Your new post is loading...

Your new post is loading...

A key consultant for the California Public Employees’ Retirement System (CalPERS) has defended the system selling most of its forestland portfolio at a loss estimated to be around $500 million, saying CalPERS assets are better invested in core real estate.

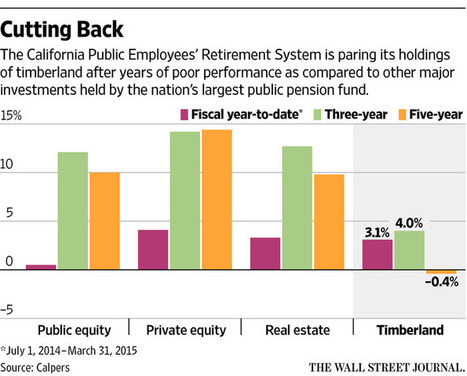

Forestland, real estate, and infrastructure make up the three components of the CalPERS $37.5 billion real assets program, but unlike returns for real estate and infrastructure over the last few years, forestland investments have been a money loser for the system.

Andrew Junkin, president of Wilshire Consulting, who serves as the pension system’s general and forestland consultant, told the CalPERS Investment Committee on August 14 that the recent sale of almost 80% of CalPERS’s $2 billion forestland portfolio was not “a panicked move.”

“I think your [investment] staff spent a lot of time really thinking through the options and finding the best possible solution at this time,” he said. CalPERS sold the portfolio on an unclosed date after the end of the second quarter on June 30.

Junkin said the sale of the forestland portfolio came just before CalPERS would have had to make “a very large principal payment.” He said there had been a recent evaluation of the forestland portfolio’s value, resulting in a markdown. Junkin said even with the markdown, CalPERS officials received a higher price for the sale of the portfolio than the price listed in its valuation report.

Junkin said CalPERS would have had to mark down the portfolio, even if it did not sell the land, based on the evaluation.

CalPERS officials have not disclosed the sale price of the southeastern US timber portfolio or markdown information, but the portfolio was listed as being worth $1.559 billion as of June 30. That number reflects previous markdowns.

CalPERS had paid around $2 billion for the portfolio starting back in 2008, part of then Chief Investment Officer Russell Reed’s plan to help diversity the system’s assets. CalPERS, with more than $352 billion in assets under management, is the largest retirement plan in the US.

CalPERS sources say the pension system lost around $500 million from the sale.

Junkin told the investment committee that the forestland portfolio struggled because of its heavy concentration in the southeast timber market. “Timber prices in the southeast were hit pretty hard in the global financial crisis because that tends to be the market that’s used for home construction,” he said. Junkin said even as home construction recovered, timber prices remained depressed. He said CalPERS’s timing was “poor,” buying the forestland before financial crash, but that “you can’t know in advance that the market’s going to collapse.”

The forestland portfolio was also heavily leveraged, acknowledged Junkin. He has previously said that CalPERS had to harvest trees to pay the debt service on the forestland portfolio. CalPERS officials have not disclosed the level of leverage in the portfolio.

CalPERS data shows that the overall forestland portfolio had a 1.92% return for the one-year period ending June 30, 187 basis points below CalPERS’s forestland benchmark. For the three-year period, the portfolio had a loss of 2.37%, 581 basis points below the benchmark, and for the five-year period, it had a loss of 0.99%, 709 basis points below the benchmark. For the 10-year period, the portfolio saw loss of 1.07%, 513 basis points below the benchmark.