil fund is de facto an index tracker fund, which is forbidden from investing outside of listed stocks and bonds, except in unlisted property. NBIM, whose investment management arm Tangen will soon lead, must keep to benchmarks set by the Finance Ministry, with a tracking error of just 1.25 percent. “The role of chief executive is not very influential on the way the fund is managed,” says Kapoor. He points out that though NBIM has a staff of more than 500 well-qualified and experienced managers, it is fewer than 20 bureaucrats in the Finance Ministry, “with little financial expertise and no experience,” who really call the shots. “The job is high-profile, yes, but the difference between a good job running NBIM and a bad job running NBIM is not really noticeable in terms of performance, because it only has a [small] tracking error from the benchmark set by the Finance Ministry. Room for maneuver is very limited.” This was a problem encountered by Slyngstad during his 12 years as head of the fund. He called repeatedly for the fund to enter into new asset classes such as private equity — calls that were rebuffed by the Norwegian government and the central bank. In 2018, a year before his departure, Slyngstad presided over a momentous inquiry into whether the oil fund should continue to be housed in the central bank, itself a highly unusual arrangement unlike those of other large sovereign wealth funds.

Investors caught up in the frenzy of the stock market’s wild rebound this year have a new favorite spot for their money: pools of cash that hunt for acquisitions. Some will pocket huge gains and others will be saddled with deep losses from these so-called blank check companies, but one group -- Wall Street’s top banks -- is coming out a winner. Three of them -- Citigroup Inc., Credit Suisse Group AG, and Goldman Sachs Group Inc. -- now account for nearly half of underwriting revenue, meaning they stand to generate, according to Dealogic, at least $400 million in fees from blank check companies that have listed this year. That’s a record amount of cash from a market that at one time barely generated anything for the largest firms. [...] It’s a notable transformation for SPACs, which were once an obscure part of the market tainted by association with penny-stock scandals. [...] The products’ popularity has been pushed by yield-hungry investors, who see SPACs as safe bets that could offer better returns than Treasuries. The money earns interest until a deal is struck. If a manager can’t find a deal in a certain time or investors don’t like the planned merger, they can get their money back. If a merger is successful, then investors can share in those gains. Banks typically take a 2% cut of money raised from selling shares in a public listing. Once a SPAC completes a merger, the firms are then given 3.5% of initial public offering proceeds. And they can earn extra fees for every service provided along the way, for example by raising more funding for a merger or helping to find a company to purchase. [...] SPACs account for nearly 40% of the IPO market this year up from only 1.1% a decade ago, according to Dealogic data.

On June 29, 2020, the U.S. Department of Labor (DOL) announced a new proposed class exemption to certain prohibited transaction restrictions in the Employee Retirement Income Security Act of 1974, as amended (ERISA), and the Internal Revenue Code of 1986, as amended (the Code), entitled “Improving Investment Advice for Workers & Retirees.” The proposed exemption is intended to help workers and retirees by preserving the wide availability of investment advice arrangements and products for retirement investors. The proposed exemption is expected to be well-received by “investment advice fiduciaries,” because it is broader and more flexible than the DOL’s pre-existing prohibited transaction class exemptions which generally provide relief for more discrete transactions. Here are five things you should know about the proposed exemption.

Bombardier Inc. said it burned through $500-million less cash than expected in its latest quarter and secured new credit worth $1-billion, bolstering its finances as the Canadian manufacturer vies to win regulatory approval and finalize the crucial sale of its rail business to France’s Alstom SA in the months ahead. HPS Investment Partners LLC, a New York-based credit-investment firm with over US$60-billion in assets under management, has agreed to provide a three-year secured term loan to Bombardier of up to US$1-billion, the Montreal-based plane and train maker said in a statement Wednesday. In addition, the company said its cash usage in the second quarter was $500-million better than the previous forecast it gave to investors. It gave no explanation for the change, and a spokeswoman declined to offer more details until the next quarterly earnings report on Aug. 6. “Collectively, these actions provide Bombardier with additional liquidity to operate its business through the COVID-19 pandemic as it works to close the previously announced divestitures undertaken to reshape Bombardier’s capital structure,” the company said in the statement. Bombardier burned through US$2.6-billion of cash in the first half of the year as the coronavirus pandemic led to a slowing of new orders, the suspension of work at factories and the cessation of product deliveries because of border closures. The company’s credit spreads have widened in recent months amid investor concern that it won’t be able to divest its plane parts unit and train assets as previously planned while its liquidity position deteriorates. Those concerns appear to have eased somewhat with Wednesday’s announcement. Bombardier’s widely-held subordinate voting shares climbed 7.7 per cent in early trading on the Toronto Stock Exchange to $0.49.

Private Equity (PE) funds have returned about the same as public equity indices since at least 2006. Large public pension funds have received a net Multiple of Money (MoM) that sits within a narrow 1.51 to 1.54 range. The big four PE firms have also delivered estimated net MoMs within a narrow 1.54 to 1.67 range. Three large datasets show average net MoMs across all PE funds at 1.55, 1.57 and 1.63. These net MoMs imply an 11% p.a. return, which matches relevant public equity indices; a result confirmed by PME calculations. Yet, the estimated total performance fee (Carry) collected by these PE funds is estimated to be $230 billion, most of which goes to a relatively small number of individuals. If all vintage years are included to 2015, Carry collected is $370 billion, with a performance similar to that of small cap indices, but higher than that of large cap stock indices. The number of PE multibillionaires rose from 3 in 2005 to 22 in 2020. Rebuttals from the big four and the main industry lobby body are provided and discussed.

When the Financial Times interviewed Warren Buffett last year, he predicted that future returns from his company Berkshire Hathaway and from the U.S. stock market as a whole would be “very close to the same.” Berkshire shareholders could be forgiven for thinking: if only. The famed stockpicker had his worst performance versus the S&P 500 in a decade in 2019, and 2020 is shaping up to be nearly as bad. Instead of taking advantage of the coronavirus crisis that hit markets in March, Buffett was a casualty. Instead of highlighting Berkshire’s balance sheet strength, the crisis exacerbated longstanding concerns over the company’s direction. Some longtime Buffett watchers argue that it is time to fundamentally rethink Berkshire’s mix of businesses and investments. The question comes more loudly now than at any time since Berkshire missed out on the dotcom boom: has Buffett lost his touch? Four things investors (even Warren Buffett) just have to accept they know nothing about — and one new thing

Costco should be Warren Buffett’s next bulk purchase

Investors sour on airline sector as Warren Buffett exits top U.S. carriers. Berkshire’s “chronic underperformance” requires answers, according to Cathy Seifert, an analyst who covers the company at CFRA Research, particularly in light of some questionable investment decisions in recent years.

While Trump’s U.S. Department of Labor recently opened the door for plan sponsors to add private equity funds to their 401k plans, only the most foolhardy sponsors will rush through. Despite any assurances Trump’s DOL is gratuitously offering, the risk of getting sued is monumental. Corporate sponsors of 401k retirement plans who opt to include private equity in their investment menus could, in my opinion, be sued. Here’s why: First, private equity investments are the highest cost, highest risk investments ever devised by Wall Street. 401k sponsors will be hard pressed to conclude the fees and risks are justified in the pursuit of promises of superior performance. Further, as a result of the weighty fees and other risks, PE investments will more-often-than-not underperform resulting in 401k losses. A decade-plus of private equity investing by so-called “well-managed” pensions has resulted in increasingly disappointing, not to mention inflated and unauditable performance results. A recent Working Paper by Professor Ludovic Phalippou of the University of Oxford concluded higher cost, higher risk PE funds have returned about the same as lower cost, lower risk public equity indices since at least 2006. And Warren Buffett, arguably the world’s most respected investor, recently escalated his criticism of private equity industry ethics and dubious performance claims.

Foreign investors mopped up the flood of new issuance by Canadian governments and companies, a sign the nation continues to be viewed a safe haven. Investors from outside the country bought a net $49 billion (US$36 billion) of Canadian securities in April, the largest monthly purchases from abroad on record, Statistics Canada reported Tuesday. That included $15.8 billion in federal government bonds, as well as $10.2 billion in federal government money market instruments such as treasury bills, both record inflows. Foreign investors also bought $25.4 billion in corporate bonds. The unprecedented purchases coincide with a hefty issuance of federal debt by Prime Minister Justin Trudeau’s government to fund spending to support Canadians through the economic shock and shutdowns caused by COVID-19.

“The strong inflows into Canadian debt markets reveal that, even during the height of the crisis in this country, Canada was seen as an attractive place to park funds,” Katherine Judge and Royce Mendes at CIBC World Markets said in a report to investors.

CHICAGO (Reuters) - Employer retirement plans are not known for their flashy investments - a majority of 401(k) investors these days use target date funds that invest in broad, diversified equity and fixed income mutual funds that automatically rebalance to minimize risk as retirement approaches. That has been a healthy, if unexciting, trend. But in the years ahead, some plan sponsors may start spicing things up. Last week, the federal government opened the door for plan sponsors to add private equity funds to their 401(k) plans. Private equity funds invest in everything from buyouts of mature non-public companies to firms getting ready to go public - and even venture capital startups. Until now, these investments have been available only to wealthy and institutional investors. The private equity industry has been knocking on the 401(k) door for a number of years, and the attraction is not difficult to understand. Defined contribution plans represent a huge pool of investable funds, holding $8.9 trillion in assets at the end of 2019, according to the Investment Company Institute. [...] Private equity advocates argue that these funds can produce higher returns over time than the stock of publicly held companies, even net of fees. “If you think of the stock market as a way for investors to harness the economic power of gross domestic product and capitalizing on that, a growing portion of that activity today is being held by private investors today as opposed to being in the public markets,” said David O’Meara, senior defined contribution strategist at consulting firm Willis Towers Watson.

|